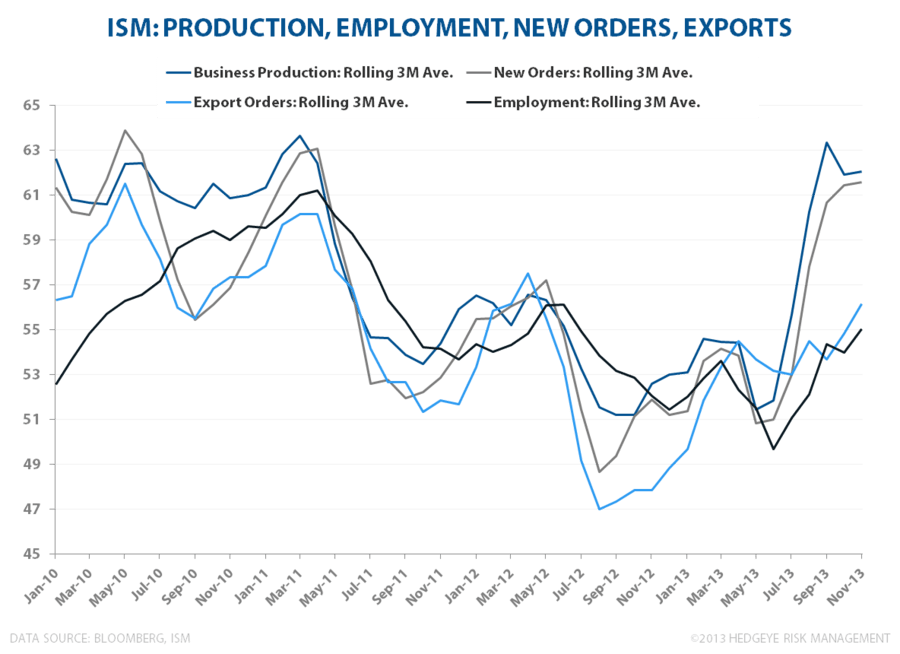

Yesterday's headline ISM reading for November improved +0.9 month-over-month to 57.3, marking another year-to-date high and the highest reading since April of 2011.

Strength was pervasive across the sub-indices as the New Orders and Employment series hit their highest levels since April 2011 and April 2012. Supplier Deliveries remained unremarkable at a middling 53 while inventory levels improved to 50.5 in November from 52.5 prior. Reported respondent commentary was generally positive as well (Here)

Whether incremental strength in November could be partially attributed to deferred demand coming back online post the government shutdown resolution in October remains equivocal. While October durable goods data showed a discrete deceleration, headline ISM advanced in October with Business Production, New Orders and Employment declining only modestly.

Notably, in the ancillary index aggregates, backlogs continued to rise and the export index advanced for a third straight month (highest since Feb 2012) as demand from outside the U.S. continues to support domestic manufacturing activity.

It’s not particularly surprising to see manufacturing gains outpace services gains domestically with household personal income and spending growth still constrained (largely stemming from sequestration and ongoing negative government employment growth) and European growth accelerating.

While any reading >60 is solid, we’ll be interested to see if New Orders can make a higher high in December or if we get a repeat of August and another short cycle top as we head into the 2014 iteration of the budget/debt ceiling tragicomedy.

In the more immediate term, with the dollar correlation to equities holding moderately negative, the market remains largely myopic in its focus on the implications of the macro data for prospective policy adjustments.

* * * * * * *

For more information on how you can subscribe to Hedgeye research click here.