TODAY’S S&P 500 SET-UP – January 24, 2014

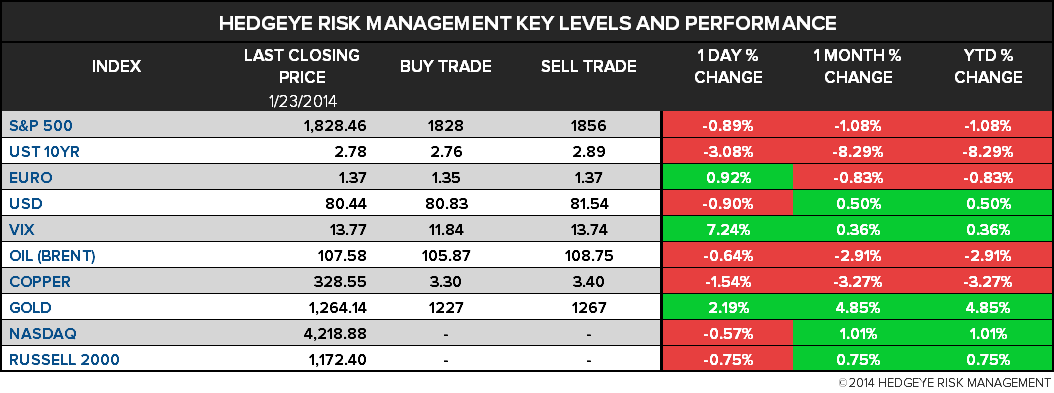

As we look at today's setup for the S&P 500, the range is 28 points or 0.03% downside to 1828 and 1.51% upside to 1856.

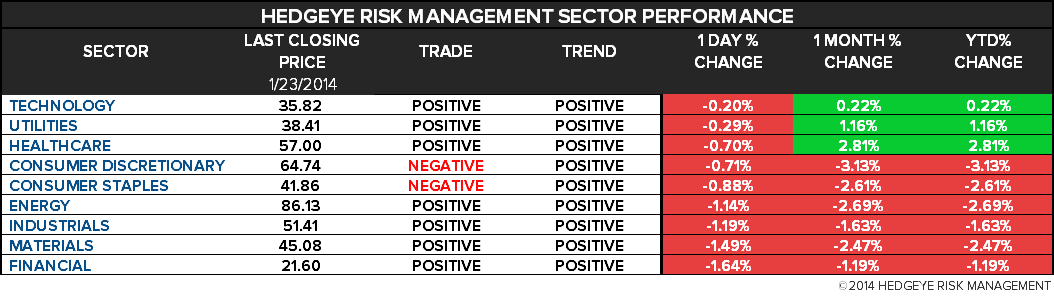

SECTOR PERFORMANCE

*Levels as of 1/23/14

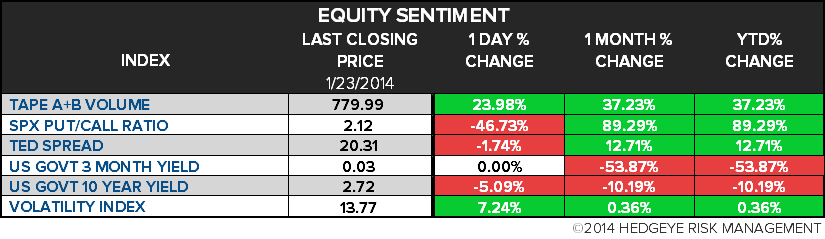

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.40 from 2.42

- VIX closed at 13.77 1 day percent change of 7.24%

MACRO DATA POINTS (Bloomberg Estimates):

- No major data releases

- 7:05am: BoE’s Carney speaks at Davos

- 12pm: ECB’s Draghi speaks at Davos

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Sec. of State John Kerry attends talks on Syria in Montreux

- Treasury Sec. Jack Lew, Commerce Sec. Penny Pritzker attend Davos

- House not in session, Senate meets in pro forma session

- 10:30am Chairman Reince Priebus addresses Republican National Cmte winter meeting

- 11:30am Homeland Security Sec. Jeh Johnson speaks at U.S. Conference of Mayors winter meeting

- 1:30pm Gov. Rick Snyder, R-Mich.; former NYC Mayor/Bloomberg LP founder Michael Bloomberg discuss economic case for immigration reform

WHAT TO WATCH:

