TODAY’S S&P 500 SET-UP – November 22, 2013

As we look at today's setup for the S&P 500, the range is 20 points or 0.60% downside to 1785 and 0.51% upside to 1805.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.50 from 2.51

- VIX closed at 12.66 1 day percent change of -5.52%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:40am: Fed’s George speaks in Paris

- 10am: JOLTs Job Openings, Sept., est. 3.840m (prior 3.883m)

- 11am: Kansas City Fed Mfg Activity, Nov., est. 6 (prior 6)

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 12:15pm: Fed’s Tarullo speaks in Washington

- 1pm: Baker Hughes rig count

GOVERNMENT:

- President Obama hosts King Mohammed VI of Morocco at White House

- 10:15am: Sec. of Defense Chuck Hagel meets with Canadian counterpart Rob Nicholson to discuss defense relations, sign Canada-U.S. Asia-Pacific Defense Policy Cooperation Framework

WHAT TO WATCH:

- J&J said to narrow bidder list to 3 for diagnostics business

- Robin Hood conf. continues today w/ Ackman, Druckenmiller

- Paulson changes tone to say he won’t add more to gold fund

- Apple recoups most Samsung damages cut from 2012 verdict

- Gap’s profit forecast signals holiday quarter may disappoint

- EMA monthly CHMP announcements today from 7am NY time

- Novartis to buy back $5b in stock, add business segments

- German business confidence rises in sign recovery on track

- Apple supplier Foxconn to invest $40m in Pennsylvania

- Party City readies for IPO in early 2014, Reuters says

EARNINGS:

- Ann Inc. (ANN) 7:45am, $0.87

- Foot Locker (FL) 7am, $0.66 - Preview

- Hibbett Sports (HIBB) 6:30am, $0.65

- PetSmart (PETM) 9:05am, $0.86 - Preview

- Sirona Dental Systems (SIRO) 6:30am, $0.80

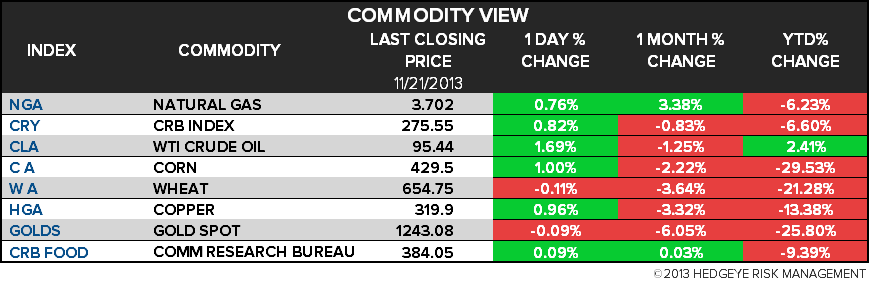

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Paulson Changing Tone Said to Say He Won’t Add More to Gold Fund

- Gold Analysts Most Bearish Since June on Fed Taper: Commodities

- Codelco ‘Optimistic’ on China Copper Demand on Middle Class

- Gold Swings Near Four-Month Low as Investors Weigh Fed Tapering

- WTI Crude Set for First Weekly Gain in Seven; Iran Deal Falters

- Taylor, Jamison Outpace Commodity Hedge Funds Seeing Losses

- Aluminum Fees in Japan Seen Near Record in First Quarter on Abe

- Copper Poised for Weekly Gain on Stockpiles, China: LME Preview

- Rebar Caps First Weekly Gain in Three on Mill Price, Inventory

- Western Bulk Says China Minor-Bulks Rose 19%; Supramaxes to Gain

- Shale Boom Pits U.S. LPG Against Mideast in Asia: Energy Markets

- South African White Corn Climbs to Highest in More Than 7 Months

- Gold Option Wagers on Surge to $3,000 Was Most-Active Yesterday

- German Gold Assets Drop 0.1% in October in First Cut Since June

- Copper Gains Amid Signs Recovery Picking Up as Stockpiles Shrink

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

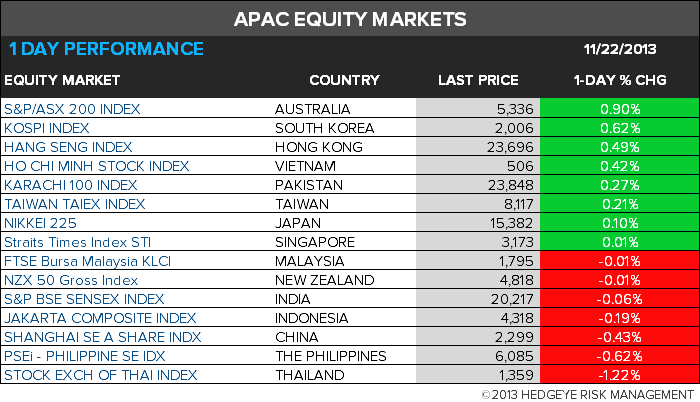

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team