This note was originally published at 8am on December 27, 2013 for Hedgeye subscribers.

“Difficulties are just things to overcome, after all.”

-Ernest Shackleton

Even though many of us thoroughly enjoy our jobs, most work years are still typically a bit of an endurance test. Luckily, as I wrote yesterday, the U.S. stock markets had a very healthy year and returns were up and to the proverbial right. So, for stock market operators, 2013 wasn’t all that much of an endurance test.

I recently finished reading a book called, “Endurance: Shackleton’s Incredible Voyage”, which tells the story of Ernest Shackleton and his failed attempt at being the first person to cross Antarctica from sea-to-sea via the pole. Shackleton’s ship was named the Endurance and endure is exactly what he and his shipmates did.

The Endurance departed from South Georgia for the Weddell Sea on December 5th, 1914. Two months later the Endurance was frozen in an ice flow and Shackleton ordered the abandonment of the ship and her conversion into an ice station. For the next 8 months, the crew lived on the ice floe in the middle of the Antarctic Sea until the ship was finally broken in half by ice pressure.

At that point, Shackleton order his crew to another ice floe and for the next six month, until March 1916, he and his crew shifted between various floes. By April, their current flow was becoming too small and Shackleton and his crew jumped into the remaining life boats to make a five day harrowing trip to Elephant Island.

After a couple weeks on the deserted Elephant Island, Shackleton selected a crew of six to sail with him across the Drake Passage back to South Georgia Island, the nearest point of civilization more than 600 miles away.

The Drake passage is widely considered the most challenging water to sail on the planet. According to Wikipedia:

“There is no significant land anywhere around the world at the latitudes of the Drake Passage, which is important to the unimpeded flow of the Antarctic Circumpolar Current which carries a huge volume of water (about 600 times the flow of the Amazon River) through the Passage and around Antarctica.”

Shackleton and his crew sailed the Drake Passage in a 20-foot wooden sail boat in the middle of a hurricane and eventually made it to a whaling station on South Georgia Island (only after crossing the Island on foot, something no man or men had done to that point). So, after almost 20 months of being stranded in the Antarctic, Shackleton and his crew made it to civilization. And that, my friends, is endurance!

Back to the Global Macro Grind...

After a relative tame investing year in 2013, the question for all of us is: what will we have to endure in 2014 to generate outperformance? There are a few things that potentially come to mind, specifically:

1) Debt Ceiling – The debt ceiling is set to expire on February 7th, though the Treasury Department has the ability to extend this via the use of extraordinary measures for about another month. Treasury Secretary Jack Lew, and thus the Obama administration, has already sent the opening volley in a letter to Congress last week. As Lew wrote in the letter:

“The creditworthiness of the United States is an essential underpinning of our strength as a nation; it is not a bargaining chip to be used for partisan political ends.”

In part he is of course correct, the debt ceiling shouldn’t be used as a bargaining chip, but in reality 2014 is an election year and it is a very good bargaining chip for the Republicans. In particular the Tea Party, who need a win to go back to their constituents with after the recent budget compromise.

