TODAY’S S&P 500 SET-UP – January 22, 2014

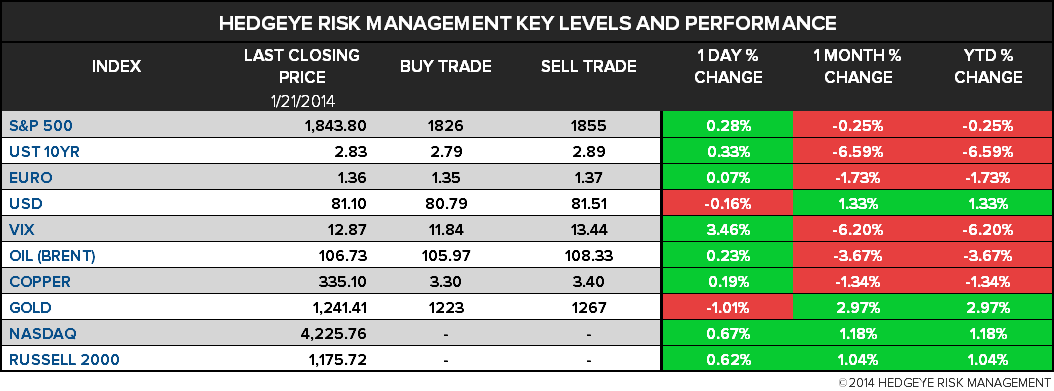

As we look at today's setup for the S&P 500, the range is 29 points or 0.97% downside to 1826 and 0.61% upside to 1855.

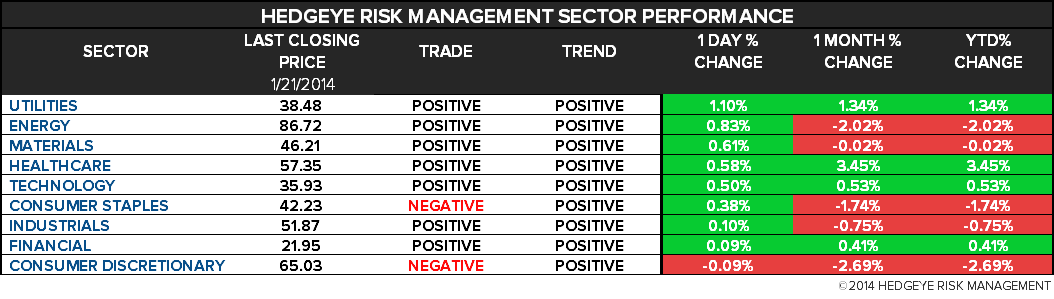

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.46 from 2.45

- VIX closed at 12.87 1 day percent change of 3.46%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Jan. 17 (prior 11.9%)

- 7:45am/8:55am: ICSC/Redbook weekly sales

- 4:30pm: API weekly oil inventories

GOVERNMENT:

- House, Senate not in session

- FCC begins first major airwaves auction since 2008, selling licenses nationwide for frequencies suited for use by smartphones, tablets; Dish Network has pledged to bid at least $1.56b to ensure sale’s success

- 12:30pm: NASA teleconference on agency’s Earth science activities planned for 2014

WHAT TO WATCH:

- BlackBerry to sell most of Canadian real estate to raise cash

- ABB says profit reduced by $260m in power systems charges

- Discovery seeks sports rights with control of Eurosport

- Amazon said to seek content rights to start Internet TV service

- Floating notes debut in US as more cash chases fewer securities

- Banks seen taking on European debt amid lingering problems: NYT

- Gross heir-apparent El-Erian quits as Pimco fights redemptions

- Bitcoin no bargain for investors with 47% bearish in poll

- Nokia investors call for rewards as Microsoft proceeds loom

- Dow Jones said to dismiss CEO Fenwick amid slow demand for DJX

- BHP quarterly iron ore production narrowly misses forecast

- Bank of Japan sticks to record easing as inflation picks up

- China money rate drops as PBOC cash injections spur stocks gain

- World Economic Forum meeting in Davos coverage

AM EARNS:

