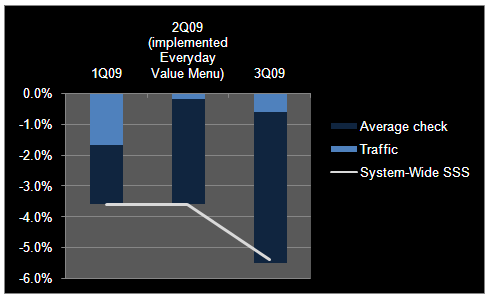

SONC's fiscal 3Q09 top-line numbers came in worse than expectations with system same-store sales down 5.4%. The company was lapping its first quarter of easy sales comparisons, and management set expectations high when it highlighted this fact during its second quarter conference call, saying, "As a reminder, as we move into the third and fourth quarters, our same-store sales comparisons at partner drive-ins will become increasingly easier." Unfortunately, these easy comparisons did not translate into improving same-store sale trends. Instead, comparable sales deteriorated further from 2Q09, down 7.7% at partner drive-ins and -4.9% at franchise drive-ins, and worsened as the quarter progressed with May sales coming in lighter than March and April.

Like last quarter, SONC's declining average check became increasingly problematic. Following the introduction of its Everyday Value Menu in late December, SONC's traffic trends have turned less negative at the expense of its average check, which fell 4.9% in 3Q09 following -3.4% and -1.9% in 2Q and 1Q, respectively.

SONC is not alone in this balancing act between traffic and check with some of its QSR peers choosing to chase traffic at the expense of check and margins (MCD) and others failing to drive traffic with their premium-priced brand strategies (CKR). SONC had allocated all of its advertising dollars to promoting its new value offerings from January to April, which curbed traffic losses, but with its average check declining further, the company reallocated some of its marketing dollars back to its premium offerings in May. And what happened? Traffic was softer in May. Management recognizes that it must work to fix its average check and has introduced initiatives to do so, primarily by trying to re-engage its customers with its higher priced combo meal offerings, but there is no easy fix, particularly in this environment. As management stated, "Value is the number one item driving traffic these days and we need to make sure that traffic is sustained."

SONC ‘s quick success in its ability to drive traffic with the Everyday Value Menu, which grew to 10% of sales within 3 months of its introduction, and the subsequent fall off in traffic in May as the company decreased its marketing spending around the value menu only increases my conviction that CKR will not work in this environment. The company will not be able to drive traffic with its premium menu items. When CKR reports its fiscal first quarter results after the close today, management will continue to maintain that it must protect its brand and will not succumb to selling "margin-eroding" products. We already know that sales trends worsened during the quarter, particularly at Carl's Jr., which were down 5.1%, and I don't see them improving under this current premium sales strategy.

Despite the continued top-line weakness and declining average check, SONC's fiscal 3Q09 margin performance did provide some good news during the quarter. Both restaurant level and operating income margins declined YOY but improved rather markedly on a sequential basis.

The company's refranchising efforts have seemed to help on this measure. In the third quarter, alone, SONC refranchised 177 units, bringing this year's total to 194 and lowering the company's partner ownership mix to 14% from closer to 20%. The positive impact from these refranchising efforts was felt rather immediately as underperforming partner drive-ins that were refranchised had less of an impact on margins and SG&A expenses came down as a percent of sales. As the company benefits from increased royalty revenues and focuses on fixing the fewer partner drive-ins in the system, margins should continue to improve going forward. In the near-term, however, there will some offsets to these margin improvements as the company is facing increased pressure on the labor line in 4Q09 with minimum wage rates set to increase yet again in July. Additionally, although management is expecting commodity costs to come down YOY in the fourth quarter, food costs as a percent of sales are expected to be flat to up as a result of the company's increased contribution from its value menu. SONC has done a good job of managing this food cost line following the introduction of its Everyday Value Menu but we knew it was only a matter of time before margins would take a hit from this new menu.