Last week Consumer Staples underperformed the broader market, with the XLP +0.4% versus S&P500 +0.8%, continuing a weak start for the sector in 2014, down -4.8% YTD.

The Hedgeye U.S. Consumption Model is flashing predominantly red, as only 4 of the 12 metrics are flashing green.

From a quantitative set-up the sector remains broken across the immediate term TRADE and intermediate term TREND durations, our language for a bearish medium term sector outlook. You’ll see a similar bearish setup for most of the largest names in Consumer Staples.

We continue to believe that the group is generally way over-owned and loaded with premium valuations, despite a healthy moderation in the P/E week-over-week, declining 120bps to 17.7x. Headwinds we see for the group include:

- U.S. consumption growth is slowing as inflation rises, in-line with the Macro team’s 1Q14 theme of #InflationAccelerating

- The economies and currencies of emerging markets – once the sector’s greatest growth engine – remain weak with the prospect of higher inflation in 2014 eroding real growth

- Less sector Yield Chasing as Fed continues its tapering program

- In the U.S., the most recent data on ISM Manufacturing and Prices Paid disappointed month-over-month

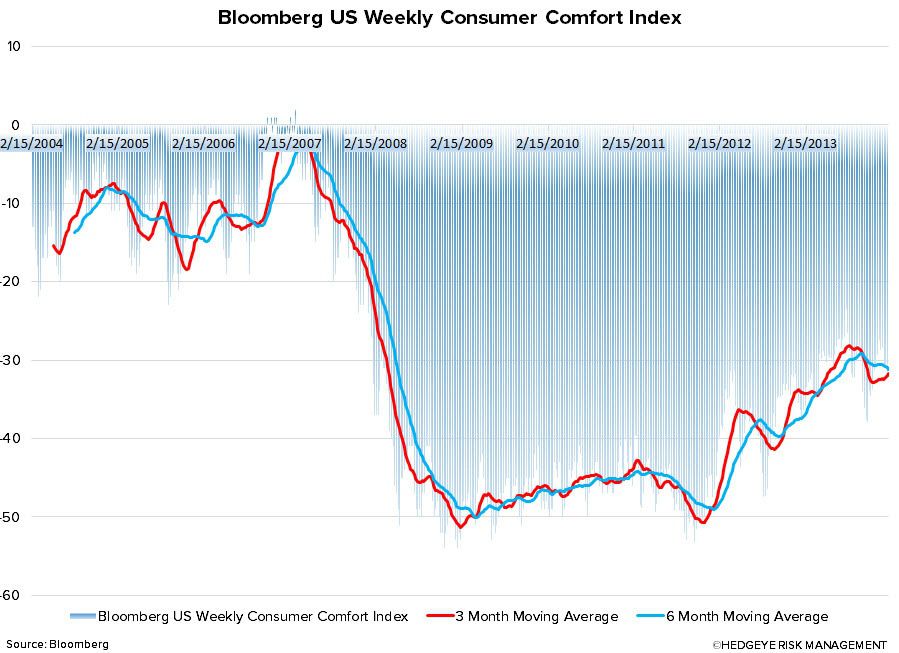

- The high frequency Bloomberg weekly U.S. Consumer Comfort Index has not seen any real improvement over the past 6 months and declined week-over-week

Top 5 Week-over-Week Divergent Performances:

Negative Divergence: NUS -15.6%; FLO -9.8%; HAIN -6.0%; DF -4.6%; HRL -3.7%

Positive Divergence: HLF +4.7%; BNNY +4.6%; CCE +2.6%; DPS +2.1%; BF/B +2.1%

The “Newsy” News Flow:

Coca-Cola and Green Mountain Partnership - last week KO announced it will purchase a 10% minority equity position in GMCR. Under the terms of the equity agreement, KO will acquire 16.7M of newly issued shares in GMCR for approximately $1.25B. KO also revealed a new Keurig cold machine to dispense liquid syrup with built-in carbonation, which it has been working on for 5 years!

- We note that Soda Steam (SODA) has struggled with sales of its non-branded syrups — can branded Coke change the consumer's tide towards syrups? Also, we suspect the need for KO and GMCR to combine their hot and cold systems into one as customers desire the innovation but lack the kitchen cabinet space for two units. Could PEP partner with SODA, or just buy the company outright?