- Abbott Laboratories (ABT) 7:44am, $0.58 - Preview

- Allegheny Technologies (ATI) 7am, $(0.21)

- Amphenol (APH) 8am, $0.98

- Brinker Intl (EAT) 7:45am, $0.58 - Preview

- Coach (COH) 7am, $1.11 - Preview

- Freeport-McMoRan (FCX) 8am, $0.80 - Preview

- General Dynamics (GD) 7am, $1.75 - Preview

- Motorola Solutions (MSI) 7am, $1.62

- Northern Trust (NTRS) 7:30am, $0.75 - Preview

- Parker Hannifin (PH) 7:30am, $1.25 - Preview

- St Jude Medical (STJ) 7:30am, $0.99 - Preview

- TE Connectivity (TEL) 6am, $0.77

- Textron (TXT) 6:30am, $0.59

- United Technologies (UTX) 6:59am, $1.53 - Preview

- US Bancorp (USB) 7am, $0.75 - Preview

- Norfolk Southern (NSC) 8am, $1.51 - Preview

PM EARNS:

- BancorpSouth (BXS) 4:01pm, $0.28

- Crown Castle Intl (CCI) 4:01pm, $0.16

- East West Bancorp (EWBC) 5:02pm, $0.55

- eBay (EBAY) 4:15pm, $0.80 - Preview

- Jacobs Engineering (JEC) 8:28pm, $0.74

- Netflix (NFLX) 4:05pm, $0.66 - Preview

- Noble (NE) 5pm, $0.81

- Polycom (PLCM) 4:05pm, $0.15

- PTC (PTC) 5:02pm, $0.44

- Raymond James Financial (RJF) 4:16pm, $0.73

- SanDisk (SNDK) 4:05pm, $1.57

- Stryker (SYK) 4pm, $1.22 - Preview

- Susquehanna Bancshares (SUSQ) 4:30pm, $0.21

- Teradyne (TER) 5:01pm, $0.04

- Umpqua Holdings (UMPQ) 4:05pm, $0.24

- United Rentals (URI) 4:15pm, $1.48

- Varian Medical Systems (VAR) 4:02pm, $0.91

- Western Digital (WDC) 4:15pm, $2.08

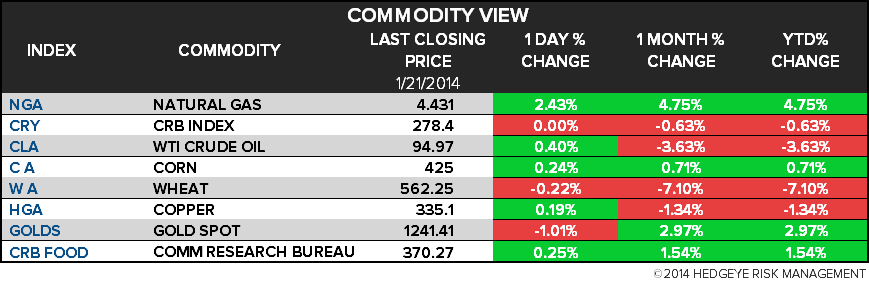

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Uranium Poised for Bull Market as Japan Reviews Reactors: Energy

- Nickel Seen Stalling by Morgan Stanley as Goldman Eyes Rally

- Whistle-Blower in Coal Rally Heralds Colombia Shift: Commodities

- WTI Crude Rises a Third Day on Forecast Distillate Supplies Fell

- Copper Declines on Speculation Chinese Holidays to Curb Demand

- Wheat Gains on Speculation Cold Temperatures May Hurt U.S. Crop

- Rubber Futures Drop to Five-Month Low on China Demand Concerns

- Abenomics Accelerates Gold Sales in Japan as Inflation Hedge

- Rebar Rebounds From 16-Week Low Amid Improved China Money Supply

- India Seen Failing to Meet Sugar Export Plans: Chart of the Day

- Australian Cattle Prices Extend Decline to Lowest Since 2009

- Coal India Faces $4 Billion Rent Claim for State’s Mine Land

- Gazprom, Statoil Gas May Replace Shell-Exxon Supplies in Europe

- Gold Target Cut by Morgan Stanley Seeing ‘More Pain to Come’

