EVENTS TO WATCH

LULU: Consumers Challenge Our Bearish View - Friday 1/10 1:00pm EST

The results of our LULU survey are in, and we think we'll have some intriguing take-aways on both LULU and anyone that competes in the (primarily) female active market. Please ping us for details on the call.

INDUSTRY OBSERVATION

Takeaway: With all the companies putting up disappointing sales, we wanted to throw out a factor that we think is critical. Yes, weather was terrible as the month closed out (and got worse in January). But one thing we'll keep in mind is our view that this holiday will go down as a watershed year for the shift from bricks and mortar to dot.com. The chart below shows that over the past 10 years there has been a steady increase in e-commerce's share of total spending, but we think that when this quarter's numbers are reported, it will show the greatest increase in the slope in the the history of the internet. Our belief is that shopping is behavorial, and an increase in dot.com will only feed upon itself and continue to gain share in 2014.

COMPANY NEWS

BBBY - BBBY Reports Q313 Results

Takeaway: BBBY's announcement was obviously a negative one. But in light of the horrendous results reported by retail overall, it really wasn't that bad. The reality is that for many retailers, it's the last two weeks that cleaned their clocks. I can count one, maybe two times in my career I've ever mentioned the weather excuse, but this is one where it at least needs to be considered as a factor. Maybe not THE factor, but it certainly mattered.

M - Macy’s, Inc. Outlines Cost Reduction Initiatives to Support Continued Profitable Sales Growth

(http://phx.corporate-ir.net/phoenix.zhtml?c=84477&p=irol-newsArticle&ID=1889181&highlight=)

- "Macy’s, Inc. today announced it will implement focused cost reductions, including organizational changes, as it prepares to sustain profitable sales growth in the years ahead."

- "Changes being announced today are estimated to generate savings of approximately $100 million per year, beginning in 2014. These savings are incorporated in the company’s 2014 earnings guidance (announced today in a separate news release)."

- "In conjunction with the implementation of these cost reductions, as well as of store closings and asset impairment charges, an estimated $120 million to $135 million of charges, of which $50 million to $55 million is expected to be non-cash, will be booked in the fourth quarter of 2013. These charges were not previously included in earnings guidance provided by the company."

- "Approximately 2,500 employees are expected to be laid off and are eligible for severance as a result of these organizational changes…In total, the Macy’s, Inc. workforce is expected to remain at a level of approximately 175,000 associates."

- "The company is announcing today that it will close the following five Macy’s stores in early spring 2014. Final clearance sales will begin on Monday, Jan. 13 and run for between 10 and 11 weeks (except for Fashion Place Mall, which will close on Sunday, Jan. 12 with no final clearance sale."

- "Eight new and replacement Macy’s and Bloomingdale’s stores are currently planned and/or under construction, as previously announced."

Takeaway: We're the first to give Macy's props for smoking the competition on the comp line, but we need to read in to the impetus for its cost-cutting plans as well. Usually businesses don't go into austerity-mode when business is beating plan.

AMZN - Amazon Enjoys Record-Setting Year for Marketplace Sellers

(http://phx.corporate-ir.net/phoenix.zhtml?c=97664&p=irol-newsArticle&ID=1889316&highlight=)

- "Amazon today announced a record-setting year for Marketplace Sellers with businesses of all sizes selling on Amazon. In 2013, Marketplace Sellers on Amazon sold more than a billion units worldwide, cumulatively worth tens of billions of dollars. Marketplace Sellers around the world also continued rapid adoption of Fulfillment by Amazon (FBA), a service that Marketplace Sellers can choose to have Amazon ship their products directly to customers and offer Amazon Prime benefits…"

- "Apparel is a fast growing category for Marketplace Sellers on Amazon. The number of FBA units shipped by Amazon doubled in size from 2012 to 2013."

Takeaway: We said it before and we'll say it again…2013 will prove in hindsight to be the watershed year for the shift

COLM - Inspired by Greatness: Columbia Unveils 2014 Olympic Uniforms for U.S., Canadian, and Russian Freestyle Ski Teams

- "Columbia Sportswear Company a global leader in active outdoor apparel, footwear, accessories and equipment, unveiled today the 2014 Olympic uniforms for the U.S., Canadian and Russian Freestyle Ski teams."

