TODAY’S S&P 500 SET-UP – January 10, 2014

As we look at today's setup for the S&P 500, the range is 25 points or 0.71% downside to 1825 and 0.65% upside to 1850.

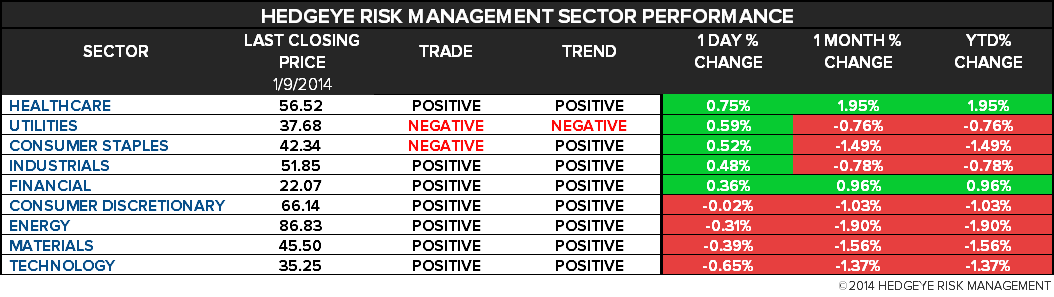

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.54 from 2.54

- VIX closed at 12.89 1 day percent change of 0.16%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Nonfarm Payrolls, Dec., est. 196k (prior 203k)

- 8:30am: Unemployment Rate, Dec., est. 7% (prior 7%)

- 8:45am: Fed’s Lacker speaks in Raleigh, N.C.

- 10am: Wholesale Inventories m/m, Nov., est. 0.4% (pr 1.4%)

- 10am: IBD/TIPP Economic Optimism, Jan., est. 46 (pr 43.1)

- 11am: Fed to purchase $2.5b-$3.5b in 2019-2020 sector

- 1pm: Fed’s Bullard speaks in Indianapolis

- 1pm: Baker Hughes rig count

GOVERNMENT:

- 9:30am: Joint Economic Cmte holds hearing on Dec. employment, w/ testimony from BLS Commissioner Erica Groshen

- 9:30am: House Nat. Resources Cmte panel hearing on seismic exploration of Atlantic outer continental shelf

- 10am CFTC holds closed meeting on enforcement matters

- 12:30pm: Amtrak President Joseph Boardman delivers address on passenger rail issues; National Press Club

WHAT TO WATCH:

- Dec. job gain in U.S. probably capped best year since 2005

- Debt rule faces dilution as regulators heed bank warnings

- ICE said to hire Evercore to sell NYSE technology divisions

- Google X staff meet w/FDA pointing to possible medical device

- Apple cuts China iPhone online, store price for holiday sale

- Goldman Sachs denies Singapore stock dump, countersues Quah

- LightSquared awaits regulatory approval; funding deadline near

- YRC may drop after Teamsters reject accord tied to refinancing

- Aegerion gets U.S. subpoena on rare-disease drug marketing

- Chevron says 4Q net income fell as energy production declined

- Bazaarvoice PowerReviews deal can be blocked by U.S.: judge

- PCs mark steepest drop in 2013 with 10% decline in shipments

- U.K. industrial output unexpectedly stagnated in Nov.

- China’s imports rise to help nation claim trade crown

- NTT Docomo adds most Japan users for first time since 2011

- U.S. Funding Deadline, Retail Sales, GE: Wk Ahead Jan. 11-17

EARNINGS:

- No earnings expected from S&P 500

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- China’s Ore to Coal Imports Reach Records in ’13 as Demand Gains

- Amazon Soy Route Seen Extending Brazil Lead on U.S.: Commodities

- Nickel Surges After Report Indonesia Detained Chinese Vessels

- WTI Crude Rises From Eight-Month Low on Signs Losses Excessive

- Gold Moving-Average Oscillator Returns Most Through 2013 Plunge

- Gold, Silver Imports by India Tumble as Government Keeps Curbs

- Wheat Futures Head for Longest Weekly Losing Streak in Two Years

- Chalco Says Has Enough Bauxite Stored Ahead of Indonesia Ban

- Rubber Posts Biggest Weekly Drop Since April on China Demand

- Red Kite Says Copper Outlook Turns Positive With Glut Delayed

- LNG Export Surge Boosting Prices for Australian Buyers: Energy

- Sugar Traders Turn Most Bearish in Four Months on Indian Exports

- OPEC Outages Propping Up Oil Price Mask Weak Demand: Bear Case

- American Water Expands Military Business With $288 Million Deal

- Gold Rises Before Jobs Data as Investors Weigh Demand, Tapering

CURRENCIES

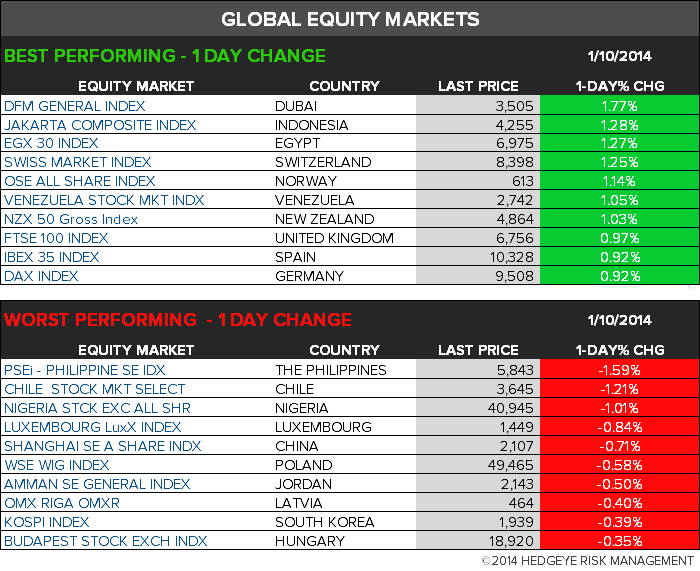

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team