“Welcome to game day… Now it’s real. The score counts. And you either win or lose.”

-John Hamm

That’s how golf and life coach John Hamm opens Part Two of Unusually Excellent: Competence – Leading on the Field With Skill. Russell Wilson did just that last night. Seahawks 43 vs. Broncos 8.

Credibility, Competence, and Consequence – per Hamm’s framework, that’s the epicenter of leadership skill. And since I can’t argue with that, I like it.

Note that in this game there is no credibility in A) cheating and/or B) making a few big “calls.” Credibility is scored in our profession by repeatable processes. If you can score in both up and down markets, you win. So let’s get at it this morning and try to do more of that.

Back to the Global Macro Grind…

What’s winning so far in 2014 is not what was winning for most of 2013. That’s because:

A) Global Inflation is no longer deflating, it’s re-flating

B) Growth (particularly in the US and across most of Asia) is slowing, not accelerating

On the Asian #GrowthSlowing scene, China’s manufacturing PMI came in at 50.5 (which is a six month low) and non-manufacturing PMI came in at 53.4, lowest reading since December 2008.

All of this, of course, will be reported to you by the ultimate lagging indicators (your central bankers and consensus economists paid by Big Government), on a lag. So keep it here, where Game Day happens every morning at 4AM.

In terms of our Top Global Macro Theme for Q114, #InflationAccelerating:

- CRB Commodities Index (19 Commodities) = +0.3% last wk to +1.1% YTD (vs SP500 -3.6%)

- CRB Commodities Foodstuff Index = +1.1% last wk to +3.3% YTD

- Corn +1.0% last wk to +2.8% YTD

- Cocoa +4.3% last wk to +7.5% YTD

- Coffee +9.4% last wk to +13.1% YTD

So we hope you enjoyed flipping out of some of that long-term Starbucks (SBUX) idea and into some CAFÉ (the coffee ETN). One’s price is winning YTD; one’s is losing.

On the #GrowthDivergences front (Hedgeye Macro Theme #2) YTD:

- Russell2000 (IWM) -2.8% vs. Utilities (XLU) +2.98%

- Emerging Markets (MSCI Equities Index) -6.6% vs. Europe (EuroStoxx600) -1.7%

- Japanese stocks (Nikkei) -10.3% vs. Danish stocks (Copenhagen Index) +5.2%

In other words, being long inflation expectations (particularly via breakevens or food inflation) is crushing it YTD, and so is being long European Equity exposure relative to the slowing growth exposures you could be long in the USA or Japan.

That’s not to say that the score may not continue to trend this way. You can make that change in momentum bet this morning if you’d like. You could have doubled down on the Denver Broncos when they were down 22-0 last night too.

Competence in risk management starts the way Seattle started last night; with their defense scoring a safety! Not getting scored on in this game is easily the best way to win. If your shorts can generate positive P&L, all the better.

From a Style Factoring perspective in US Equities, here’s what’s getting lit up like Denver’s defense did:

- Consumer Discretionary Stocks (XLY) -1.1% last wk to -6.0% YTD

- High Beta Stocks (by S&P quartile ranking in our model) -4.5% YTD

- High Short Interest Stocks (again, by quartile) -4.1% YTD

In other words, if you’re overweight any of these Style Factors in a US Equity only portfolio, that’s bad. This is what we call a bullish to bearish reversal in big beta!

But as the game goes on, the score makes more and more sense. With #InflationAccelerating, who gets hurt the most? The Consumer. But don’t tell the Fed that. If growth continues to slow, Janet Yellen’s 1st move will probably be to stop tapering (i.e. devalue the Dollar) and perpetuate more purchasing power pain on The People.

If you don’t like that game recap, go buy another house – and like it. Because, like Barney Frank, Janet Yellen is big on housing, irrespective of it being the mother of all bubbles that got the US consumer into this savings mess to begin with.

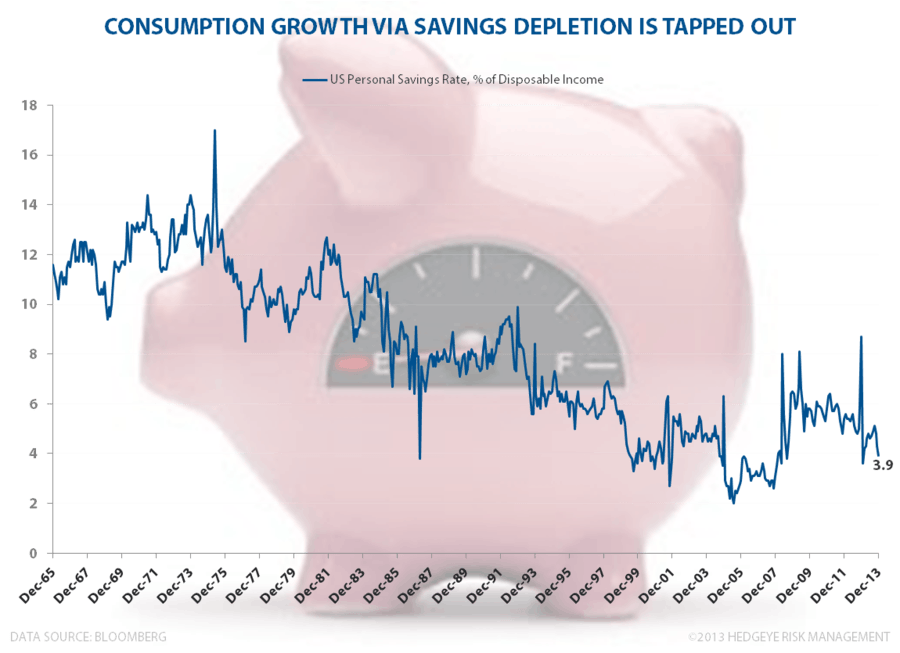

Got Savings? At 3.9% (current US Savings Rate as a % of Disposable Income – see Chart of The Day), Americans are once again dipping into those in order to keep up with their over-spending neighbors (and the government’s understated cost of living).

But no worries, Game Day for the government will include some cochamamy narrative about “inequality” in America while they dream up the next currency devaluation policy to encourage The People to lever up again. If they go for it, the score of that policy will count too – and this time the Keynesians will lose as big as the Broncos did.

Our immediate-term Risk Ranges are now (Our Top 12 Global Macro Ranges are in our Daily Trading Range product):

Nikkei 142

VIX 15.89-20.41

EUR/USD 1.35-1.37

NatGas 4.57-5.41

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer