EVENTS TO WATCH

Hedgeye Black Friday Consumer Survey: Focus on JCP. We'll be conducting a follow-up to our prior consumer survey (which helped us call a JCP beat and KSS miss) following Black Friday weekend and Cyber Monday. We'll have results next week, and will have an updated presentation accordingly. If you are interested in our results, please email sales@hedgeye.com, or .

INDUSTRY DATA

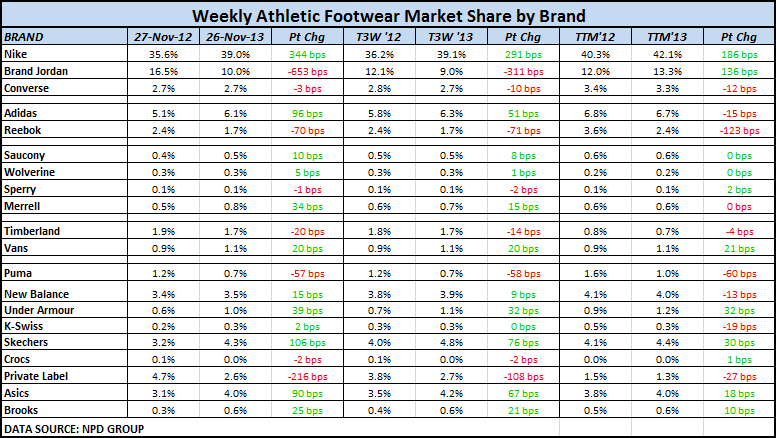

Weekly Athletic Footwear Data

Takeaway: This is a meaningless week as it relates to total industry sales as comparisons don't line up well on the holiday calendar -- ie industry sales decline of 46.5% is hardly representative of reality. But what is relevant is the change in average selling price and market share. As it relates to ASP, we're looking at a 10% boost for the week, which is driven by strength across the board. On the market share front, the best gains continue to belong to Nike and Jordan. It's worth noting that Reebok has taken a notable dive over the past three weeks.

COMPANY NEWS

ARO - Aéropostale Adopts Poison Pill

(http://www.wwd.com/business-news/financial/aropostale-adopts-poison-pill-7292882?module=hp-business)

- "Aéropostale Inc.’s board, which is being pressured by investors to consider selling the company, put a poison pill in place to make sure things don’t move too fast."

- "The New York-based company adopted a stockholder-rights plan Tuesday that allows shareholders to purchase preferred stock if a person or group acquires 10 percent or more of the company, or if a passive institutional investor takes a stake of 15 percent or higher, with some exceptions."

- “'The plan is not intended to prevent an acquisition of the company on terms that the board considers favorable to, and in the best interests of, all stockholders,' the company said. 'Rather, the plan aims to provide stockholders with adequate time to fully assess a takeover bid, and, if appropriate, allow the board time to explore alternatives to maximize stockholder value.'”

Takeaway: If the company is doing this to simply slow down the process and arrive at the best decision for shareholders, then we're ok with the poison pill. But if they're doing it to protect the interest of a very small group of holders (ie management) then we have a major problem with this move.

JNY - Jones Group Sets Deadline for Sycamore

(http://www.wwd.com/business-news/financial/jones-group-sets-deadline-for-sycamore-7293521)

- "The Jones Group Inc.’s board set Sunday as the deadline for Sycamore Partners to submit its final buyout bid, according to a source."

Takeaway: Are we missing something, or does JNY have zero leverage in setting a deadline for anybody to submit a bid? They only have one bidder…if they scare that one away, then they're begging for a 20% decline in the stock. Poor strategic move, in our opinion.

CROX - Crocs Said to Discuss Investment With Funds Including Blackstone

- "Crocs Inc...is in talks with buyout firms including Blackstone Group LP about a possible investment, people with knowledge of the matter said."

