Below are Hedgeye analysts' latest updates on our high-conviction stock ideas and CEO Keith McCullough's refreshed levels for each stock.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

The latest comments from our Sector Heads on their high-conviction stock ideas.

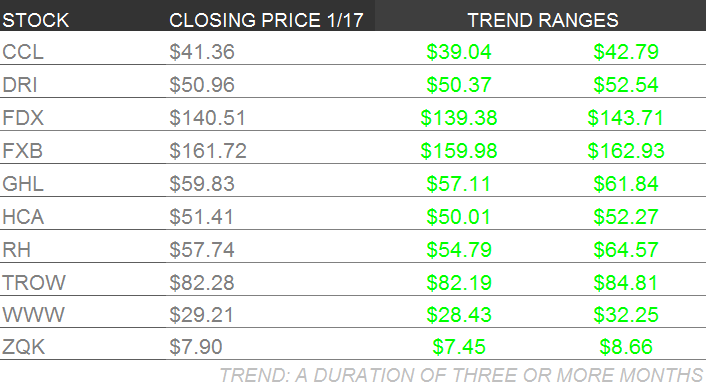

CCL – Hedgeye Gaming, Lodging & Leisure analyst Todd Jordan reiterates his bullish thesis on Carnival. Next week, his team will have visibility into "Wave Season" and will update their take accordingly. CCL is up 15% since being added to Investing Ideas, while the S&P 500 has gained 2.5%.

DRI – Hedgeye Managing Director Howard Penney has been calling Darden’s "strategic plan" woefully inadequate since Day One. Needless to say, people have clearly been listening to the veteran Restaurants analyst. Earlier this week, Barington Capital publicly came out and called for a broader breakup of DRI, which would include spinning off the Olive Garden brand. The activist group plans to host an online presentation on January 30, 2014 to provide more color around their plan to enhance shareholder value.

If these activists are successful in forcing change, Penney sees significant upside to the stock. Mind you, the near-term fundamentals of the business are ugly and current trends in the casual dining sector don’t do much to allay these concerns. We are bullish on DRI, but acknowledge it may not be the smoothest ride. Darden is a name you want to hold over the long-term.

FDX – Shares of FedEx weakened a bit on UPS’s pre-announcement of disappointing earnings. Much of the UPS miss appears related to the challenges of excessive, close-in volume in the holiday season. While there may be some read through to FDX’s costs, we do not expect the holiday challenges to have an ongoing impact on either company. If anything, excess demand from e-commerce could be seen as a long-run positive. We will need to see UPS’s report to confirm the full nature of the preannouncement, but we do not expect it to impact our bullish thesis on FDX.

FXB – We remain bullish on the British Pound versus the US Dollar, a position supported over the intermediate term TREND by prudent management of interest rate policy from Mark Carney at the BOE (oriented towards hiking rather than cutting as conditions improve) and the Bank maintaining its existing asset purchase program (QE).

UK high frequency data continues to offer evidence of emergent strength in the economy, and in many cases the data is outperforming that of its western European peers, which should provide further strength to the currency. Notably this week the UK reported strong retail sales, up 5.3% in DEC Y/Y vs expectations of 2.5% and 1.8% in NOV. CPI also moderated 10bps to 2.0% in DEC Y/Y versus the previous month – we expect this cut in the consumption tax to continue to boost business and consumer confidence and with it consumption.

The British Pound is holding its Bullish Formation, which we expect will continue to be supported by prudent monetary policy from the BOE and strengthening economic fundamentals.

GHL – Bulge bracket bank earnings season shed some light on where the growth was to finish 2013. The earnings releases of JP Morgan, Goldman Sachs, and Bank of America were all consistent in that mergers and acquisitions or M&A had excellent finishes to the end of year which bodes well for the boutique M&A firms (they specialize in M&A versus these larger banking operations where M&A is only 5-10% of total revenues).

The largest banking operation in the sector, JP Morgan, had a 35% increase quarter-to-quarter from 3Q13 in M&A with Goldman Sachs putting up 38% higher revenues q-o-q and even Bank of America (more of a trading and underwriting specialist) which had M&A revenues up 42% from last quarter.

The across the board validation of much improved M&A results in the fourth quarter is a good indication for Greenhill (GHL)’s result on Thursday, January 23rd. While GHL’s quarterly earnings result will likely be less important than management’s assessment of the state of the industry, with the past 3 years having been flat to down in global M&A volumes, any sort of positive indication that things are improving should be well received by investors (GHL is still an unpopular stock with only 1 buy recommendation out of 11 and hence having low expectations).

We estimate that 2014 will be the first positive year of M&A volume improvement since 2010.

HCA – The concern over admission growth in the hospital sector has been growing all quarter. Citi's team wrote a headline-grabbing note saying Q413 was the "worst ever" for hospitals. But it's important to separate the headline (which is frightening) from the fundamentals which continue to look good to us and that we published.

Over the last week, we saw a lot of evidence that we will continue to be right.

First, HCA Holdings pre-announced that Q413 came in better-than-expected. In addition, Tenet Healthcare Corp (THC) which is HCA's closest peer, said something very similar.

Meanwhile, the companies that supply the hips and knees and other devices that drive profits at hospitals? We saw a host of companies announce or indicate their sales trends are improving, while our macro work continues to tell us the trend will continue.

RH – We remain extremely bullish on Restoration Hardware. Our fundamental thesis remains unchanged, and we think it’s important to remember that 2014 will be the first year of square footage growth after a number of years of store closings. Store openings/expansions in Greenwich, CT, Los Angeles, New York, and Atlanta starts phase-1 of the real estate transformation. Couple that with increased sales productivity, robust dot-com growth, new category extensions, and GM improvement – you get, in our opinion, the best 5-year growth story in all of retail.

So... what’s the reason for the pullback?

In the absence of news on RH, we have to defer to conjecture and experience to help explain investors’ behavior. At and prior to the ICR conference in Orlando, FL you had a whole slew of retailers (everyone from Pier1 to Gap) miss holiday sales numbers. The key reasons for the lackluster holiday season: mall traffic, a highly promotional environment, and weather. In light of the current state of retail, investors have drawn the conclusion that RH will be the next to preannounce disappointing holiday earnings. Let’s be clear about one thing – we think it’s highly unlikely that RH preannounces. As it relates to the Holiday season, RH, unlike many other retailers is not tied to the Holiday shopping period.

Over the past 12 months of reported data 55% of sales have been furniture, and of the remaining 45% a negligent amount of that is related to holiday specific inventory (which we might add was completely gone from the one store we visited on Christmas Eve). Do people buy sofas as presents…they might…but we don’t see that as a gift giving category sensitive to the ‘highly promotional’ holiday sales environment. Weather may have a minimal impact when it comes to the 10% of items that are actually sold and taken home from a retail store, but will it stop you from buying a couch? Our answer to that is no as well, the furniture buying is event driven (i.e. home remodel, move, etc) and is stretched over 5-8 store visits. Lastly, RH sales are essentially booked for this quarter (Nov. – Jan.), remember that 90% of orders are fulfilled from the company’s distribution centers. Order fulfillment at this time takes 6 – 9 weeks currently depending on demand, and is not booked as revenue until it arrives at the customers homes. If we do see a weather induced pullback, it’d most likely be felt in Q1 not Q4. It’s hard to even entertain the weather argument with RH, since nearly 50% of its sales come from the .com channel.

We understand that it’s often difficult to remain positive during pullbacks – but the logic in the bear case is less than convincing. Under a worst case scenario, could we see a 5% hit to RH’s top line? Perhaps – given the horrific results we’re seeing at other retailers. But that means that sales grow 30% instead of 35%. The consensus whisper is for a comp of 10%, which we find to be ridiculous.

RH remains our top long idea in retail by a country mile. Nothing that is happening in the current climate could affect our $11 earnings power thesis.

TROW – Shares of T Rowe Price continue to remain attractive as the firm should benefit from a strong finish to 2013 from an equity flow standpoint. Industry equity mutual fund flow totaled a $46 billion inflow in the 4th quarter of 2013 compared to $55 billion which was redeemed within bond funds. T Rowe Price, as largely an equity only manager with the best equity mutual fund performance in the industry, should have benefited from this dynamic in the last quarter of last year. In a recent conversation with TROW management, the firm also referenced that its Asian sovereign wealth clients which have been in redemption the past two quarters, have been less active in the 4th quarter which could remove one major negative catalyst within the story.

