This note was originally published at 8am on November 21, 2013 for Hedgeye subscribers.

“I love everything about investing except maybe the fact that I’m actually in the investment industry. If you see how sausage is made you probably wouldn’t eat it.” - Yours Truly, ~10 hours ago

One day back in high school my friend Michael decided to start referring to himself as “Mike Nice.” Quoting yourself to jumpstart an investment missive is about as cool as trying to give yourself your own nickname....but the message fits the theme today, I can’t think of anything else and at 4am, questionable ideas have a sneaking ability to cloak themselves as appealing.

Anyway, back to the Global Macro Grind….

It has been difficult to escape the valuation discussion the last few weeks as bubble speculation has been ubiquitous alongside higher nominal, and real, highs for domestic equities. We added our own speculative cogitations to the already teeming cauldron of valuation commentary yesterday (see BUBBLE MONGERING for more) in a note surveying a current cross-section of market valuation measures. We reprise those below, but the takeaway was fairly straightforward - across the balance of metrics, equities are, indeed, moving towards overvalued.

To recapitulate the selection of metrics we considered yesterday:

Shiller PE: The Shiller PE ratio attempts to normalize the price to earnings ratio by adjusting for economic cyclicality. It does so by dividing the price of the S&P500 by the 10Y average of inflation adjusted earnings. At its current reading of 24.9X, the CAPE ratio is moving into the top decile of its historical range. Mapping the Shiller PE by decile vs subsequent market performance suggests return expectations should move systematically lower alongside incremental increases in valuation. Historically, 1Y and 3Y returns progressively decline for each decile change in the Shiller PE (ie. average forward returns by decile decline as multiples move higher).

Tobins Q-Ratio: Longer-term valuation arguments center on the premise that returns on capital should equalize to cost of capital and market values should normalize to economic value. Tobin’s Q ratio is not a measure we use to tactically manage risk, but we can appreciate the intuition underneath its application – after all, why buy an asset when you can “re-create” it for less and compete away existing, excess profit. Currently, the q-ratio sits just below the 1.0 level and approximately 1.0 standard deviation above the long-term mean value – a level that has generally not been a harbinger of positive forward returns historically.

S&P 500 Market Cap-to-GDP: Assuming the collective output of SPX constituents credibly reflects aggregate national production (or serves as a credible proxy for it), the Market Capitalization-to-GDP ratio effectively represents a price-to-sales multiple for the economy. On a historical basis, we are certainly entering “expensive” territory as we push towards breaching 100% to the upside. At current levels we are approximately equal to the 2007 highs and well above the long-term average.

FORWARD/TRAILING P/E: On conventional P/E metrics, the market is moderately expensive currently at 17X trailing earnings and 15X forward earnings. Valuing the market on a single year of (recurrently over-optimistic) forward earnings estimates has its myopic trappings and, additionally, any perceived cheapness in current multiples should be discounted to account for mean reversion downside off peak corporate profitability (more below).