- "Proceeds from the sale of a minority stake or debt could be used for a stock buyback, said the people, who asked not to be identified because the information is private. The private-equity investor would then help map out a turnaround plan for the retailer, including having a say over senior management candidates, the people said."

Takeaway: We're sitting here thinking about which business we'd rather own -- JNY or CROX. It's not an easy decision. But the answer is probably CROX. JNY has dozens of brands where consumers hardly know they exist. CROX only has one major brand, but its brand is like Xerox or Kleenex -- as it's synonymous with a single product (that's tough to grow into new categories). CROX probably wins, as the low production cost, low R&D model is scalable globally, even if Americans won't go near the stuff.

SCC - Sears Canada Announces Reorganization of its Repair Services and Parts Business

(http://phx.corporate-ir.net/phoenix.zhtml?c=117881&p=irol-newsArticle&ID=1880385&highlight=)

- "Sears Canada Inc. announced today that, following a comprehensive review of its Repair Services and Parts businesses, it will be implementing a number of significant changes designed to improve efficiency, profitability and the overall customer experience. The changes will take place over the next six months and will result in a workforce reduction of 712 associates."

- "Separately, the Company is also announcing today a staffing reduction in its head office operation, a move to align the Company's support structure with the size and volume of the organization as well as to take advantage of internal processes that have been recently implemented to improve efficiency. The changes affect 79 associates and have been made across various functions of the head office operation."

LVMH - Louis Vuitton Exhibit in Moscow Stirs Controversy

- "A major Louis Vuitton exhibition slated to be inaugurated in Moscow on Friday was the subject of a political maelstrom Tuesday as Communist Party representatives and other officials expressed outrage at the showcase."

- "The venue — a giant structure resembling a vintage trunk, plunked in Red Square — has proven controversial given its proximity to the Kremlin and the presidential residence."

Takeaway: We don't mean to side with the Kremlin on this one, but this one is tough to stomach. Then again, there's generally no such thing as bad press, and the fact that we're talking about it now means that they're achieving their goal. That said, I'm still not buying a LV trunk this holiday.

TGT - Survey: Target.com tops in digital coupon distribution

(http://www.chainstoreage.com/article/survey-targetcom-tops-digital-coupon-distribution)

- Target.com’s coupon distribution page — coupons.target.com - achieved the highest total average daily visits through the first half of 2013, according to an analysis by Kantar Media Marx. This is almost double the number of average daily visits to other key retail websites tracked by Kantar Media Marx.

Moncler - Moncler Sets Price Range for IPO

- "Moncler’s selling partners — ECIP M, controlled by Eurazeo SA; CEP III, controlled by The Carlyle Group, and Brand Partners 2, controlled by Progressio Investimenti — set the price per share between 8.75 euros, or $11.87 at current exchange rates, and 10.20 euros, or $13.84."

INDUSTRY NEWS

comScore: Online holiday spending off to solid start

(http://www.chainstoreage.com/article/comscore-online-holiday-spending-solid-start)

- "For the holiday season-to-date (Nov. 1 - 24), $18.9 billion has been spent online using desktop computers, up 14% versus the corresponding days last year, according to comScore. Tuesday, November 19 was the heaviest online spending day of the season to date at $963 million. Two other shopping days – Thursday, Nov. 14 and Sunday, Nov. 24 – have also seen at least $900 million in online retail spending."

Bangladesh Reform Faces New Obstacles

- "Reform measures aimed at improving conditions in the troubled Bangladesh garment industry face new obstacles as political upheaval takes hold in advance of national elections. The announcement on Monday that the 10th parliamentary election would take place on Jan. 5 set off a series of disturbances on Tuesday, including a 48-hour strike and shutdown of road, rail and sea transportation, and the expectation of more delays in shipments and other disruptions for businesses."

- "The Dhaka Chamber of Commerce and Industry estimates that each day of a strike causes a loss of 16 billion takas, or $206 million, with an average of 50 such days of shutdown a year damaging the ability of the industry."