“The way I feel about music is that there is no right and wrong. Only true and false.”

-Fiona Apple

I was dead wrong on the no-taper call yesterday, and (after covering my US Dollar short position within minutes of the decision) was somehow positioned right (8 LONGS, 0 SHORTS). Where I was brought up, being right for the wrong reasons is called luck.

True or False: Ben Bernanke did the right thing in tapering yesterday? True. Whether or not his obeying the US 2013 #GrowthAccelerating data on a lag (he’s 3 months late in making a decision he should have made in September) proves to be right is up to history.

I think that if most people were intellectually honest about it, they wouldn’t have told you that A) Bernanke was going to taper yesterday AND B) US stocks would rip to all-time highs on that. But they did. That is the only truth that matters this morning.

Back to the Global Macro Grind…

So what do we do now? Sticking with the process, that’s actually the easiest call to make. We simply go right back to where we were positioned from December 2012-September 2013:

- Long Growth (Equities)

- Short Gold, Bonds (and Equities that look like Bonds, like MLPs)

Why?

- #RatesRising + a USD that isn’t going down in a ball of flames = bad for Gold Bond positions

- #Flows (out of Gold Bonds into US Growth Stocks) should dominate well into the new year

That’s why my 1st three moves in #RealTimeAlerts after the taper decision yesterday were:

- COVER US Dollar Short

- SHORT Pimco’s Total Return Fund (BOND)

- SHORT Kinder Morgan (KMI)

It’s one thing to make mistakes in this game. It’s entirely another to make mistake-upon-mistake after making that first mistake. In hockey terms, give away the puck once – feel shame. Give it away again – feel sitting on cold Canadian bench for rest of game.

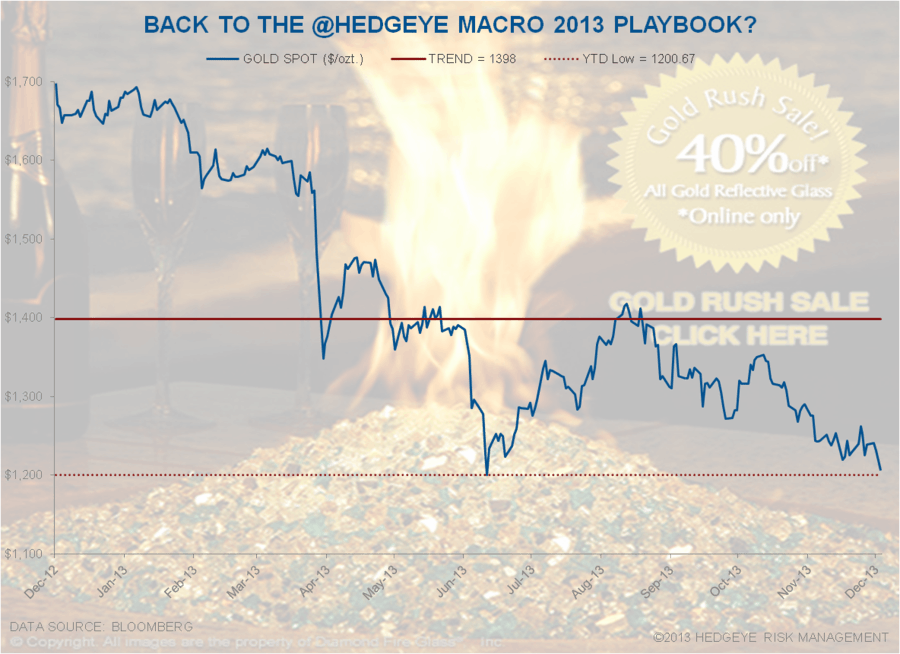

I could have easily given away the puck post taper yesterday buying something like Gold because it was down. It’s down a lot more this morning (Silver -3.9%, Gold -1.1%) and testing its June 27th YTD closing low of $1200/oz.

True or false: Gold hates #RatesRising?

- US Treasury 10yr Yield 2.88% = +17 bps month-over-month and +112 bps YTD

- Gold (started the yr at $1675) = still crashing, -28.3% YTD

Another puck I could have given away would have been trying the long Yen “because everyone is short the Yen.”

True or false: Nikkei loves Burning Yen?

- Japanese Yen (vs USD) = crashing, -17% YTD

- Nikkei = +1.7% overnight to +54.97% YTD

In other words, as soon as you saw the word “taper” yesterday, you got the Dollar right (up) and that helped you get a lot of other things Global Macro right.

True or false: Dollar Up = Emerging Markets Down?

- US Dollar (despite being UP now for 1st wk in 6) = +1.1% YTD

- MSCI Emerging Markets Index = down -5.9% YTD

Oh, and despite the epic US Equity market rip to all-time highs (SP = +26.9% YTD), Emerging Equity markets in Asia were down overnight (India -0.72%, Philippines -0.64%). Turkeys’ stock market is -0.7% this morning too.

On the taper news yesterday, Argentina, Chile, and Peru all saw their stock markets close down on the day. “Emerging” commodity countries = #EmergingOutflows.

So is it the marketing messages of asset management firms that are perma long Gold, Bonds, and Emerging Markets that are right or wrong in a Dollar Up + #RatesRising environment? Or are the perceptions of their investors simply false?

The truth is always in the balance of your account. It’s there, each and every market day, whether you played lucky or not.

Our immediate-term Global Macro Risk Ranges are now:

SPX 1

USD 80.15-81.14

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer