Perhaps the discrete tanking in the Jan ISM Manufacturing data was due to the weather as some ISM respondents intimated (comments below).

Or, perhaps, after binging on a GDP juicing inventory build in 2H13, we get to deal with the hangover to start 1Q14 as the weaker, concomitant rise in household income proves insufficient for expeditiously drawing down that burgeoning goods stock.

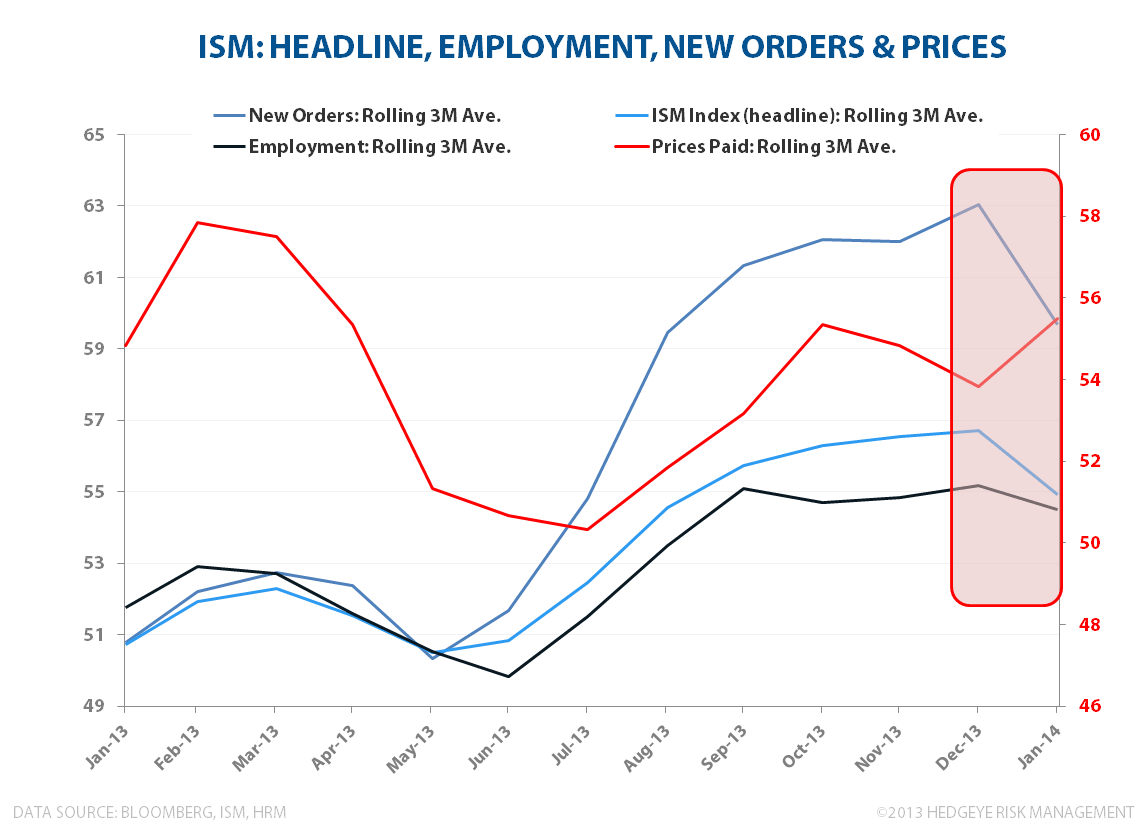

Today’s ISM manufacturing data for January serves as a solid microcosm for our view of the broader macro dynamics as New Orders rolled over (#GrowthSlowing) alongside a material acceleration in Prices Paid (#InflationAccelerating).

Headline ISM dropped 5.2 pts sequentially to 51.3 with softness pervasive across the sub-indices as Production, New Orders, Employment and Backlogs all declined in January while Prices Paid jumped above 60 for the first time in a year. Most notably, New Orders declined from 64.4 in December to 51.2 in January – the largest MoM decline since December 1980.

We’ve been fairly vocal on our expectation for a sequential move into Quadrant #3 – Growth Decelerating as Inflation Accelerates - in our GIP (Growth/Inflation/Policy) model for the U.S. economy and how to play that from a positioning perspective. Please see the links below to our 1Q14 Macro Investment Themes call and recent update notes for additional detail .

NO SILVER LININGS: DECEMBER DURABLE GOODS

MAKING SENSE OF EQUITY STYLE FACTORS YTD

In short, we turned increasingly more bearish in 1Q14 as the price signals broke down (see: Not #BTDB Today: SP500 Levels, Refreshed) and the domestic fundamental macro data began slowing on the margin (See Eco Summary Table below). Incremental, growth-slowing data over the last few weeks has served to further confirm that price signal.

We started the week net short in Real-Time Alerts and aren't overly keen on attempting to catch the knife here this morning.

ISM Services, Employment and Debt Ceiling on Deck. Keep Moving.

ISM RESPONDENT COMMENTARY (JAN.):

Christian B. Drake

c

@HedgeyeUSA