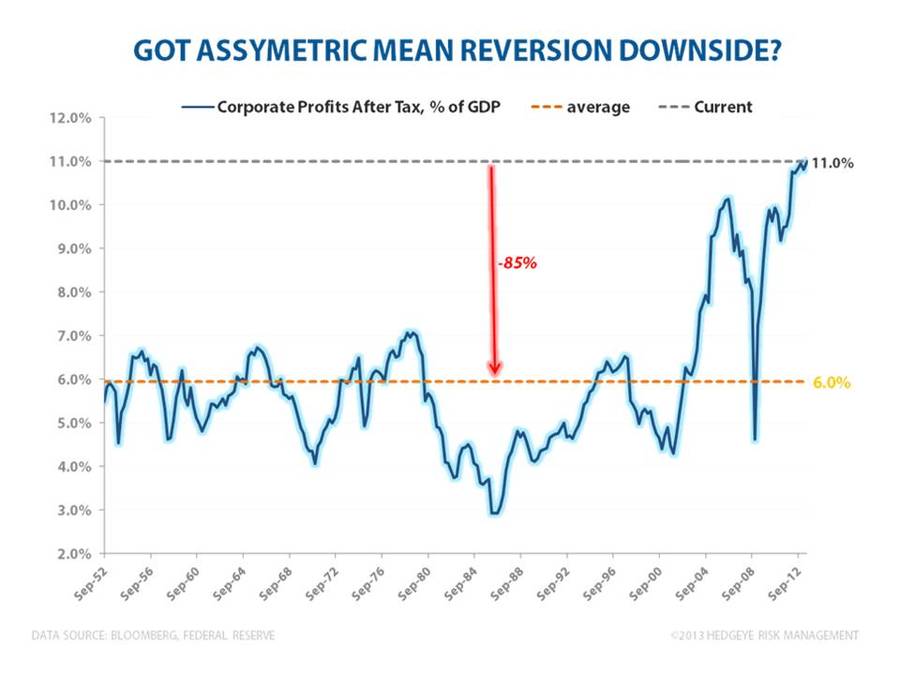

PEAK MARGINS: In the Chart of the Day below we show after-tax corporate profits as a percentage of GDP. The latest 2Q13 data marked another higher high in corporate profitability at 11% of GDP – this is some 85% above the long-term average. Unless you think peak returns to capital provide a sustainable path to aggregate demand growth in the face of negative trend growth in real earnings, trough returns to labor, middling productivity growth and secularly depressed investment spending, then the mean reversion risk for operating margins remains asymmetrically to the downside.

ESTIMATES: Topline growth estimates for the SPX (market weighted) don’t look unreasonable at +4.8% YoY for 2014. However, the slope on earnings growth (+10.9% for 2014) over the NTM continues to look overly aggressive given expectations for further, significant margin expansion (+100 to +250bps in incremental expansion over 2014) above already peak corporate profitability. Of course, iteratively ratcheting down expectations and subsequently beating deflated growth estimates over the course of the year remains the prevailing (and hereto successful) playbook strategy for higher equity prices.

So, generally speaking, we are overvalued. Practically, what do you do with that?

A chief problem for the bear camp is that that the overbought-overvalued market narrative has become a tired one as moderately elevated valuation has characterized most of 2013 and prices advancing at a premium to profits is not a new phenomenon.

Valuation-in-isolation narratives are some of the sell-sides finest sausage and sirenic when expertly crafted. But Valuation isn’t a catalyst.

At Hedgeye, we use a broad range of valuation and sentiment indicators when contemplating the direction of markets and where our view sits in the context of current prices, consensus estimates, and prevailing sentiment. From an Investment decision making perspective, valuation sits somewhere near the middle-bottom of the our consideration hierarchy.

We get that valuation matters in anchoring return expectations over the longer term. Underneath the technicals, acute policy catalysts, and reflexivity that drives immediate and intermediate term price trends sits the steady drumbeat of fundamentals and an accordion-like tether to ‘fair value’.

However, Price, not deviation from estimated intrinsic value, together with our view on marginal changes in macro fundamentals are the signals we use to risk manage immediate and intermediate term exposure.

With the Price signal bullish (SPX and all nine S&P sectors in Bullish Formation) and fund flows, decent domestic and global macro data, rising M&A activity, near universal acknowledgement of the existent ‘bubbliness’ (can you really be in the terminal stage of a bubble if everyone agrees it’s a bubble?), and the lack of a discrete negative catalyst all supporting equities in the immediate term, we’ll continue to lean long until the price signal changes.

Tops are process and we have continued to Buy The Bubble on shallow corrections within our published risk ranges while taking down our gross and net equity exposure since the No-Taper announcement in September. We’ll probably continue to run tight and #RemainActive as yesterday’s FOMC Minutes only extended the confused communication policy out of the Fed.

Raise some cash. Embrace the uncertainty and volatility of it all. Don’t eat the sausage. Eat a snickers… Don't invest like a Diva.

Our immediate-term Risk Ranges are now as follows:

UST 10yr Yield 2.67-2.83%

SPX 1762-1802

DAX 9139-9266

Nikkei 14779-15388

VIX 11.98-14.28

USD 80.62-81.37

Christian B. Drake

Associate