TODAY'S CALL OUT

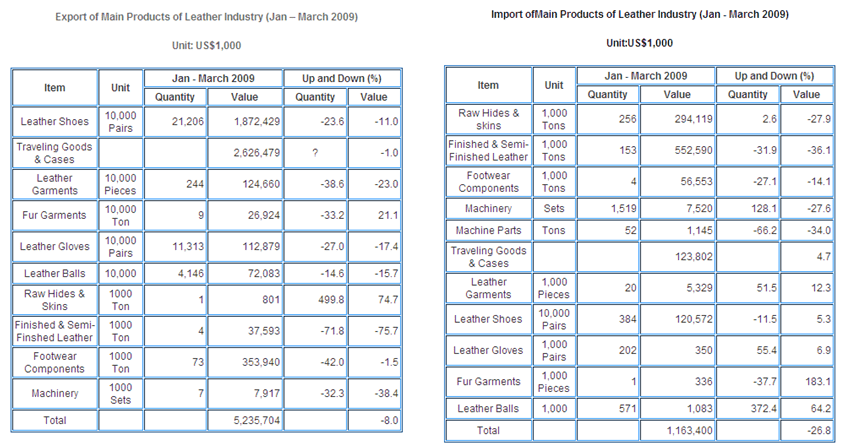

While the Street was predisposed yesterday with the hangover of the Fed announcement, and in digesting results from Nike and Bed, Bath & Beyond, some important datapoints around 1Q Chinese Leather imports/exports went unnoticed. Yeah...I know, I know... We're already looking at the close of 2Q, and China makes up its numbers anyway. So these are stale and fabricated...why should we focus on them? Aside from the case I could make that the US makes up its numbers as well on trade categories (and other areas), this data from China is at least consistently fabricated. In other words, it tends to directionally track economic reality for users of leather. Two callouts...

- The growth spread in leather shoe imports/exports troughed. Exports were down 24% in units, and 11% in dollars. The gap here is second only to 'footwear components' in the major categories, in which exports were down 42% in units and only -1.5% in dollars. At the same time, leather shoe imports were UP 5.3% in dollars. While I'd argue that there will be a secular shift in imports of leather footwear into China by European producers as the Chinese consumer continues to emerge from the Iron Rice Bowl and takes down savings rates and spend on higher-end goods, this quarter's uptick is notable.

- Is it any mistake that this is the exact quarter where exports for China in aggregate were down 23%? Nope. Is it any surprise that just weeks after quarter-end China loosened taxes (VAT) on footwear to stimulate exports? Nope. Similarly, should it come as a surprise that three weeks later China did the same for leather goods? Nope. Since then we've seen around 1,500 factories re-open in the Pearl River Delta in China (off a base of 6k).

Mark my words everyone... These numbers will prove to be a trough. The balance of power from a margin perspective is shifting back to the US brands that have been hurt over the past 2 years. People are underestimating the impact in 2010 for key companies.

LEVINE'S LOW DOWN

Some Notable Call Outs

- We're not ones to perpetuate rumors or to recycle published news stories, but this quote is notable from UK's The Independent. Tadashi Yanai, CEO of Japanese company Fast Retailing (parent of Uniqlo) said that he wants Fast Retailing to become the world's biggest clothing manufacturer and retailer, with annual sales of ¥5 trillion (over £30bn) within the next decade. He also said that, "to achieve our target, the Asian market is the most important and we have already begun to expand there. In Europe and the US it is not realistic to establish hundreds or thousands of new stores solely via our own efforts, so we want to buy a big chain business." He went on to confirm that Gap is "within the scope" of the domestic companies he has his eye on.

- We're still questioning the logic of the DBRN/TWB merger announced yesterday. The conference call did little to articulate the real opportunities the combined entity will ultimately benefit from. We do not count elimination of "public company costs" or the assistance that DBRN will provide in alleviating Tween's limited access to capital as blockbuster reasons to justify the deal. Regardless of the strategic rationale, this deal is the largest we have seen so far in what is likely to remain a robust m&a cycle.

- In a growing trend that may ultimately benefit retailers like CHRS and CTR, other specialty and department store retailers are cutting their exposure to the plus size business. The economy along with the higher cost, slower turning nature of plus sizes has led to the elimination of the category in stores. Most retailers are maintaining online offerings however. Historically, the plus size business has been seen as an untapped growth opportunity but it has not been successfully capitalized on in recent years.

