“During the past five difficult years, we’ve attempted to make the decisions and take the actions that would keep Caterpillar competitive in a global economy, no matter how difficult those decisions might be. Early in the 1980s, we recognized that our industry was faced with substantial overcapacity and that there would be tremendous price pressure on our products.”

-1986 Caterpillar Letter to Shareholders

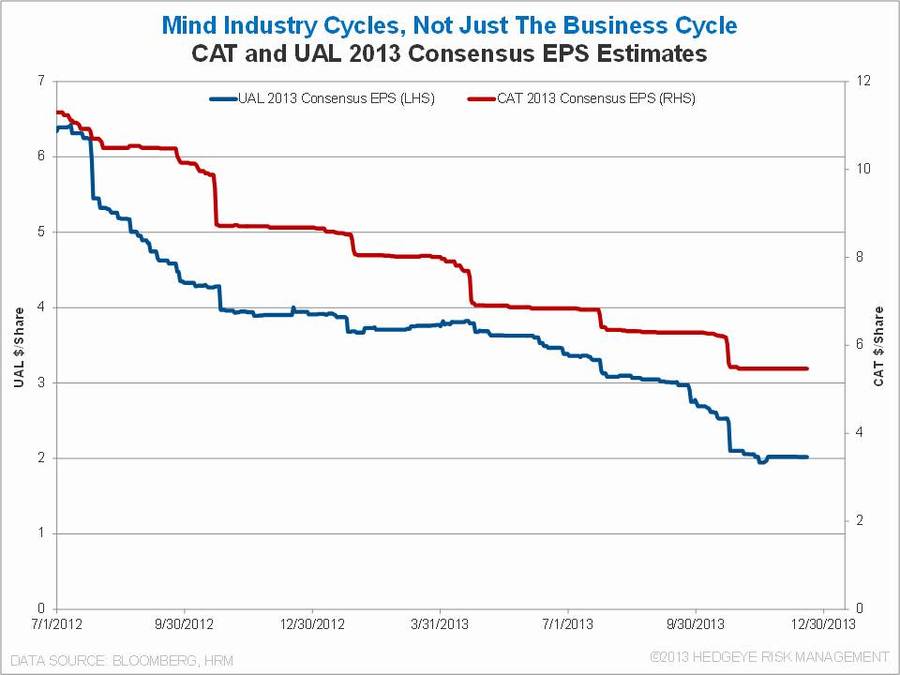

On a list of the Worst CEOs of 2013 yesterday, CAT’s Oberhelman and UAL’s Smisek joined John Chambers and Michael Jeffries on the, let’s say, “laggard” list*. Both UAL and CAT have been Hedgeye Industrials ‘shorts’ since we launched in mid-2012, paired against ‘longs’ PCAR (later TEX) and lower cost airlines, respectively. While we are not surprised to see CAT and UAL on the list, is it fair to blame the CEOs? Was it really management?

As a long-time buysider, I worry about having my views immortalized in print. Intellectual flexibility is central to survival in markets; published opinions serve as an anchor. In October of 2012, we penned our previous Early Look "Steady-As-She-Goes?" outlining the short case for CAT. Luckily, there is little to change 14 months later. A differentiator in our Industrials work is a keen focus on industry specific cycles. I often hear cyclicals discussed in the context of the business cycle – particularly in reference to early/mid/late cycle. We take a different and, we think, more robust approach.

Back to the Global Macro Grind...

Most capital equipment cycles are simply driven by the fact that “stuff” gets old. Typically, regulation, tax changes or the like drive a period of abnormal demand, such as a pre-buy ahead of costly new emissions regulations. Clumps of capital equipment purchased at the same time tend to wear out at the same time, creating ups and downs in demand, capacity utilization and margins independent of trend growth. Central planners tend not to consider these long-tailed distortions when slamming policies into place, but our P&L is grateful for their neglect.

The cycles in airlines and mining equipment are a bit different, however.

In airlines, the cycle has historically been driven by a dance we call the ‘bankruptcy shuffle’. When the least competitive airline lowers costs in bankruptcy, it pushes the next airline down the cost curve into the top cost spot. As we see it, AMR’s bankruptcy last year thrust UAL into that uncomfortable seat, conceptually in the back near the bathroom. Given heavily unionized labor and little control over other costs, it has been very difficult for airlines to address uncompetitive costs outside of Chapter 11. While the airline industry appears to be benefiting from an accelerated replacement cycle in commercial aircraft driven by significant fuel cost increases, and probably consolidation and other factors, we do not think the industry has improved enough to allow the high cost player to make a reasonable profit. After all, AMR went bankrupt fairly recently. As we see it, this dynamic will continue to plague UAL.

In resources-related capital equipment, rising commodity prices drive growth in commodity capital spending. In mining, for example, higher metals prices allow profitable development of new mining projects. The staggering increase in metals prices in the past decade drove a ‘bubble’ in mining capital investment. Unfortunately, once metals prices stopped increasing, the stream of new projects started to run dry. And dry is normal. Assuming commodities remain flat to down, we suspect that CAT, JOY, Komatsu and friends will enter a period much like the early 1980s described in the quote above.

But what about management?

Hindsight is 20/20 and we usually prefer to give people – yes, management teams are made of people – the benefit of the doubt. But in the case of CAT and UAL, management actions should shake investors. For example, UAL’s 2011 non-GAAP income metrics include $600 million in profit from an accounting change (adoption of ASU 2009-13). Usually, the whole point of a non-GAAP presentation is to remove non-operating items. UAL stopped providing estimates for this benefit in 2012, despite some dicey S.E.C. correspondences on the issue. UAL also laid out a brand new cost cutting plan at its recent analyst day, while having failed to deliver on its current profit improvement plan. And don’t get us started on UAL’s special items. At CAT, management made spectacularly poor acquisition choices in Bucyrus and ERA, paying far too much and buying into a bubble, as we see it. Worse, CAT management seems to be in denial about the severity of the resources-related capital equipment downturn, with industry overcapacity a serious looming problem, by our estimates.

Management teams at cyclical companies often get too much credit or grief for factors well beyond their control. But when management teams make efforts to avoid, deny or hide what is really going on, a challenging period can quickly spiral into a disastrous one. CAT suffered mightily in the early 1980s, but that existential threat forced a clear-eyed appraisal of what was needed to survive and, many years later, thrive. In our view, these two management teams have yet to “make the decisions and take the actions” necessary, possibly out of a desire to avoid potentially humiliating accountability. They are people. Fortunately for shorts, we expect these management teams to focus on investor perception instead of business reality for a while longer.

Our immediate-term Global Macro Risk Ranges are now:

UST10yr 2.86-2.95%

SPX 1

VIX 12.91-14.91

USD 80.15-81.14

Gold 1191-1232

Good Luck Out There Today.

Jay Van Sciver, CFA

Managing Director