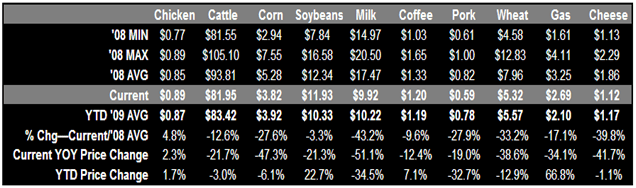

Food costs continue to be extremely favorable for restaurant companies with only chicken prices currently up on a YOY basis.

Sales trends continue to be weak but the 20%-plus YOY declines in most restaurant commodity prices should continue to soften the impact on margins in Q2. Chicken prices are only up about 2% YOY and year-to-date so the only negative standout is the increasing gas prices, which though still extremely favorable on a YOY basis, are now up nearly 70% year-to-date. Gas prices tend to increase the most in the summer driving months so we will have to watch how these increasing prices impact consumers' discretionary spending and eating out habits in the coming months. Current prices at the pump still look good, however, relative to the $4-plus per gallon we experienced last June and July.

Lower dairy prices will continue to help restaurant margins in the near-term with milk and cheese prices down 51% and 42%, respectively. That being said, these favorable prices may reverse rather significantly in 2010 because according to a Bloomberg article, milk prices could rise by at least 25% by the second half of 2010. Dairy farmer profits are currently under pressure because it now costs $17 to produce $10 of milk. In an effort to improve profitability, the article states that the National Milk Producers Federation in Arlington, Virginia, will pay dairies to slaughter 103,000 U.S. cows in the coming months. "The cuts will lead to the first two-year drop in output in four decades and higher prices in 2010 for butter, cheese, milk and the non-fat dry powder that's a benchmark for global exports, according to U.S. Department of Agriculture forecasts....U.S. dairies are trimming the herd. The kill in the week ended June 6 rose to 60,800 head, 35 percent higher than a year earlier, according to USDA data. This year's cull is up 13 percent from 2008."