WWW – Prior to their presentation at the ICR conference on Tuesday, Wolverine Worldwide reaffirmed the top end of its EPS guidance and took down its revenue estimates by $20 mm. While some took this as an excuse to get even more beared up on WWW, we did not. The holiday selling period was abysmal for many reasons and for practically every brand/retailer on the planet, so for WWW to come through that environment virtually unscathed was a testament to the company’s strong portfolio and diversity (both brand and geographic).

The bearish view was centered on the company’s lighter than expected FY14 revenue guidance and the reported weakness in the Sperry brand. As it relates to revenue it’s important to remember that WWW is the master of tempering the street’s expectations. On its Q4 2012 Conference Call the company guidance called for FY13 Adjusted EPS to be in the range of $1.25 to $1.33. Guidance has risen 7% to where it currently sits today. So we take the company’s conservative targets with a grain of salt - especially when you consider that 2013 was an investing year. This will be the first year where the PLG brands will be able to leverage the global distribution capabilities of its parent company moving from their current 5% of sales outside the US towards the 40% company average. It won’t happen in one year, but that type of opportunity gives us comfort in our double digit sales growth target for FY14. Sperry, on the other hand is not a concern to us in the slightest. The weakness is Sperry was related to inventory of key winter boot styles, not the impending slow down of the boat shoe category in the US that we’ve been assured was looming for four straight quarters. Even if that trend were to decelerate, we’d happily trade 5% growth in the US for 30% growth in International.

The punchline is that we think management’s ‘msd top line and dd bottom line guidance will ultimately result in 10% sales and 20%+ EPS growth. Our estimates remain well above consensus.

ZQK – Quiksilver announced this week that it sold the Tony Hawk brand to Cherokee Inc for $19 million. Tony Hawk was classified as a non-core brand and was sold exclusively at Kohl’s (definitely not on par with the likes of the namesake Quiksilver line, Roxy, and DC footwear). The cash will help the company clean up their balance sheet and fuel investments in core brands.

There are still three assets left to go (Surfdome Shop, Moskova brand, and Maui and Sons) to get ZQK from its prior 11 brand portfolio to its core 3. We view 2014 as a year of cost-cutting and reorganization, which does not really get us too excited. But that still gets ZQK from a loss of $1.53 last year to a modest profit in 2014. But 2015 and beyond is a much different story.

Our long-term model has ZQK adding $600mm in revenue as the company’s new, 12 month old, management focuses its attention on growing the Quiksilver, Roxy, and DC brand free of the distraction of low grossing non-core brands. In the end, this is a 40%+ EPS grower that’s a double if we use a 20x p/e, which we think is more than fair based on the soon-to-be-realized growth profile.

* * * * * * *

Macro Theme of the Week: #GrowthDivergences

In our first Investing Ideas of 2014, we introduced Hedgdeye’s 1Q14 Macro Themes, three key global macro forces that we believe will play a dominant role in shaping the markets in the near term.

The themes are:

- #InflationAccelerating

- #GrowthDivergences

- #FlowShow

This week, we elaborate on the second theme, #GrowthDivergences, as Darius Dale, Hedgeye’s resident expert on all things Asia, focuses “All Eyes on Japan” in this HedgeyeTV video.

#BTDB?

Hedgeye CEO Keith McCullough has been chanting a mantra of “Buy The Darned Bubble!” since December. While the current rise in US equity prices may not be sustainable as what economists call a “secular” trend, meaning a long-term trend that is not seasonal or cyclical in nature, McCullough says there is still money to be made before prices pause or meaningfully correct.

#GrowthDivergences

In the Q1 call, Hedgeye’s Macro team tracked the world’s major markets and identified significant divergences in growth rates among national markets, and in the stages of our proprietary Growth / Inflation / Policy four-quadrant model. For Japan, the headline was “Recovery Losing Steam?” with indications that the economy is heading towards Quad #3: “Growth Slowing and Inflation Accelerating.” This is a dicey setup, as both monetary and fiscal policy find themselves in a box. On the monetary policy side, in a growth-slowing environment it will take more and more quantitative easing, to achieve less and less impact in the financial markets. This concern was voiced in the recently released minutes of the latest meeting of the US Federal Reserve board, and seems to have contributed to the decision to finally announce a taper.

