Any concept can drive strong top-line results with increased marketing initiatives that are focused on communicating the concept's compelling value proposition. Nearly 100% of the time, the increase in same-store sales does not come without cost - increased traffic with its value message at the expense of average check and restaurant margins. While the increase in sales might be good for the Franchisor, the operational complexities associated with extreme discounting can be a net negative.

The recent Kentucky Grilled Chicken promotion from KFC is a classic example.

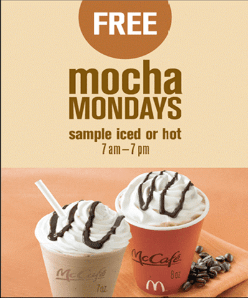

What do you think McDonald's can expect with its new Mocha Mondays promotion? McDonald's is offering a complimentary 7 oz. Iced Mocha or indulge in an 8 oz. Hot Mocha each Monday from 7 a.m. to 7 p.m. at participating McDonald's restaurants from July 13 through August 3.

According to McDonald's "This is one of the largest sampling initiatives we've taken on as a company." It's going to be very interesting to see how this plays out for MCD.

Burger King Holdings Inc. (BKC) appears to be headed down a similar road. The Burger King operators shot down a plan to sell double cheeseburgers for $1 nationwide. Those operators understand the consequences of this move.

The marketing muscle behind these value messages by the larger chains will hurt the little guys more. In this context, CKR will continue to see pressure on its industry leading margins.