MORNING NEWS

Zach's overview of items you're unlikely to find in the general press.

- Takashimaya Co., Japan's third largest department store chain, announced a steep drop both in sales and profits for the third straight quarter. Net profit dropped a whopping 93 percent to 316 million yen, or $3.2 million at exchange rates for the period. The retailer said Friday it has not seen any sort of recovery for apparel and high-priced luxury goods in recessionary Japan. To that end, sales slid 13.3%, operating profit dropped 72%. Japanese department stores are struggling to spur revenue as falling wages and a worsening job outlook deter consumer spending. Takashimaya began its summer sale this month, 10 days earlier than the usual July start. <http://www.bloomberg.com/apps/news?pid=20601205&sid=awIFL54qzpFg>, <http://www.wwd.com/business-news/takashimaya-q1-net-profit-drops-93-percent-2191705?navSection=retail-news>

- Subhiksha Trading Services Ltd., the Indian retailer that closed stores after it ran out of cash, is confident its debt recast will be completed "well before" the end of next month after negotiations with stakeholders. The debt restructuring of the company, key to the survival of the retail chain, has to be completed by July 31, or six months since the beginning of the process. Subhiksha, which owes 13 banks about 8 billion rupees ($165 million), said 12 of the banks and the company's three largest stockholders are working to restructure the debt and infuse funds needed for the company to reopen its stores, Subramanian said. Subhiksha on Jan. 30 said its business was at a "near standstill" and it needs 3 billion rupees to resume operations. The retailer, founded in 1997, ran out of cash in October after relying on a "high level" of debt, according to the company. <http://www.bloomberg.com/apps/news?pid=20601205&sid=a6T5uKNOZJQY>

- Online e-tailer eLuxury appears to be reincarnating as a social media site devoted to the world of luxury. Today, the e-tailer shuts its doors and on Monday, the new concept makes its debut. Starting Monday, the site will pose one question a day, subjects will include fashion, art, food and wine, design, culture, travel, beauty, music and entertainment, the company said. "ELuxury will learn from its audience, getting smarter each day, and will use this intelligence to present increasingly targeted and relevant content," said a statement. <http://www.wwd.com/business-news/takashimaya-q1-net-profit-drops-93-percent-2191705?navSection=retail-news>

- Textile group Devanlay SA, the manufacturer and distributor of sports brand Lacoste, has appointed José Luis Duran, former chief executive officer of French food retailer Carrefour, president of its management committee. Duran will be named ceo of the company in September and is expected to take the helm of Swiss-based Maus Frères SA, Devanlay's holding company, in 2010, succeeding Guy Latourrette. <http://www.wwd.com/business-news/duran-to-head-devanlay-manufacturer-of-lacoste-2191204?navSection=business-news>

- McKay Belk, president and chief merchandising officer of the Belk Inc. department store chain, is going on sabbatical for ministry-related work. Belk's sabbatical from the department store chain, which was founded by his grandfather William Henry Belk in 1888, begins Aug. 3. Belk said after his 12-month sabbatical he will become vice chairman, and will continue to provide the company advice on merchandising strategy and vendor relations. He will also continue as a member of the Belk board. But Belk also said he may not decide to come back. <http://www.wwd.com/business-news/takashimaya-q1-net-profit-drops-93-percent-2191705?navSection=retail-news>

- John Jansen has been appointed to the new position of GM for Keen Europe. He will run the division from the company's new European headquarters in Rotterdam, the Netherlands. Jansen will focus on building the brand's business in Europe, but also will be part of Keen's global management team. He will work across the company to create a growth strategy for Keen in Europe. Jansen was previously VP of commerce for O'Neill in Europe and also has worked for Nike and Converse. <http://www.wwd.com/footwear-news/brooke-burke-to-appear-in-skechers-ad-2191329?navSection=footwear-news>

- Dakine launched an interactive mobile-specific website, an abbreviated version of Dakine's website that is compatible with most media rich-enabled cell phones. When connected to a high-speed wireless or 3G network users can access streaming music and video clips. Additionally, worldwide surf reports provided by Surfline.com are available along with Snow reports provided by OnTheSnow.com. <http://www.sportsonesource.com/news/article_home.asp?Prod=1§ion=8&id=28495>

