This note was originally published at 8am on January 24, 2014 for Hedgeye subscribers.

“If we lack emotional intelligence, whenever stress rises the human brain switches to autopilot and has an inherent tendency to do more of the same, only harder. This, more often than not, is precisely the wrong approach in today’s world.”

- Robert K. Cooper PhD

Robert Cooper is a neuroscientist and strategic advisor to CEOs and many Fortune 500 companies. Taking on the work that Dr. Cooper requires is certainly not easy. According to Cooper, your brain is organized to reflect everything you know in your life. Or, in other words, your brain is a record and an artifact of your past.

Consistent with this line of thought, Cooper poses the following question: Does your environment control your thinking or does your thinking control your environment?

To help you ponder, we ask the following questions:

- What does your daily routine look like?

- Did you wake up today and hop out of bed on the same side?

- Did you shut your alarm off with the same hand?

- Did you go to the bathroom like you always do?

- Did you shower and follow the same grooming routine?

- Did you dress the way your coworkers expect you to dress?

- Did you follow the same breakfast routine and do you get angry when the morning commute to work is just slightly off the normal pace?

I’m sure many of you will find that you often revert back to a routine in life you are comfortable with or, in Layman’s terms, the same-old, same-old life. This is considered living life inside your box and it is much more prevalent among us and our colleagues than we’d like to acknowledge.

Admittedly, this may be too much philosophical thinking for a Friday morning. But, the metaphor of switching to autopilot during rising levels of stress could be the norm for a CEO whose company you have invested hundreds of millions of dollars in and whose stock is underperforming. Isn’t this a scary thought? What if this routine keeps him/her in survival mode and prevents him/her from making the right decisions for the company he/she is running?

Back to the Global Macro Grind…

I often refer to this decision making process in the restaurant space as the “6 Stages of Grief.” This is a cycle that some companies tend to go through before they can see life outside the box. As I see it, today’s activist investors provide a version of neurological therapy for this grief.

Unfortunately, the news of an activist investor can actually provoke a series of decisions based on past experiences that might be inconsistent with what is appropriate for today’s environment. When an activist investor arrives on the scene, it’s only natural that “as stress rises, the human brain switches to autopilot and has an inherent tendency to do more of the same, only harder.”

Whether it’s a letter from Dan Loeb saying you’re an idiot or a letter that says “we look forward to maintaining an open dialogue and working with you to ensure that value is created for all shareholders,” either one could put management on the defensive and get them to react in ways that could potentially destroy shareholder value.

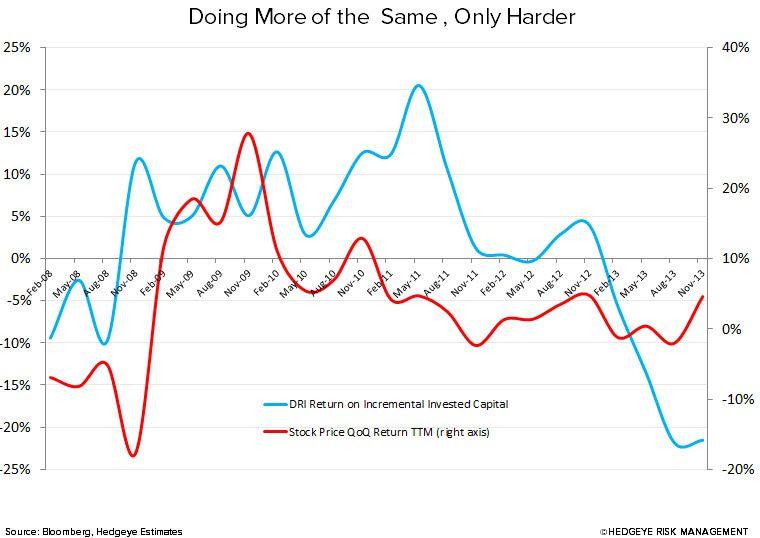

Sadly, this is precisely the path of destruction that the CEO of Darden Restaurants is headed down.

As I said earlier this week, the challenge for the Board members of Darden (or any Board) is to recognize the appropriate time to step up, break out of their box, and implement meaningful change. It is their challenge, their job, and their responsibility not to be more of the same.

When a Board works closely with a CEO for a number of years, the best interest of shareholders’ can become fuzzy. As an outsider, it appears that this is the case with the current Board and Chairman/CEO Clarence Otis. The operational performance of DRI has stagnated and it is, without question, time for a significant change.

As Keith said in yesterday’s Early Look, we are short a significant number of restaurant names. On yesterday’s earnings call, the CEO of Starbucks, Howard Schultz, went out of his way to emphasize the decline in bricks and mortar retailing. Starbucks was wisely in a position to win in this environment. Mr. Schultz is a great example of a CEO, at least in my space, that is willing to take on the difficult task of recognizing when and where he can strengthen his company.

To be honest, I welcome the commentary about bricks and mortar retailing as it relates to my short call on CAKE. My original thesis was shorter term, but his comments could make our bearish call on CAKE more secular in nature. In the short run, however, we believe the price spikes in the dairy complex are unaccounted for and suggest that EPS estimates are too aggressive for the company in 2014.

Moving on to a broader concept, the biggest risk to the consumer and restaurant space in 2014 is our MACRO theme of #InflationAccelerating. The CRB Index, milk, cheese, natural gas, cattle, hogs and coffee are all up more than the S&P 500, as gold continues to signal higher lows. With the Bloomberg Consumer Confidence Index flat week over week at -31, sluggish Per Capita Disposable Income, and a stagnant job market, it could be challenging for most companies to take price in order to offset inflation.

The irony of all this is that one of the few names I like on the long side is Darden Restaurants. The CEO’s tendency is to do more of the same, only harder. While I’m typically not a proponent of this line of action, it has indeed created a significant opportunity for a lot of money to be made.

It has also provided me with the material for a scathing attack on what has arguably been the largest case of value destruction in Casual Dining history. For the record, if you’re reading this Mr. Loeb, I have everything you could possibly need to write your best letter yet.

Function in disaster, finish in style.

Howard Penney

Managing Director