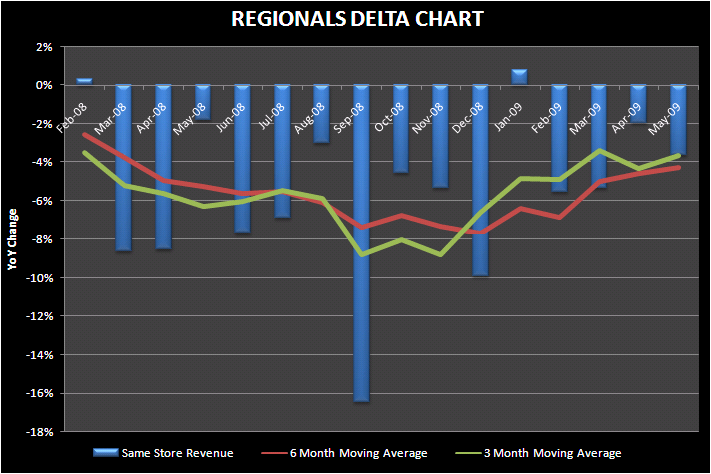

I feel a little uneasy about regional gaming revenue trends. It's not so much that May was disappointing. It was with same store revenue falling 4%, but the comp was the most difficult of the year after February. On the other hand, June is a much easier comp. June of 2008 was down 7% versus May 2008 down only 2%. I don't want to get bogged down on monthly revenues but it feels like the January positive pivot has stalled out.

Beyond the June easier compare, the catalysts look negative:

- With the lapping of the IL smoking ban and the removal of the MO loss limit, shouldn't numbers be better? May in Missouri was very disappointing. Same store revenues fell despite the loss limit removal and the faster than expected ramp up at Lumiere Place.

- Gas - 50 straight daily increases? This has to have an impact. As we wrote about in our 06/29/08 note, "GAS PRICES AND THE ECONOMY DO MATTER", gas prices are a statistically significant variable. Every 1% increase in gas prices causes a 0.15% decline in gaming revenues. Gas prices on average were down an average of 39% YoY year to date through the end of April. Unfortunately, gas prices have increased 30% over the last 50 days. The precipitous drop in gas prices in the first third of the year may have masked more serious issues in gaming spend. More on this in an upcoming note.

- Sequential comps - We'll look at 2 year comps when June comes out. May started out strong and trailed off in the second half of the month.

- Government transfer season is over - Tax refunds and other transfer payments have already made their way into consumers' pockets. We'll see how sustainably stimulating that stimulus will be.