TODAY’S S&P 500 SET-UP – December 17, 2013

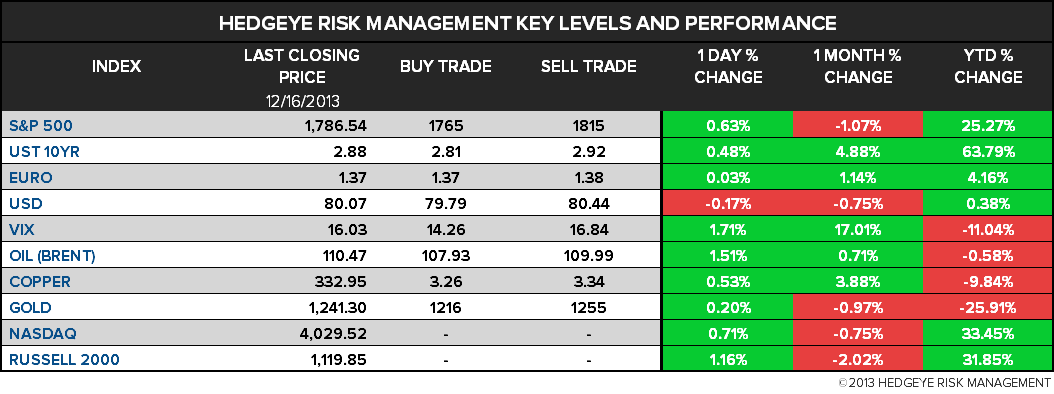

As we look at today's setup for the S&P 500, the range is 50 points or 1.21% downside to 1765 and 1.59% upside to 1815.

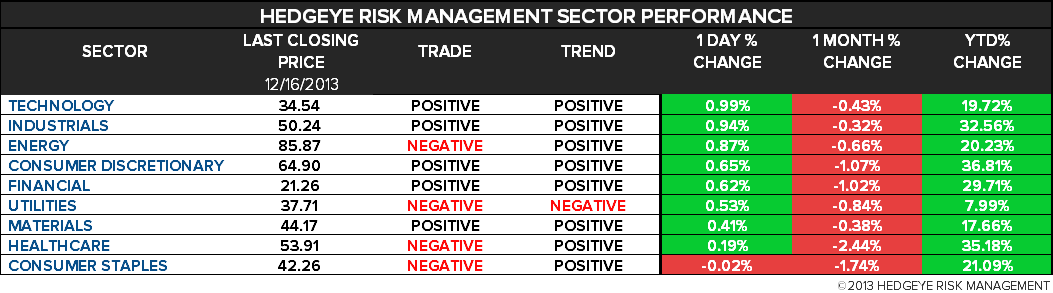

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.54 from 2.55

- VIX closed at 16.03 1 day percent change of 1.71%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Current Acct Balance, 3Q, est. -$100.4b (pr -$98.9b)

- 8:30am: Consumer Price Index m/m, Nov., est. 0.1% (pr -0.1%)

- 10am: NAHB Housing Market Index, Dec., est. 55 (prior 54)

- 4:30pm: API weekly oil inventories

- Two-day FOMC meeting starts

GOVERNMENT:

- Senate in session, House not in session

- Senate to consider bipartisan budget agreement reached Dec. 10

- 8:50am TSA Administrator John Pistole delivers keynote remarks at Air Line Pilots Association

- 9am, FOMC 2-day closed meeting on interest rates starts

- 9:30am Sens. Amy Klobuchar, D-Minn., Christopher Coons, D-Del. hold news conf. on U.S. manufacturing sector

- 10am Sen. Tom Coburn, R-Okla. holds news conf. on “Wastebook” annual report on federal spending

- 10am ADBE, ANLY among witnesses set to testify at Senate Judiciary Cmte hearing on limiting so-called patent trolls

- 10:30am Interior Sec. Sally Jewell and Gov. Martin O’Malley, D-Md., make offshore wind energy announcement

- 10:30am Senate Homeland Security Cmte holds hearing on safety at federal facilities post Washington Navy Yard massacre

WHAT TO WATCH:

- FOMC begins 2-day meeting on interest rates

- Charter said to tap Goldman Sachs for Time Warner Cable bid

- Sherwin, NL, ConAgra must pay $1.1b in lead paint lawsuit

- MetLife said in talks for stakes in AMMB’s insurance units

- Goldman Sachs aluminum antitrust suits sent to New York

- Nasdaq must face some investors’ claims over Facebook IPO

- Facebook to start showing video ads this week, WSJ reports

- U.S. Senate set to consider Dec. 10 budget agreement

- Glaxo to end doctor payments amid marketing practices review

- Herbalife clean audit a setback for Ackman’s pyramid case

- SAC manager Steinberg’s jury to begin deliberations

- Detroit seeks to pay UBS, BofA $230m to cancel swaps

- U.K. inflation nears BOE’s 2% target w/unexpected slowdown

- Europe car sales up 3rd month on new Volkswagen models

- German ZEW investor confidence rises as economy gathers pace

- Japan to add military hardware amid growing China tensions

EARNINGS:

- FactSet Research Systems (FDS) 7am, $1.22

- Heico (HEI) 5:14pm $ 0.40

- Jabil Circuit (JBL) 4:02pm $0.54

- Sanderson Farms (SAFM) 6:30am, $2.19

- VeriFone Systems (PAY) 4:01pm $ 0.26

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Indonesia’s Cabinet to Discuss Ore Ban Amid Freeport Queries

- Chocolate Eaters Drive Record Cocoa-Output Deficit: Commodities

- Gold Declines in London Before Fed Meeting; Palladium Advances

- Brent Falls From One-Week High; U.S. Fuel Supplies Seen Rising

- Ivory Coast 2013-14 Cocoa-Bean Arrivals 43% Higher as of Dec. 15

- Copper Swings Between Gains and Drops Before Fed Policy Meeting

- China Finds More U.S. Corn Shipments With Unauthorized MIR162

- Palm Oil Drops as Record Global Soybean Output May Hurt Demand

- Commodity Investments Seen by Barclays Set for Record Outflow

- Citigroup Divests Metalmark Holding to Comply With Volcker Rule

- Buffett $1 Billion Order Shows Wind Power Rivals Coal

- Ex-Mizuho Derivatives Trader Banned for Lying to U.K. Watchdog

- Hong Kong Exchanges Bulls at Highest Since 2011 on LME: Options

- China Said to Buy 87,200 Tons of Rubber for State Reserves

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

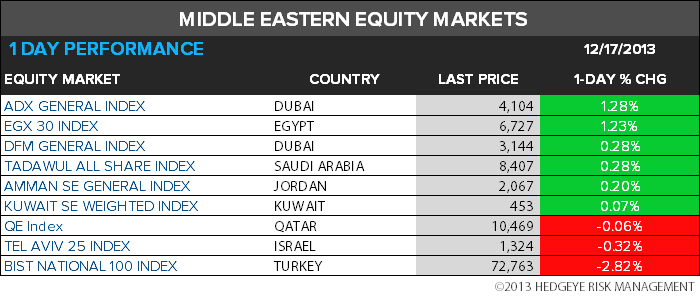

MIDDLE EAST

The Hedgeye Macro Team