CVS Cuts Tobacco - CVS Caremark announced last week that it will stop selling tobacco products at its more than 7,600 drugstores nationwide by October 1. The Company estimates that it will lose approximately $2 billion in revenues on an annual basis from the tobacco shopper.

- While Big Tobacco is beginning to forecast cigarette volumes down 2-3% in 2014, a moderation from 2013 of ~ -4%, CVS’ decision is a bold one that could be very impactful – namely will Walgreen’s, Duane Reade, and Rite Aid follow along? CVS does not sell electronic cigarettes and said it was waiting for guidance on the devices from the FDA.

Last Week’s Research Notes

Earnings Calls This Week (in EST):

Monday (2/10): BNNY 5pm

Tuesday (2/11): RAI 9am; DF 9am

Wednesday (2/12): LO 9am; DPS 11am; MDLZ 5pm

Thursday (2/13): PEP 8am; JAH 8:30am; AVP 9am; THS 9am; IFF 10am; BG 10am; TAP 11am; KRFT 5pm

Friday (2/14): SJM 8am; CPB 9:30am

Quantitative Setup

In the charts below we look at the largest companies by market cap in the Consumer Staples space from both a quantitative perspective and fundamental aspect where we can offer one. As you will see over time, sometimes our fundamental view does not align with the quantitative setup (though not often).

