Our Top Q413 Global Macro Theme remains #EuroBulls.

The heart our #EuroBulls call is a bullish position on the GBP and EUR versus the USD and a bullish position on UK and German equities, built on a few central factors:

- Central Bank Intervention: we expect Janet Yellen to remain the ueber dove on policy and push out any QE taper expectations to at least late in Q1 2014, which should burn the Greenback lower (etf UUP).

- BOE “Hawks”: we expect Mark Carney and the BOE to remain on hold with interest rates and the asset purchase target, built on improving UK fundamentals, which should encourage the British Pound higher (etf FXB).

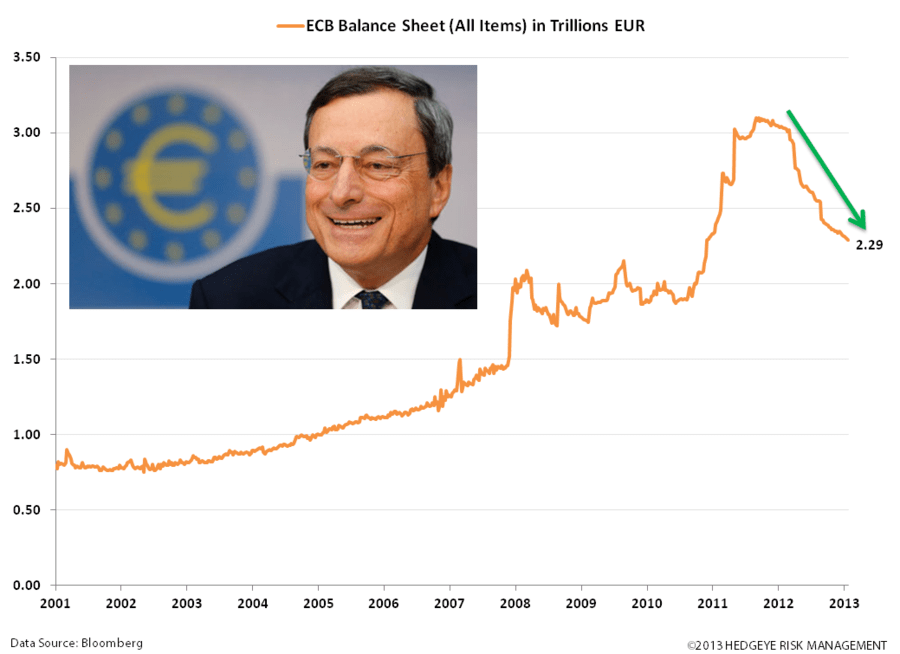

- Draghi’s Back Pocket: we were surprised (and off-sides) with the ECB’s decision to cut the interest rate 25bps on 11/7. The cross has since corrected and we like the set-up on the long side. Twisting an expression, we don’t think it pays to ‘Fight the ECB’: Draghi has balance sheet flexibility with LTRO repayments to unlock additional sovereign and banking bailouts, if needed (etf FXE).

- Island Insulation: the UK was the first country to issue austerity in Europe -- we’re seeing the threw-put of that decision with fundamentals improving ahead of its European peers. We maintain a bullish bias on UK equities (etf EWU).

- German Leadership: Chancellor Merkel is formalizing coalition talks with the SPD; alongside her Finance Minister Schaeuble we see strong continuity of policy vis-à-vis the EU with the new coalition. We’re seeing strong domestic economic health from Eurozone’s largest economy and we expect the country to benefit as the region recovers off a low base. We’re buyers of Germany’s stability (etf EWG).

Just Charts - Below we show the data we’re seeing that is supportive of our #EuroBulls call:

- GDP Taking the Turn: before we highlight the economies of Germany and the UK, we’ll note that we’re seeing a broader improvement from the Eurozone region. In the next charts, the turn (to the positive) is underway!

