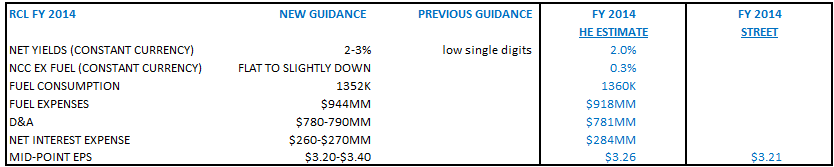

In an effort to evaluate performance and as a follow up to our YouTube, we compare how the quarter measured up to previous management commentary and guidance

OVERALL:

-

MIXED: 2014 is a mixed picture for RCL as suggested by our cruise survey: stronger Europe, weaker Caribbean. 2014 net yield guidance was solid but not surprising. We see CCL as the better bet as pricing particularly in the Caribbean looks more robust than RCL in early Wave 2014.

EUROPE

- BETTER: Surge in close-in bookings for Q4 pushed net yields higher than expected. Mgmt more optimistic on Europe. Strong NA sourced demand continues to lead the way for the European cruise market. For European-sourced European demand, they're generally meeting expectations.

- PREVIOUSLY:

- Early bookings for the overall Europe portfolio had been very encouraging, with our load factors trending ahead of last year in the mid single-digit range and higher ticket per diem for every month of the season.

- We're seeing a little bit of a comeback in Southern Europe and Germany.

CARIBBEAN

- WORSE: 2014 net yields are forecasted down low single digits, lower than the previous forecast of flat to slightly down. Higher capacity playing a role. Longer-dated itineraries performing better than shorter-dated ones.

- PREVIOUSLY:

- We've acknowledged as the Caribbean is of particular concern. Despite this, our more premium Caribbean products, including the Oasis-Class ships and the Solstice Class ships continue to enjoy superior pricing and are delivering good returns. As a result, based on our early bookings, we expect our core Caribbean yields to be roughly flat to down slightly in 2014.

- We look forward to the Caribbean returning to better pricing.

- our Caribbean yield change this year over last year and our preliminary Caribbean yield change outlook for 2014 are roughly equal.

- While we expect to maintain a high level of focus on driving revenue on all of our Caribbean products, in general, we see more competitive pressure in the near term in South Florida than in other Caribbean homeports.

ASIA

- BETTER: Territorial dispute between China and Japan remains a wild card. However, Asian/Australian bookings are up considerably in 2014.

- PREVIOUSLY:

- For 2014, we have opened up our sailings for booking, once again, based on itineraries offering exclusively Korean destinations. This is, of course, frustrating, particularly since we do not see any signs of positive geopolitical change in the dynamic between China and Japan.

- Our capacity increase in Asia in 2014 will be just over 20%, which primarily reflects a full-year capacity upgrade from Legend of the Seas to Mariner of the Seas, that occurred in May of this year.

PULLMANTUR

- SAME: Mgmt recognized the weakness in the brand but sees a brighter future ahead. 2014 will be a transitional year. Mgmt expects the biggest benefits of Pullmantur's changes to occur in 2015 and beyond.

- PREVIOUSLY: Pullmantur has faced the toughest operating environment of any of our brands, and they've worked hard to overcome the huge obstacle that they have faced.

COMPETITIVE PRICING/PROMOTIONAL ACTIVITY

- SAME: Discounting remains prevalent and very competitive during Wave Season.

- PREVIOUSLY: Heighted promotional activity is centered mostly around short excursions in the Caribbean. Pricing in the Caribbean remains very competitive.

2014 BOOKINGS

- SAME: Bookings are 5% higher than same time last year. APDs up in all four quarters. Loaded factor flat in 1Q but up in 2Q, 3Q, and 4Q.

- PREVIOUSLY:

- We are currently booked ahead of same time last year in both APD and load factor.

- Our comparables become a little bit easier going forward.

- New booking volumes since our last call have averaged about 5% higher than during the same period last year, and our average booking window has extended slightly.

- Caribbean yields are expected to be flat to slightly down year-over-year.

- Europe is expected to have a second year of strong yield improvement.

- Healthy yield growth is expected in Asia

- Expect moderate growth from the already high-yielding Alaska program.

2014 NCC EX FUEL

- SAME: 2014 guidance issued for 'flat to slightly down'.

- PREVIOUSLY: Just to reiterate on the cost side, our expectations on costs are for them to be better than flat in 2014,

ONBOARD YIELD

- BETTER: Onboard again outperformed -across all categories and markets. Onboard yields were up 8% in 4Q. Mgmt expects +2-3% onboard yields for 2014.

- PREVIOUSLY:

- We benefited from new onboard venues introduced as a result of our revitalizations. And we saw further strength in spending from our U.S. customers, which helped generate improvement in gaming, beverage, specialty dining and shore excursions.

- Onboard is obviously expected to go up but tempered relative to 2013

CELEBRITY

- WORSE: While still optimistic on Alaska, mgmt commentary was more guarded.

- PREVIOUSLY:

- Demand for European itineraries has been very strong from all of our core markets, including the United States and the United Kingdom and Ireland. And we are well positioned for another year of yield growth.

- Alaska has been a solid performer for us over the past couple of years, and we've been maintaining similar yields to those achieved during our record 2011 season. Bookings and pricing for 2014 Alaska sailings have been trending ahead of last year, and we are anticipating further yield growth for the season. Both Alaska and Europe products operate during our crucial Q2 and Q3 peak seasons and early indications for 2014, as their performance is shaping up very nicely.