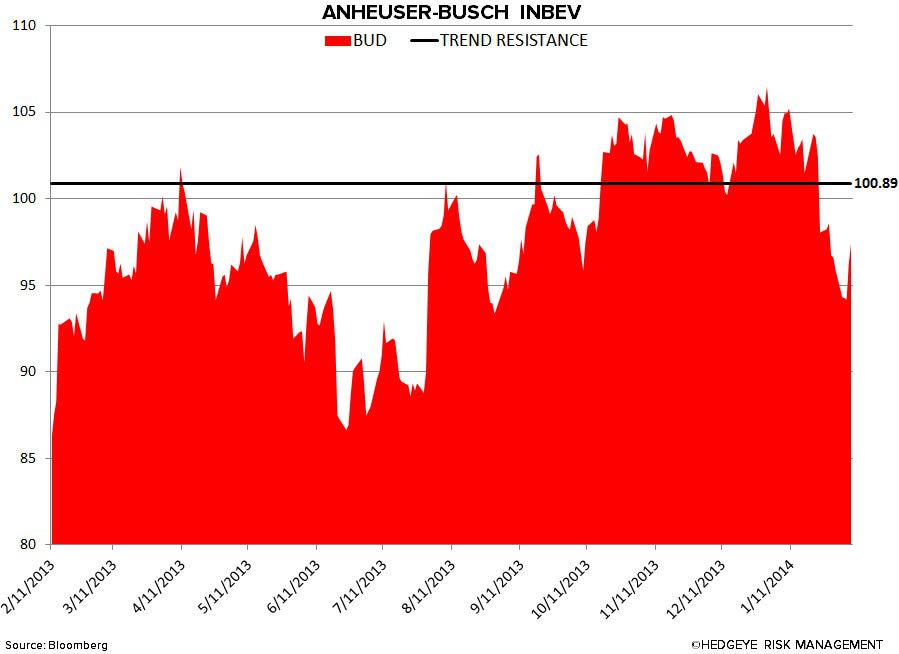

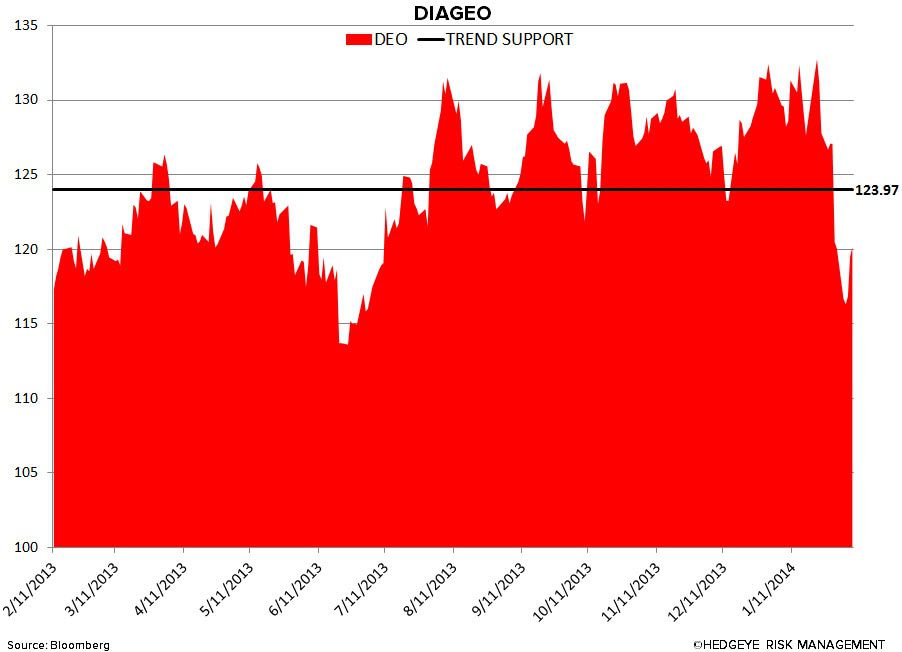

Alcohol

BUD – no-volume (no conviction) beta bounce last week doesn’t do anything to change this bearish TREND ($100.89 resistance)

DEO – one of the new worst looking big cap charts listed in America; never mind the TREND remaining bearish, now the TAIL risk is on here w/ resistance of $123.97

Beverage

KO – outdone by a hair in the downhill crash competition at #Sochi by DEO; bearish TREND resistance remains overhead at 39.74; TAIL risk = #on

PEP – is it the chips? Don’t know but it couldn’t look worse than KO and it doesn’t; bearish TREND remains but holding long-term TAIL risk line of 79.42, barely

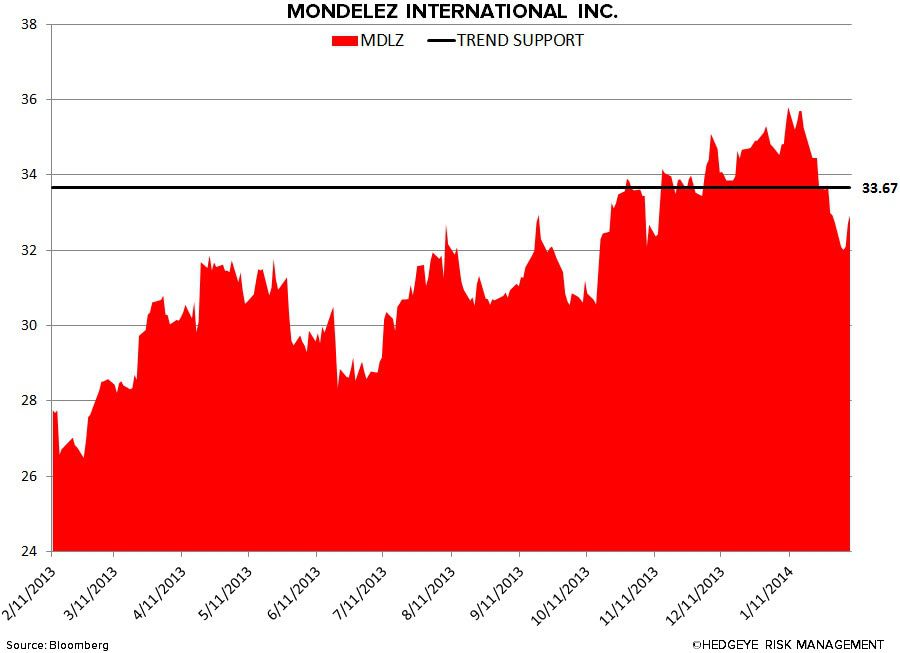

Food

GIS – Cheerios are cool, but the stock still isn’t; bearish TREND resistance as intact as a bowl without milk up at $49.98

MDLZ - the name of the company is turning out to be as unimpressive as the stock sans Peltz renaming it; TREND support now resistance at $33.67

Household Products

KMB – don’t cry for me Argentina – your KLEENEX is the only signal on our screen that absorbs the bullish TREND support of $103.43

PG – good Mom commercials at the Olympics, bad stock; bearish TREND @Hedgeye firmly intact up at $79.99

Tobacco

MO – dogs bounce too, eh? Altria is earning its newfound bearish TREND with resistance up at 36.29

PM – dog breath.com remains – bouncing big last week on no-volume gets this puppy a biscuit too; TREND resistance firmly intact up at 85.16

Matt Hedrick

Food, Beverage, Tobacco, and Alcohol

Howard Penney

Household Products

(o)