- French Consumer Confidence Increases to 15-Month High as Recession Eases - French consumer confidence rose in June for a fourth consecutive month to the highest since March last year in a further sign the recession may be easing. <http://www.bloomberg.com/news/industries/consumer.html>

- U.K. retailer Woolworths was relaunched today as an online business, woolworths.co.uk, by its new owner Shop Direct. The Web site focuses on the same Woolworths' offers as the store chain-toys and outdoor, children's clothing under the Ladybird brand, video games, DVDs, CDs and books and party goods, plus its famous "pick 'n' mix" sweets. Household goods have been dropped from the offer. <http://www.licensemag.com/licensemag/Retail/Woolworths-Back-in-Business-with-Shop-Direct/ArticleStandard/Article/detail/606498?contextCategoryId=33594>

- Recap of PVH's annual meeting - PVH is freezing development of Calvin Klein full-price retail stores as the company continues to downsize its outlet retail operation. Although Calvin Klein is a highly profitable growth engine, PVH's outlet retail business has been a drag on financial performance. Calvin Klein retail stores have been hurt by the recession and won't expand until they begin to meet performance goals. PVH will continue to shut outlet stores, with 150 closures expected over the next three years in addition to the 100 Geoffrey Beene stores already shut. <http://www.wwd.com/business-news/duran-to-head-devanlay-manufacturer-of-lacoste-2191204?navSection=business-news>

- Quiksilver Inc. and its subsidiary Quiksilver Americas Inc., entered into a commitment letter with Bank of America, N.A. ('Bank'), Banc of America Securities LLC, General Electric Capital Corporation ('GECC'), and GE Capital Markets Inc., pursuant to which the Bank and GECC committed, subject to certain conditions, to provide a senior secured asset-based revolving credit facility to Quiksilver Americas and certain of its domestic subsidiaries in the aggregate principal amount of $200 million. On June 24, 2009, the same parties entered into an amendment of the Revolving Credit Commitment Letter to extend the date by which all specified conditions must be satisfied, from June 26, 2009 to July 31, 2009. <www.sec.gov>

- Dickies aims to give its clothing a higher purpose in a new ad campaign. The manufacturer of work, school and outdoor apparel unveiled its new brand campaign today "Wear with Purpose", which focuses on the real stories of several American workers. The campaign was developed in-house at Williamson-Dickie, and begins this month, via print, online and national broadcast, as well as point-of-sale at retailers. Williams-Dickie Manufacturing Company spent $5.3 million on media, per The Nielsen Company. Dickies' new tagline replaces "Legend in Work," but keeps with the brand's focus on the practical use of its clothing. According to Uchtman, this emphasis on hard work has broad appeal to a diverse base of consumers. <http://www.brandweek.com/bw/content_display/news-and-features/retail-restaurants/e3iabcb04149132c4bd59cfefeb2231eee6>

- Brown Shoe Co. Inc., the operator of retail footwear sites Shoes.com and FamousFootwear.com, relies on its own usability lab and outside site performance testing to see how its web pages are viewed by shoppers through multiple web browsers. Although Brown doesn't try to optimize its web sites for any single web browser, it monitors the breakdown of browser use by its site visitors and constantly tests how its pages are viewed through each of these browsers, says vice president of e-commerce Pete Hogan. <http://www.internetretailer.com/dailyNews.asp?id=30923>

- The Timberland Company has launched its latest green product innovation, the Earthkeepers 2.0 boot, which is touted as the first footwear the company has designed to be disassembled and recycled, rather than discarded, at the end of its life. The 2.0 collection is made of 80% recyclable or reusable materials that represent a 15% reduction in greenhouse gas emissions and a 15% increase in the use of recycled or renewable content, compared to the traditional Earthkeepers boot. Timberland said it will be the first footwear company to commercialize this process and plans to incorporate it into its fall 2009 collections. <http://www.environmentalleader.com/2009/06/24/timberland-designs-first-recyclable-footwear/>

- Skechers USA announced Thursday that celebrity host and season-seven winner of "Dancing with the Stars" Brooke Burke will model in the next "Nothing Compares to Family" ad campaign. Burke will appear in the campaign with her fiancé, David Charvet, of "Baywatch" fame, and son Shaya, 1, and daughters Rain, 2, Sierra, 7, and Neriah, 9. The model first appeared in a Skechers ad in 1995. <http://www.wwd.com/footwear-news/brooke-burke-to-appear-in-skechers-ad-2191329?navSection=footwear-news>