CURRENCIES

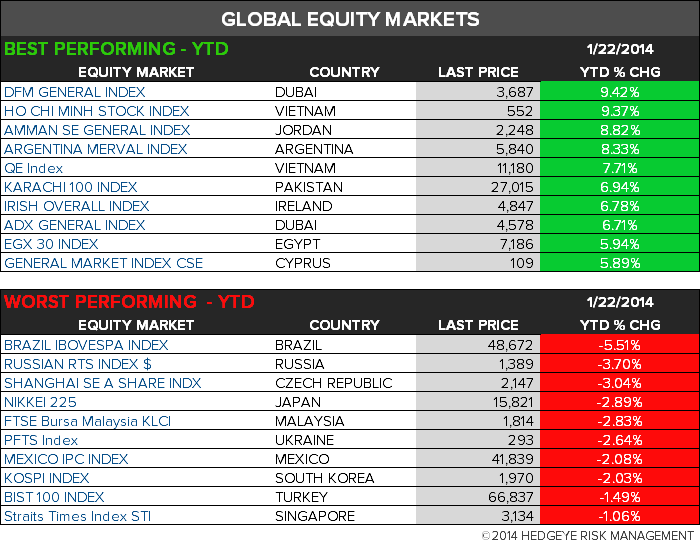

GLOBAL PERFORMANCE

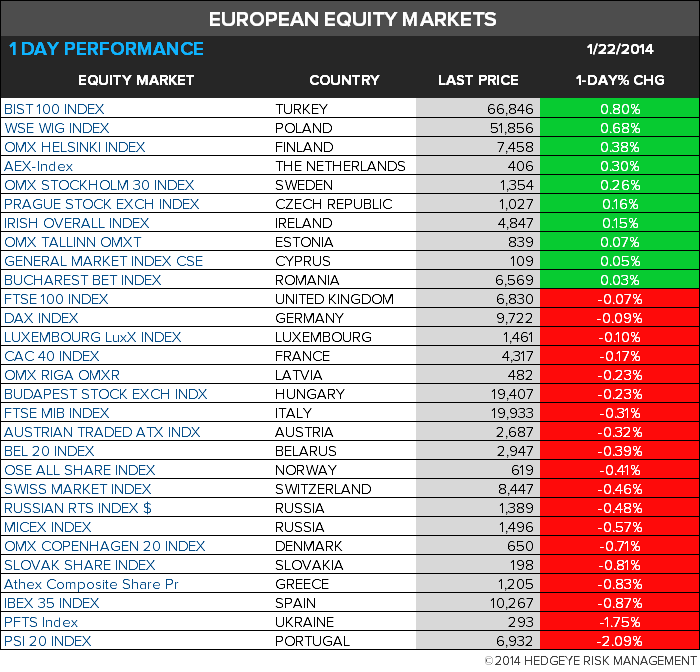

EUROPEAN MARKETS

ASIAN MARKETS

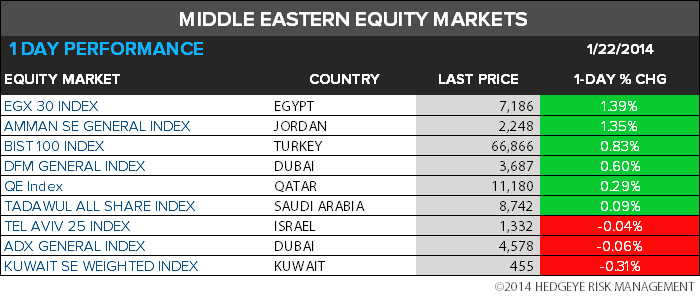

MIDDLE EAST

The Hedgeye Macro Team