Last night after the close BNNY reported its fiscal Q2 2014 results: the top and bottom lines saw strong sequential and year-over-year growth while gross margin was pressured and frozen pizza results were weaker.

Despite slightly uneven quarterly results we remain bullish on the company as its 2H outlook stands to benefit from product roll-out, and COGS and SG&A efficiencies, including from its acquisition of Safeway’s manufacturing plant (announced 3 days ago) in Joplin, Missouri, where the company has been producing over 50% of its snacks business since inception in 2002. The purchase price is $6M, plus the cost of inventory and supplies at the close – it is expected to be an all cash transaction.

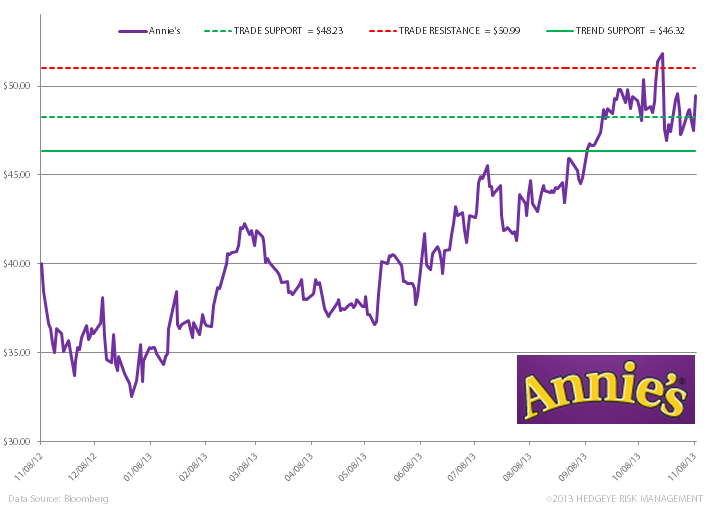

From a quantitative set-up, our levels below show the price of the stock comfortably trading above our immediate term TRADE and intermediate term TREND support levels. We remain buyers of the stock on weakness, however today wasn’t that day with the stock up intraday over +5%!

What We Liked:

- Net Sales of $58.7MM, up +25.7% Y/Y

- EPS of $0.28, up +21.7% Y/Y

- Expected 2H improvements in cost structure through Safeway manufacturing plant acquisition

- Base business continues to be strong; and company said already seeing strong performance from rollout of new microwavable mac & cheese cups and family-size frozen entrees in the quarter

- Expect stronger pizza sales heading into winter, typically larger for the category

- Despite Gross Margin hiccup in the quarter (-240bps Y/Y and -140bps Q/Q), we expect 2H and FY to be more normalized Gross Margin

- Fiscal 2014 Outlook: expects net sales toward the upper end of previous 18% to 20% range; expects adjusted diluted EPS toward the lower end of previous $0.97 to $1.01 range

What We Didn’t Like in the Quarter:

- Continued struggled with its pizza business

- After a voluntary pizza recall in January 2013, in the quarter the company overshot on inventory, and had to sell at discount (we chalk this up to growing pains)

- Again saw impact from roll-out of new products on Gross Margin

Matthew Hedrick

Associate