“After the fight is over the winning animal emerges with even higher levels of testosterone.”

-John Coates

The thing about fighting bulls are those damn horns. No matter what the math, data, or weather, the perma ones are really stubborn too. They’ll just sit there sometimes and stare at you. So, when you’re a bear, it’s better to attack them from behind.

The aforementioned quote comes from a chapter in The Hour Between Dog and Wolf that John Coates calls The Fuel of Exuberance. “Biologists studying animals in the field had noticed that an animal winning a fight or a competition for turf was more likely to win its next fight” (pg 166).

Sounds like trending bullish and bearish price momentum to me. All our back-tests show the most powerful ramps in market emotion (fear and greed) occur when there is a reversal from bearish to bullish (or bullish to bearish) on our intermediate-term TREND duration. In other words, bear vs. bull fights matter; especially at the big TREND turns.

Back to the Global Macro Grind…

From a #behavioral market strategy perspective, does the “Winner Effect” (Coates) matter? Big time. Why? It especially matters in modern markets because, newsflash: machines chase price.

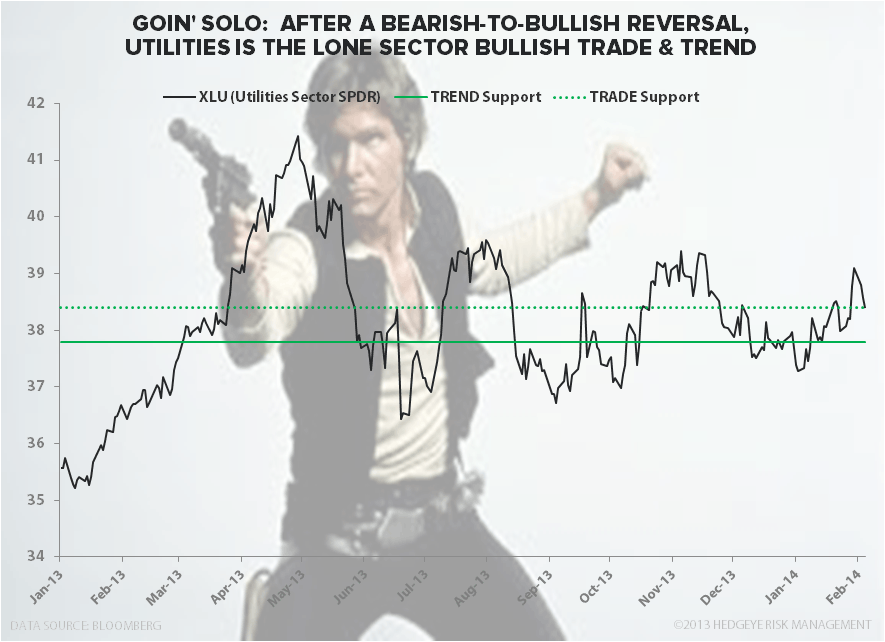

What are the most interesting bullish-to-bearish reversals in the @Hedgeye quant model right now?

- Nikkei reversing to bearish TREND

- SP500 reversing to bearish TREND

- 10yr US Treasury Yield reversing to bearish TREND

How about the most interesting bearish-to-bullish reversals in TREND?

- Commodities (CRB Commodities Index) reversing to bullish TREND

- Utilities (XLU) reversing to bullish TREND

- Fear (VIX) reversing to bullish TREND

From a Global Macro Theme perspective it’s easy to explain why all 6 of these intermediate-term TREND reversals rhyme: with #InflationAccelerating, growth expectations in Japan and the US are slowing.

These same risk management signals started to manifest in Q1 of 2008 (that’s why we got so bearish on the US consumer back then), but they also started to coagulate again in Q1 of 2011.

2011 was a very interesting year in that while US stocks (SP500) closed flat on the year:

- Fear (VIX) ripped from 15 to 24 in Q1 of 2011

- Utilities (XLU) and Treasuries (TLT) marched steadily higher (relative and absolute) throughout 2011

- Commodities (CRB Index) had a monster Q1 of 2011

Fast forward to mid-Q1 of 2014 and here’s the score:

- Nikkei -13.1% YTD

- SP500 -5.2% YTD

- US Treasuries (TLT) +5.2% YTD

- CRB Commodities Index +2.5% YTD

- Utilities (XLU) +1.1% YTD

- Fear (VIX) +45.4% YTD

Just saying.

Oh, and there was that “financial innovation” thing (a Policy to Inflate asset prices; especially Bonds and Commodities) that eventually caused the all-time highs in commodities like Gold in Q3 of 2011 called the quantitative easing…

So, play it forward – what do you think the Mother of All Doves (Yellen) is going to do if US growth continues to slow? Bernanke didn’t go to Jackson Hole last year, but I’m betting that she’ll strap on the cowboy pants and start printing again.

I know, Hilsenrath hasn’t leaked that probability memo to the bulls or bears yet. But Mr. Macro Market has. So keep your head on a swivel out there as these currency devaluation and money printing animals at the Federal Reserve still think they’re winning.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1

Nikkei 132

VIX 15.81-20.41

USD 80.93-81.46

NatGas 5.05-5.51

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer