TODAY’S S&P 500 SET-UP – February 4, 2014

As we look at today's setup for the S&P 500, the range is 48 points or 0.40% downside to 1735 and 2.36% upside to 1783.

SECTOR PERFORMANCE

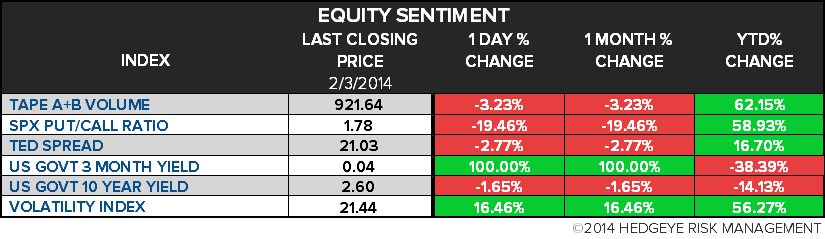

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.30 from 2.28

- VIX closed at 21.44 1 day percent change of 16.46%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45/8:55am: ICSC/Redbook weekly retail sales

- 9:45am: ISM New York, Jan. (prior 63.8)

- 10am: Factory Orders, Dec., est. -1.8% (prior 1.8%)

- 10am: IBD/TIPP Economic Optimism, Feb., est. 44.5 (pr 45.2)

- 10am: CBO releases U.S. economic outlook

- 8:30am: Fed’s Lacker speaks in Winchester, Va.

- 12:30pm: Fed’s Evans speaks in Detroit

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- 10am: CBO releases U.S. economic outlook

- 10am: Sen. Homeland Security Army recruiting contract hearing

- 10am: Senate environmental panel on water supply safety post-W. Va. contamination

- 10:15am TGT CFO John Mulligan at Senate Judiciary Cmte

- 10:30am: Moody’s Chief Economist Mark Zandi on 2014 outlook at Senate Budget Cmte

- 1:30pm: House Oversight and Govt Reform Cmte hearing on Obama admin marijuana policy

WHAT TO WATCH:

- Yum profit beats ests. on growth in international division

- Intel changes pay rules in seeking closer ties to performance

- Symantec says facing $145m in damages in U.S. probe

- TV shared ownership led by Sinclair said to get U.S. scrutiny

- Second storm of week bound for U.S. Northeast with icy snowfall

- BP 4Q profit drops as disposals hurt oil output

- UBS 4Q net beats estimates on wealth management, tax gain

- Toyota forecasts record annual profit as yen boosts exports

- BofA bonuses for rates traders are said to drop at least 15%

- Genfit seeks U.S. alliance for non-alcoholic liver ailment

- Drug cos. join NIH in study of Alzheimer’s, other diseases: WSJ

- House GOP said to finalize debt-limit strategy: WPost

- Lockheed Martin to begin production of civilian Hercules: WSJ

- Anadarko fails to find viable oil at first N.Z. well: TV3

AM EARNS:

- Affiliated Managers Group (AMG) 7:10am, $3.09

- AGCO (AGCO) 8am, $1.34

- AGL Resources (GAS) 8am, $0.91

- Arch Coal (ACI) 7:30am, ($0.38) - Preview

- Archer-Daniels-Midland Co (ADM) 7am, $0.84

- Becton Dickinson (BDX) 6am, $1.29

- Bell Aliant (BA CN) 6am, $0.35

- Boston Scientific (BSX) 7am, $0.13 - Preview

- Clorox (CLX) 830am, $0.91 - Preview

- CME Group (CME) 7am, $0.67

- Delphi Automotive PLC (DLPH) 7am, $1.04

- Eaton (ETN) 6:30am, $1.06

- Emerson Electric (EMR) 6:30am, $0.67 - Preview

- Fidelity National Information (FIS) 7am, $0.78

- Gannett Co (GCI) 830am, $0.65

- HCA Holdings (HCA) 8:29am, $0.86 - Preview

- IDEXX Laboratories (IDXX) 7am, $0.81

- International Paper Co (IP) 7am, $0.86

- McGraw Hill Financial (MHFI) 7:10am, $0.79

- Michael Kors Holdings (KORS) 7am, $0.86 - Preview

- Ryder System (R) 7:55am, $1.29

- Sensata Technologies (ST) 6am, $0.55

- Sirius XM Holdings (SIRI) 7am, $0.02

- Spectra Energy (SE) 6:30am, $0.38

- UDR (UDR) 8am, ($0.01)

- Vishay Intertechnology (VSH) 7:30am, $0.19

- Westjet Airlines (WJA CN) 6:30am, $0.52 - Preview

- Xylem (XYL) 7am, $0.52

PM EARNS:

- Aflac (AFL) 4:15pm, $1.39

- Ameriprise Financial (AMP) 4:05pm, $1.81

- Axis Capital Holdings (AXS) 4:05pm, $1.47

- Cerner (CERN) 4:01pm, $0.39 - Preview

- CH Robinson Worldwide (CHRW) 4:15pm, $0.68

- Covance (CVD) 4:01pm, $0.84

- Genworth Financial (GNW) 4:30pm, $0.30

- Gilead Sciences (GILD) 4:05pm, $0.51 - Preview

- Hain Celestial (HAIN) 4pm, $0.87

- Macerich (MAC) 4:30pm, $0.23

- Mueller Water Products (MWA) 4:20pm, $0.00

- Myriad Genetics (MYGN) 4:05pm, $0.46 - Preview

- RenaissanceRe Holdings (RNR) 4:16pm, $2.78

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Rises From One-Week Low Amid Cushing Pipeline Start

- Gold Declines in London on Signs Physical Demand Is Slowing

- Arabica Coffee Posts Biggest Gain Since 2004 on Brazil Drought

- Cotton Crop Expanding After Corn Slump Spurs Switch: Commodities

- Lead Paces Gains by Metals Amid Speculation Decline Was Overdone

- Soybeans Extend Gain on Concerns Brazil Dryness May Curb Yields

- Natural Gas Rebounds as Winter Storm Spreads in U.S. Northeast

- Rubber Declines to 17-Month Low as U.S. Factory Growth Slows

- Krung Thai Bank Won’t Lend to Government Rice Program: President

- Platinum Mine Strike Costs $36 Million a Day as Talks Resume

- Commodity Volatility Drops as Equities Swing: Chart of the Day

- Fukushima Wash-Up Fears in U.S. Belie Radiation Risks: Energy

- Senators to Vote on Farm Law That Keeps Their Benefits Secret

- Robusta Coffee Rises to 5-Month High on Lack of Vietnam Selling

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team