But tightening fiscal policy in a weak growth environment will exacerbate the forces acting as a brake on the economy. Thus, the central bank is damned if they do (QE – which will continue to damage their currency, but to diminishing effect on the markets) and damned if they don’t (slowing economic growth risks turning back the equation, hurting both the currency and the financial markets). What’s a central banker to do? Dale’s work focuses on Japan’s currency. If you want to get Japanese markets right, you’ve got to get the Yen right – a correlation that has proven out very consistently over longer periods.

Bubble Downgraded From “Buy” To “Hold”???

Dale’s models flashed high conviction on the long side in Japan a little over a year ago. Dale says Japanese equities still make sense for now, but his conviction going into the first half of 2014 is not so strong as in the first blush of Abenomics-driven market euphoria.

With Abenomics policies continuing to trash Japan’s currency, Dale’s call remains bearish on the Yen. This should be correspondingly bullish for Japanese equities over the intermediate-term TREND and long-term TAIL durations. Dale believes Japanese economic growth could slow through the first half of this year. Therein lies one uncertainty, because deflationary concerns could ripple through to corrections in Japanese equities.

Governments purposely weaken their own currencies – if you live in the Bernanke-ed States of America, you certainly get that – on the theory that, as the value of the currency goes down, the price of stuff goes up. This has certainly worked for US equities. So far, it has worked well for Japanese equities too, which is why Dale thinks a deflationary trend could be seen as negative in the Land of the Rising Equity Markets.

Dale suggests that intermediate and long-term investors in the Japanese markets might look to hedge against the possibility of an intermediate-term TREND correction. And for the first time in a long time, near-term pullbacks in the Nikkei may not be points to add to long-term positions. This is the first time in the life of the “Abenomics trade” that we’ve said wait and see on pullbacks. Dale says the markets need to hold at key long-term support levels for the bubble in Japanese equities to keep expanding.

The Land Of Falling Expectations?

For much of 2010-2012, US equities responded positively to negative economic news, as investors preferred hearing the shoes, rather than waiting for them to drop. Dale thinks this could replicate in Japanese markets. “There is a rising possibility that Japanese equities start to actually cheer on bad economic data,” he says. While the consensus is that Japanese economic growth will slow in the second quarter, Dale’s work indicates the slowdown may already be upon us in 1Q14. “Considering that Japanese economic growth data has been white-hot,” says Dale, “it’s not exactly going out on a limb to call for it to cool.” #InflationAccelerating in a low-growth environment could further dampen Japan’s consumer-aided recovery. And economic data comparisons year-over-year will naturally get tougher on the back of 2013’s strong showing, making the economic situation appear still more daunting.

Finally, Dale believes Japan’s corporations have not fully bought into Abenomics as a sustainable long-term driver of the economy. This was exactly the same set of concerns that held back growth in the US, as companies and banks alike hesitated to undertake new projects in an atmosphere of regulatory and policy uncertainty, and resulting unclear messages from the financial markets. If the major companies at the core of Japan’s economy are hesitant, then a growth slowdown could become a self-fulfilling prophecy.

A Closely-Watched Bubble

Dale says the next 6-9 months could be the first real test for the economy since Japanese central bank governor Haruhiko Kuroda materially changed the Bank of Japan’s monetary policy.

For now, Japanese markets express faith that the BoJ will continue its program of “Quantitative and Qualitative Easing,” with 80% of economists surveyed by Bloomberg expecting additional stimulus. But if the impact of that stimulus dwindles – or if the bank switches course – near-term weakness in the Nikkei could turn into a rout for investors. Dale says the Bank of Japan’s recent public statements “suggest the BoJ stands ready and willing to react to any confirmation of lost momentum on either the growth or inflation fronts in the interim.”

For investors in the Japanese markets, the big question is: how long is “the interim”? Here at Hedgeye we’re keeping our eye on the Bubble.

- By Moshe Silver

Moshe is a Hedgeye Managing Director and author of the Hedgeye e-book Fixing A Broken Wall Street