- "After a successful sponsorship of the powerhouse Canadian freestyle ski team during the 2010 Olympics in Vancouver, expanding Columbia's support to include the equally formidable U.S. and Russian teams was a natural evolution for the global brand."

- "Columbia's uniforms will be worn by national athletes competing in the following events: United States: Moguls and Aerials; Canada: Moguls, Aerials, Slopestyle and Half Pipe; Russia: Moguls, Aerials, Slopestyle, Half Pipe, and Skicross"

ADS - Adidas Appoints Eric Liedtke to Executive Board

(http://www.sportsonesource.com/news/article_home.asp?Prod=1§ion=1&id=49349)

- "The Supervisory Board of Adidas AG appointed Eric Liedtke to the Executive Board of Adidas AG effective Mar. 6, 2014. Liedtke, currently SVP Adidas Sport Performance, will assume responsibility for Global Brands on an Executive Board level. After 30 successful years at the Adidas Group, Erich Stamminger has decided not to extend his Board contract and to leave the Adidas AG Executive Board on March 5, 2014, for personal reasons."

BKS - Barnes & Noble Promotes Huseby to CEO Amid Digital Shift

(http://www.bloomberg.com/news/2014-01-08/barnes-noble-promotes-huseby-to-ceo-amid-digital-shift.html)

- "Barnes & Noble Inc. promoted Michael Huseby, who has served as its chief financial officer and president, to chief executive officer…"

- "Huseby also has been elected to the board, the New York-based company said today in a statement."

JCP, M, WMT, TGT - Winter's Wrath Bears Down on U.S. Retailers

- "Planalytics calculated $5 billion in lost business for Monday and Tuesday, noting that about 200 million people have been affected by the weather. "

- “'We’ve had, over the last couple of days, 20 to 25 stores that opened late, closed early or were closed all day. Munsey, Ind., is the only store that is still closed,' said a Macy’s spokesman on Tuesday. 'We started closing stores on Sunday. We closed eight in St. Louis markets and 15 stores closed early that day, primarily in Indiana. Only a small number of stores were closed all day and they were in Indiana, Ohio and Mississippi.'”

- “'We have just a few stores in Ohio that are currently closed, mostly due to access issues. Associates and customers can’t make it to the stores due to local or state travel advisories and mandates due to poor road conditions,' said a spokeswoman for Wal-Mart Stores Inc. 'We closed one store last night and two others this morning. At peak, we’ve had 50 stores closed. All but the three in Ohio have since reopened.'”

- "Ten J.C. Penney Co. Inc. locations were closed as a result of winter weather Tuesday, with an additional seven closing early due to weather conditions, a spokesman said Tuesday afternoon. 'We began seeing a surge in cold-weather items during the holiday season, and demand continues in much of the country,' he said."

- "Target Corp. on Sunday closed eight stores early due to the weather. All reopened the next morning."

Holiday Comp Updates

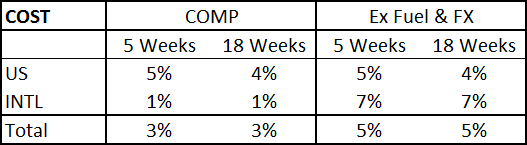

COST - Costco Wholesale Corporation Reports December Sales Results

(http://phx.corporate-ir.net/phoenix.zhtml?c=83830&p=irol-newsArticle&ID=1889295&highlight=)

- "Costco Wholesale Corporation today reported net sales of $11.53 billion for the month of December, the five weeks ended January 5, 2014, an increase of six percent from $10.87 billion during the similar five-week period last year."

- "For the eighteen weeks ended January 5, 2014, the Company reported net sales of $38.33 billion, an increase of six percent from $36.26 billion during the similar period last year."

URBN - Urban Outfitters Reports Record Holiday Sales

(http://investor.urbn.com/phoenix.zhtml?c=115825&p=irol-newsArticle&ID=1889363&highlight=)

- "Total Company net sales for the two months increased to $716 million or 8% over the same period last year. Comparable Retail segment net sales, which include our comparable direct-to-consumer channel, increased 3%. Comparable Retail segment net sales increased 21% at Free People and 11% at Anthropologie and decreased 6% at Urban Outfitters. Wholesale segment net sales increased 21%."

