TODAY’S S&P 500 SET-UP – December 16, 2013

As we look at today's setup for the S&P 500, the range is 24 points or 0.47% downside to 1767 and 0.88% upside to 1791.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.53 from 2.54

- VIX closed at 15.76 1 day percent change of 1.42

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Empire Manufacturing, Dec., est. 5 (prior -2.21)

- 8:30am: Nonfarm Productivity, 3Q final, est. 2.80% (pr 1.9%)

- 8:58am: Markit U.S. PMI Prelim., Dec., est. 54.8, pr 54.3

- 9am: ECB’s Draghi speaks in Brussels

- 9am: Total Net TIC Flows, Oct. (prior -$106.8b)

- 9:15am: Industrial Production, Nov., est. 0.6% (pr -0.1%)

- 2pm: Bernanke makes commemorative remarks at Fed Centennial

GOVERNMENT:

- Senate in session, House not in session

- U.S., EU negotiators hold 3rd round of negotiations on Transatlantic Trade and Investment Partnership

WHAT TO WATCH:

- AIG said to near sale of plane unit to AerCap for cash, stk

- J&J said to get 3 diagnostics bids of at least $4b each

- Mitsubishi Heavy, GE settle wind patent infringement cases

- China manufacturing index unexpectedly falls as output slows

- Euro-area manufacturing expands more than forecast on Germany

- Budget deal lauded by lawmakers belies fiscal rigors ahead

- Credit-card Nov. charge-offs, delinquencies reports today

- Yahoo CEO apologizes to users for e-mail service problems

- Japan Tankan shows limits on spending as cos. get cautious

- China to probe pricing in antitrust drive, regulator says

- Merkel keeps Schaeuble at Finance; von der Leyen to Defense

- Draghi ally Asmussen to leave ECB board for German govt

- Ukraine demonstrations surge; fractures hurt opposition

- Google buys robotics co. Boston Dynamics, NY Times reports

- Berry Petroleum, Linn Energy holders vote on acquisition

- Charter said to ready offer letter for Time Warner Cable

- Facebook, Wal-Mart using face recognition help write U.S. code

- Amazon German workers to take protest to Seattle HQ

- Baidu made to add warnings as regulators focus on China stks

- London 2014 house price growth to slow as property tax looms

EARNINGS:

- ChinaEdu (CEDU) 4:30pm, $0.86

- FuelCell Energy (FCEL) After-mkt, $(0.03)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Funds See Unprecedented 31% Slump With World Losing Faith

- Brent Crude Rises as Rebels Refuse to Open Libya’s Eastern Ports

- Speculators Most Bullish Since October Before Drop: Commodities

- Copper Reaches Six-Week High as Premium Signals Limited Supply

- Gold Declines as Fed May Start Taper, ETP Holdings Seen Dropping

- Wheat Extends Slump to 18-Month Low as Frost-Damage Risks Wane

- Robusta Coffee Declines as Vietnam May Boost Sales Before Tet

- Indonesia Ore Export Ban Seen Spurring Thousands of Job Cuts

- Copper Market to Stay Broadly in Balance Next Year for Trafigura

- Olam Survives Muddy Waters in Bond Comeback: Corporate Finance

- Libya’s Oil Sales Constrained as Eastern Ports Remain Shut

- Hedge Funds’ Natural Gas Bets Jump as Thermometer Drops: Energy

- Utilities May Want Coal for Christmas as Gas Prices Surge 27%

- Indonesia Ministers to Meet on Ore Export Ban Tomorrow: Hidayat

CURRENCIES

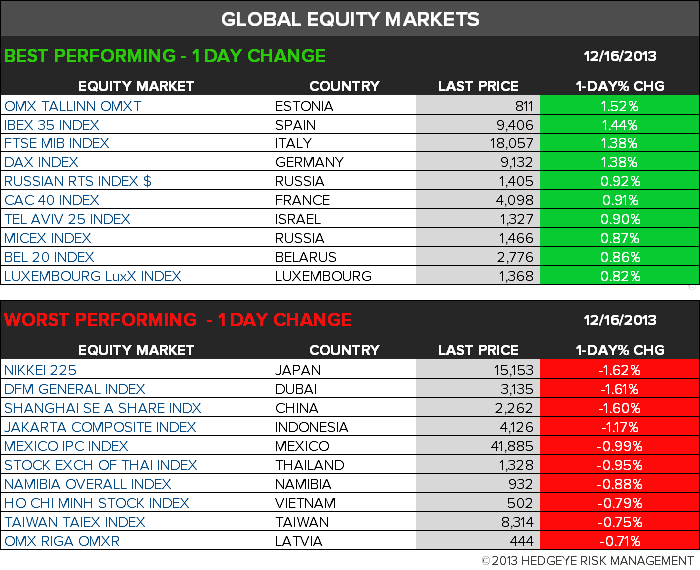

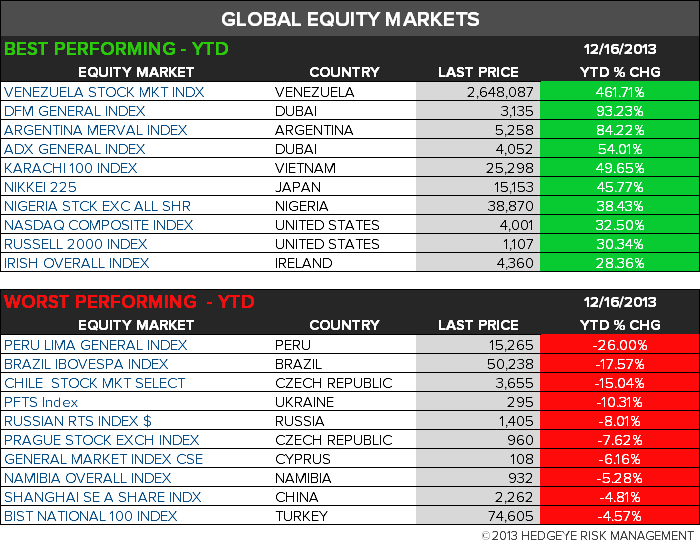

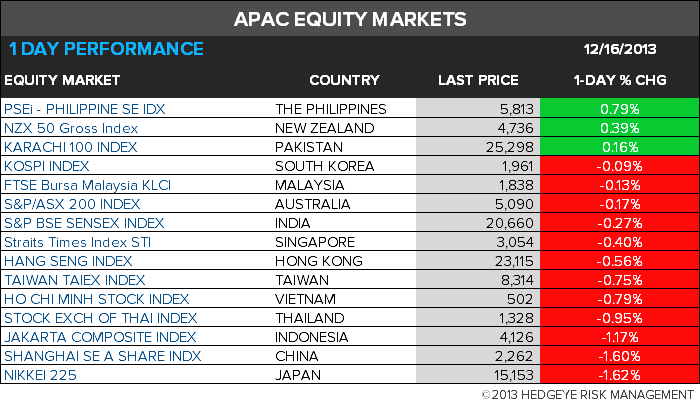

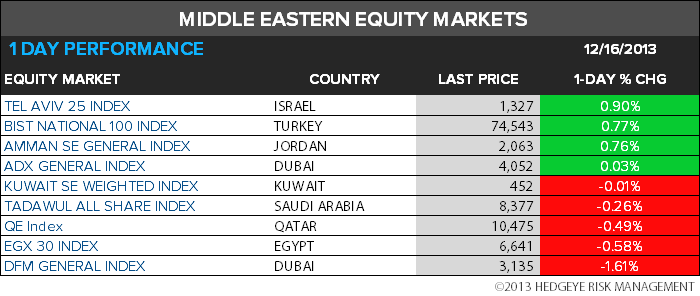

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team