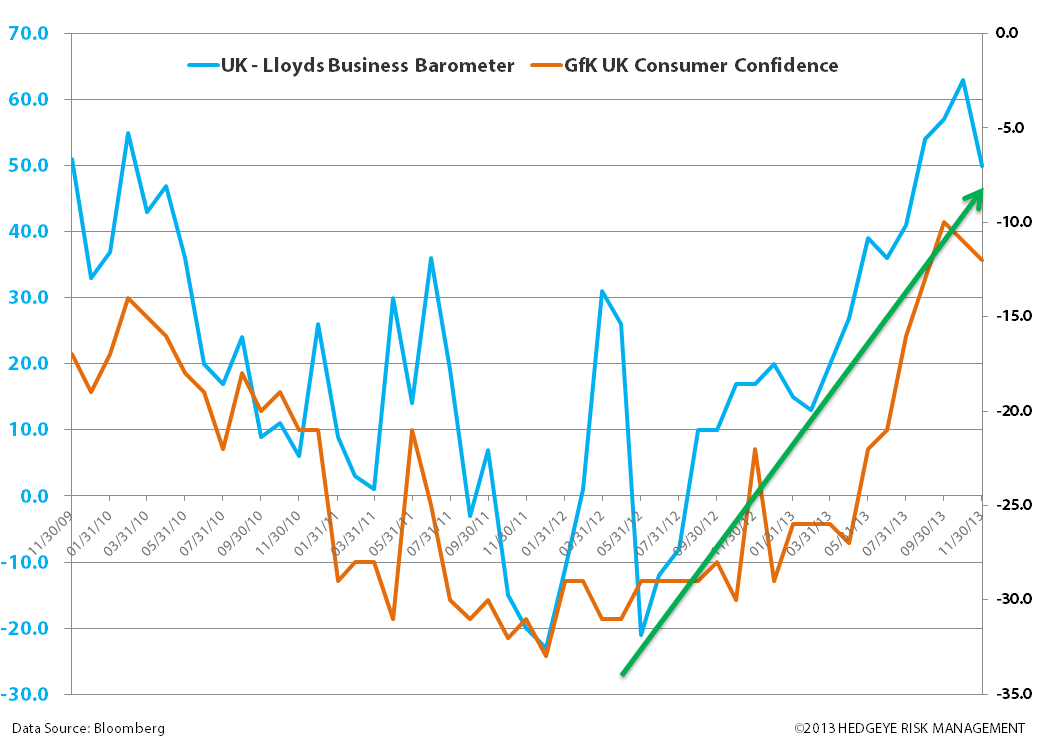

- Confidence Ramping: From economic to business and consumer, the improvement in confidence readings is hard to ignore.

- Even Autos are getting a bounce: Any increase in big ticket items is a signal of confidence to us.

- PMIs Popping: the improvement in confidence is backed by stronger Services and Manufacturing PMIs. Despite underperformance from France, we expect the Eurozone aggregate to cruise about the 50 line (expansionary), and the UK and Germany to outperform.

- Risks Abates: an additional positive signal comes from tightening credit spreads, approaching levels last seen when Europe’s sovereign ‘crisis’ began. While risk is not completely off the table, either on the sovereign or banking sides, we’re seeing compelling improvements. All European sovereign CDS are down on the month and, on average, European Financials have tightened by 46 bps or roughly 21% on the month.