LB - L Brands Reports December 2013 Sales; Updates Fourth Quarter Earnings Guidance

(http://phx.corporate-ir.net/phoenix.zhtml?c=94854&p=irol-newsArticle&ID=1889340&highlight=)

- "L Brands, Inc. reported net sales of $2.098 billion for the five weeks ended Jan. 4, 2014, compared to net sales of $1.947 billion for the five weeks ended Dec. 29, 2012. The company reported a comparable store sales increase of 2 percent for the five weeks ended Jan. 4, 2014, compared to the five weeks ended Jan. 5, 2013."

- "The company now expects fourth quarter earnings per share of approximately $1.60, compared to its previous forecast of$1.67 to $1.82. The decrease versus its previous forecast is primarily the result of lower than forecasted merchandise margins due to incremental promotional activity."

M - Macy’s, Inc. Comparable Sales Including Licensed Departments Rose 4.3% in November/December Period; Comparable Sales Rose 3.6%

(http://phx.corporate-ir.net/phoenix.zhtml?c=84477&p=irol-newsArticle&ID=1889185&highlight=)

- "Macy’s, Inc. today announced that its comparable sales, together with comparable sales from departments licensed to third parties, rose by 4.3 percent in the 2013 holiday shopping season – the months of November and December combined – compared with the same period last year. November/December 2013 comparable sales were up 3.6 percent."

Guidance

- "Macy’s, Inc. is narrowing the range of its guidance for comparable sales growth in the second half of 2013 to a range of 2.8 percent to 2.9 percent (from previous guidance of up between 2.5 percent and 4 percent) – which calculates to guidance for comparable sales in the fourth quarter to grow by approximately 2.3 percent to 2.5 percent, and for full-year 2013 sales to grow by 2.2 percent to 2.3 percent."

- "The company also noted that it will forego an expected $150 million pension contribution in the fourth quarter of 2013 as a result of better-than-expected market returns."

- "Macy’s, Inc. also provided initial guidance for fiscal 2014. Management currently expects comparable sales in 2014 to increase in the range of 2.5 percent to 3 percent compared with 2013 levels. Earnings per share are expected in the range of $4.40 to $4.50."

PIR - Pier 1 Imports, Inc. December Holiday Sales Update

(http://phx.corporate-ir.net/phoenix.zhtml?c=117517&p=irol-newsArticle&ID=1889310&highlight=)

- "Pier 1 Imports, Inc. today reported that comparable store sales for the five-week period ended January 4, 2014 increased 1.3% compared to the five-week period ended January 5, 2013...Before adjusting for the calendar shift, comparable store sales for fiscal December 2014 decreased 5.7%, which compares to a comparable store sales increase of 8.2% for the five-week fiscal period ended December 29, 2012."

ZUMZ - Zumiez Inc. Reports December 2013 Sales Results

(http://ir.zumiez.com/phoenix.zhtml?c=188692&p=irol-newsArticle&ID=1889180&highlight=)

- "Zumiez Inc...today announced that total net sales for the five-week period ended January 4, 2014 increased 4.2% to $125.3 million, compared to $120.3 million for the five-week period ended December 29, 2012. The Company's comparable store sales decreased 2.4% for the five-week period ended January 4, 2014 compared to a comparable store sales decrease of 1.0% for the five-week period ended December 29, 2012."

- "Based primarily on lower than planned sales quarter-to-date, and to a lesser extent lower than planned merchandise margins, the Company is revising guidance and now expects fiscal 2013 fourth quarter sales in the range of $226 to $229 million and net income per diluted share of approximately $0.56 to $0.59, a decrease from the previously issued guidance of sales in the range of $230 to $237 million and net income per diluted share of approximately $0.60 to $0.66."

- "This guidance is now predicated on a low single digit comparable store sales decrease for the fourth quarter and includes a previously disclosed estimate of $1.7 million, or approximately$0.05 per diluted share, for charges associated with the acquisition of Blue Tomato."

BKE - THE BUCKLE, INC. REPORTS DECEMBER 2013 NET SALES

(http://corporate.buckle.com/sites/default/files/press_release/01_09_14_release.pdf)

- "The Buckle, Inc. announced today that comparable store net sales, for stores open at least one year, for the 5-week period ended January 4, 2014 decreased 2.8 percent from comparable store net sales for the 5-week period ended January 5, 2013. Net sales for the 5-week fiscal month ended January 4, 2014 decreased 2.2 percent to $180.9 million from net sales of $185.0 million for the prior year 5-week fiscal month ended December 29, 2012."