- Samsung profit growth slows as iPhones win sales, won gains

- Ziggo says talks to be taken over by Liberty making progress

- Starbucks sales trail estimates as U.S. growth decelerates

- McKesson to purchase Celesio in deal after earlier offer failed

- China bank regulator said to issue alert on coal mine loans

- Qualcomm acquires patents from Hewlett-Packard, including Palm

- JPMorgan’s Jamie Dimon said to get increased compensation: NYT

- Morgan Stanley gives Gorman $5.06m of shares for 2013

- Jana partners takes big stake in Juniper: Reuters

- Goldman may ban some person-to-person instant messaging: WSJ

- BofA may buy own stake held by Korea Investment Corp: Maeil

- Boeing to give ANA order discounts as 787 compensation: Nikkei

- CNN says some of its social media accounts were compromised

- AT&T unlikely to bid for Vodafone in near-term, Oriel says

- U.S. says no leeway in Iran oil exports based on inflated data

- FOMC, Yellen, Obama’s address, Egypt: Week Ahead Jan. 25-Feb. 1

EARNINGS:

- Bristol-Myers Squibb Co (BMY) 7:30am, $0.43 - Preview

- Covidien PLC (COV) 6am, $0.94 - Preview

- First Niagara Financial Group (FNFG) 7:15am, $0.20

- Honeywell International (HON) 7am, $1.21 - Preview

- Kansas City Southern (KSU) 8am, $1.10

- Kimberly-Clark (KMB) 7:30am, $1.39 - Preview

- Procter & Gamble Co/The (PG) 7am, $1.20 - Preview

- Stanley Black & Decker (SWK) 6am, $1.30

- State Street (STT) 7:30am, $1.19 - Preview

- WW Grainger (GWW) 8am, $2.62 - Preview

- Xerox (XRX) 7am, $0.29

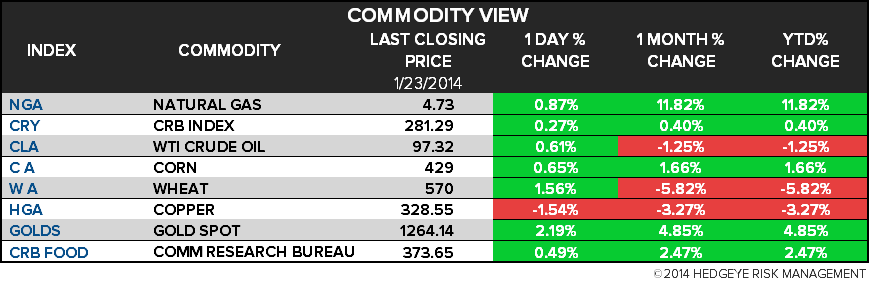

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Natural Gas Set for Biggest Weekly Gain Since 2012 on U.S. Cold

- Brent Slumps as Premium to WTI Narrows to Least in Two Months

- Big Data From U.S. Cornfields Spurs Farmer Concerns: Commodities

- Copper Trades Near One-Month Low Amid China Credit-Risk Concern

- Wheat Snaps Seven-Week Slump as Freezing U.S. May Harm Crops

- Gold Extends Gains in London, Rising to Highest Since November

- Libya Oil Growth Crimped as Gunmen Block Eastern Port Hariga

- Cocoa Advances as Lower Reserves Add to Shortage; Coffee Falls

- Rebar Rises for First Week in Seven After China Money Rates Drop

- Platinum Talks Today Will Seek End to Pay Strike Crippling Mines

- Colder Weather Forecast for U.S. as Freeze Brings Texas Ice

- Vitol to Trafigura Chasing U.S. NGLs as Traders Cash In: Energy

- Curtailment, Trucks, Contracts Are Aluminum Themes: 2014 Outlook

- Super Bowl Fans Eat 1.25 Billion Wings as Corn Crop Lowers Costs

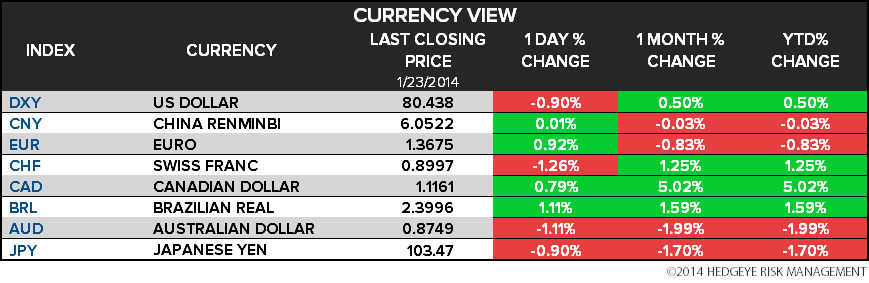

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team