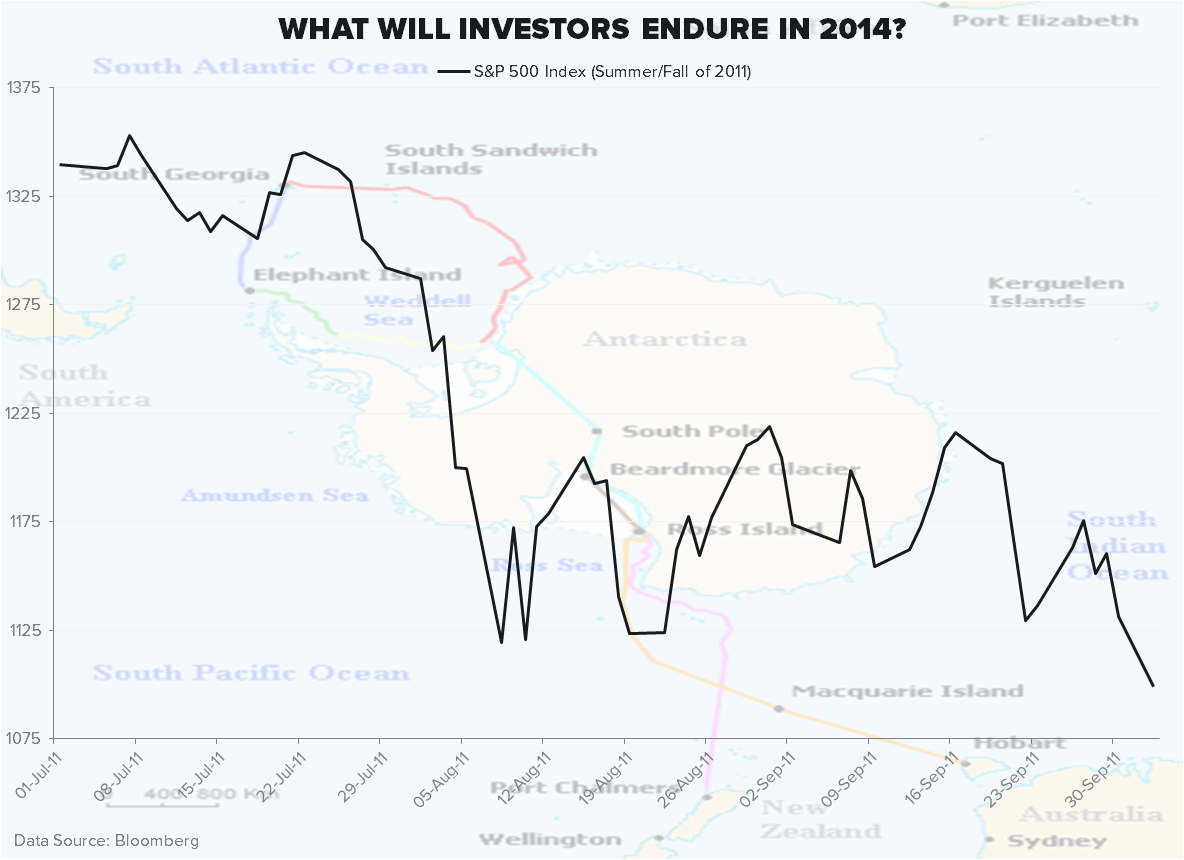

In the Chart of the Day, we show the return of the SP500 in the summer and early fall of 2011. As you may recall, while it wasn’t as difficult as sailing the Drake Passage in a wooden row boat, the last major debt ceiling debate was a difficult and volatile period for U.S. equities.

2) Interest rates – As we’ve noted, the U.S. interest rate market has basically already front run the beginning of tapering. The 10-year yield has close to doubled from the lows of May of this year to the recent high of around 3.0%. Certainly increasing rates has its positive implications, especially as it relates to supporting U.S. dollar strength, the challenge of course is controlling the speed at which rates normalize. An accelerated increase in interest rates will undoubtedly serve to stymy economic growth.

In the short run, the most significant impact that rising rates will have is on the housing market. In part, the impact on the mortgage market is already being seen. According to the Mortgage Bankers Association, mortgage applications fell 6.3% on a seasonally adjusted basis last week to their lowest level in 13-years. National home prices are unlikely to continue climbing if mortgage demand and affordability are falling.

3) Chinese growth – The Shanghai Composite is having a positive morning up more than 1.4% as Chinese Interbank rates fell for the fourth day in a row. While the spike in Chinese interbank rates has garnered headlines over the last few weeks, our Asia Analyst Darius Dale has been quick to note that much of this recent spike relates to a liquidity crunch going into year-end and is likely to be short lived. The broader question for Chine relates to economic growth.

Certainly, managing growth lower will be important for Beijing in reigning in domestic credit growth and rebalancing the economy, but what of the implications globally? A Chinese growth rate potentially slowing from 7.5% to 6-7% will definitely have implications on global economic activity. Some may be positive, such as a decline in demand, and thus price, for certain commodities. Conversely, a lower than expected Chinese growth rate may be a shock to barely recovering Western countries and companies that depend on Chinese demand.

In aggregate, the three points above may actually not provide an endurance test for stock market operators in 2014, but merely be “icebergs” that we easily sail around. Only time will tell on that front.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.91-3.02%

SPX 1810-1855

DAX 9234-9563

VIX 11.35-13.94

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research