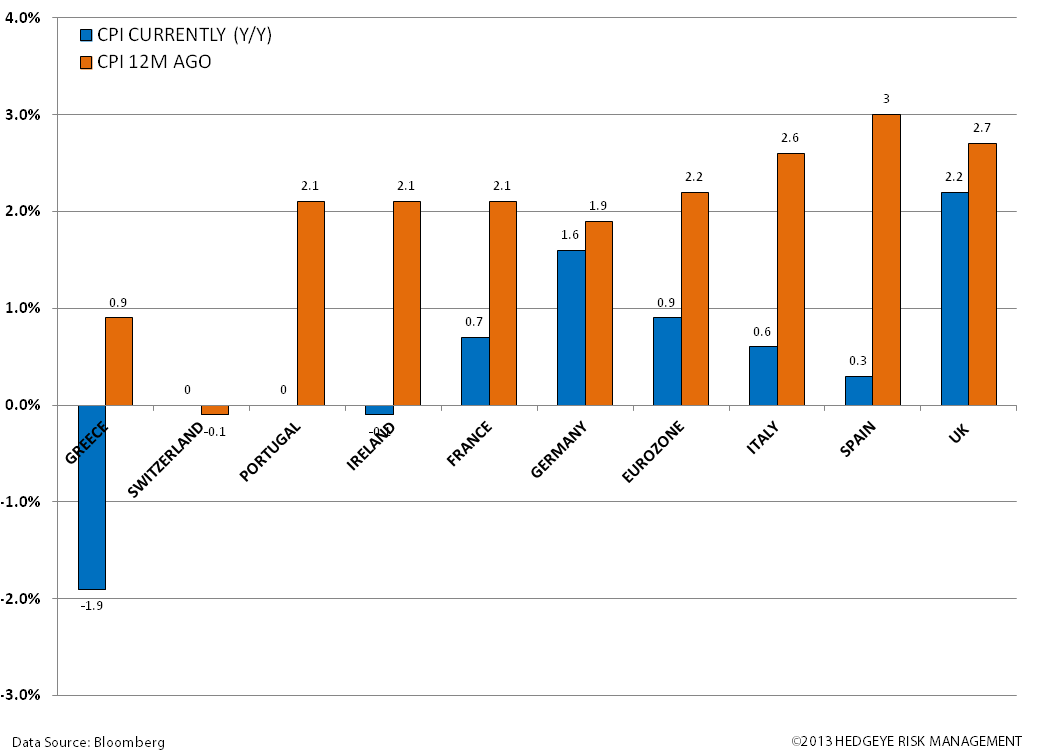

- Deflating the Inflation: we view deflation of the inflation as a lower consumption tax that will boost real inflation adjusted growth. Clearly the ECB has failed to meet its mandate of CPI at or below 2%, however CPI at its current 0.9% is not a “threat” of deflation in our opinion. Despite the ECB’s surprise cut to the interest rate on 11/7, we see no need for the central bank to cut further as fundamentals are showing improvements.

- Draghi’s Back Pocket: Our new mantra is don’t ‘Fight the ECB’ because 1). Time and time again it has not paid to, and 2). Draghi has even more balance sheet flexibility now with LTRO repayments coming in. Don’t forget our central position has been that Eurocrats want to keep the Eurozone experiment alive – this includes at all costs, be it for additional sovereign and/or banking support.

- Credit Thin: This chart remains a thorn in Draghi’s side. Getting credit to flow into the system to households and non-financial corporations has been a great challenge. We don’t expect the ECB to issue another round of LTRO, given its shortcomings in this respect, but we could foresee an alternative to the LTRO with more outlined lending requirements.

- The TREND is Your Friend: our quantitative lines in the sand on the EUR/USD have not moved much in Q4. The currency crashed on Draghi’s unexpected rate cut on 11/7. It has since rebalanced and we like it on the long side as fundamentals improve and the EUR marginally wins out versus the USD in the #CurrencyWars (etf FXE).

- UK GDP: we expect outperformance versus most of its European peers, built largely on it choking down austerity first during the great recession. The European Commission in its autumn report recently raised UK GDP expectations, to +1.3% in 2013 from +0.6% and to +2.2% in 2014 versus a previous estimate of +1.7%. We’re buyers of UK equities (etf EWU).

- UK CPI Eases: Inflation has moderated to 2.2%. We think this is an added benefit to consumers and expect a #StrongCurrency to increase purchasing power by deflating imported inflation.

- UK Confidence Confirms the Data, or visa-versa: We see confidence rising alongside high frequency data: Manufacturing PMI for November was the best in in Europe (58.4 versus 56 in October). And Construction PMI shot up to 62.6 vs 59.3 in October.

- UK Manufacturing and Retail Sales: confidence is a huge piece of the consumption puzzle; we see the trend in manufacturing and retail sales moving positively over the intermediate term. Household spending accounts for 62% of GDP in the UK.

- UK Housing May Ease: After taking off like a rocket ship for the balance of the year, the BOE announced on November 28th that it would curtail mortgage lending in its “funding for lending” scheme.

- GBP/USD: the cross is trading comfortably above over our intermediate term TREND level of support of $1.59 and long term TAIL line of $1.57 (etf FXB).

- Strong Germany: we continue to like the DAX, on a positive correlation to the EUR/USD. Fundamentals remain grounded with a low unemployment rate (6.9% vs 12.1% in the Eurozone), CPI at 1.6% Y/Y, expanding exports, strong PMIs and consumer and business confidence, and an inflection in factory orders to the upside (etf EWG).

Matthew Hedrick

Associate