Conclusion: FNP remains one of our top ideas, and as we stated Wednesday, we think that a $40 price tag next year will be a simple checkpoint on its way to $75. We've got to admit, we were half-hoping for a sell-off on the (usual sloppy) GAAP numbers, as this is a classic 'add on weakness' stock. We initially thought we'd get it, as the margin performance was less than inspiring, and the GAAP EPS number missed by $0.02. But clearly that sell-off did not happen. The market is finally at a point where it gives a free pass to (i.e. it doesn’t care about) anything that's not Kate Spade, and it lauds management's capital infusion into Kate -- even if it comes with margin degradation. Our take on the company and the stock is almost identical to what it was before the print -- except that we took our numbers (which were already the highest on the Street) up by about 10%. We remain extremely bullish on FNP, and though we'd ideally like to buy more on a pullback, we're increasingly doubtful -- at least from a fundamental vantage point -- that we'll get that chance.

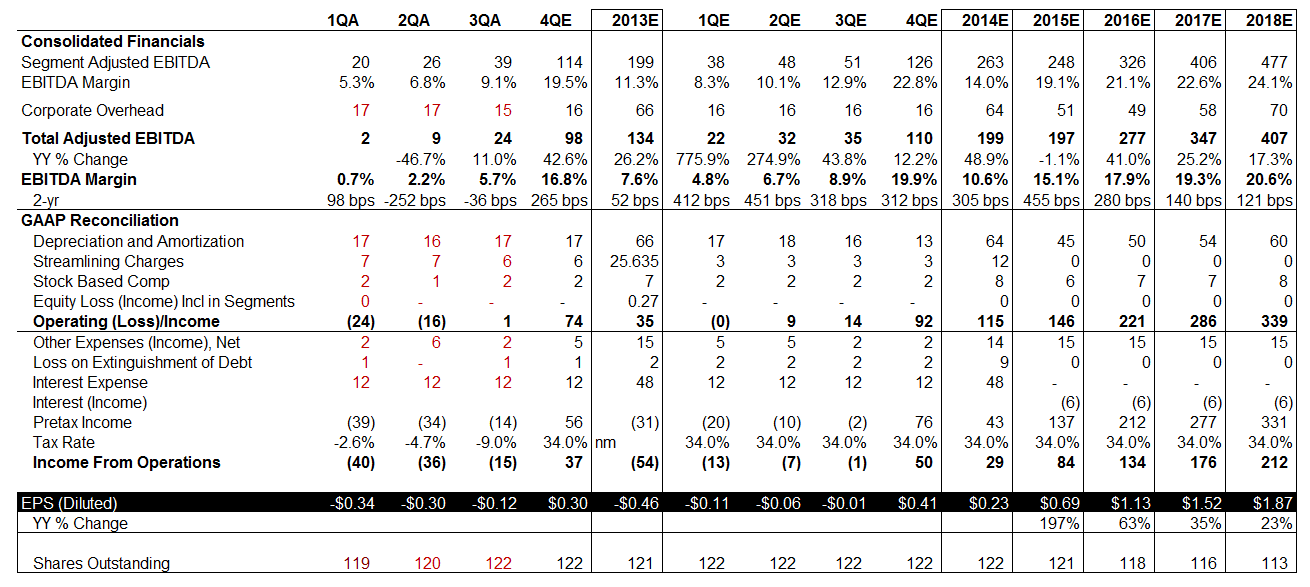

Here's our key modeling assumptions that get us to $1.85 by 2018.

- In addition to Juicy being kicked out of the portfolio by mid-'14, we assume that both Lucky and Adelington are sold off by the end of '14. We assume $475mm in gross proceeds for the pair.

- Proceeds go to pay down debt, leaving FNP (net) debt free by 2015.

- We assume the Corporate comes down from its current $66mm run rate to $50mm by the end of next year. We're going against the grain with management's comment that corporate will be 4-5% of sales. You don't boot 58% of revenue without taking a commensurate whack out of overhead. We know management is hyper focused on this. Ultimately, a 24% cut in Overhead (to $50mm) with a 58% cut in revenue seems fair.

- We assume that Kate Spade goes from 196 stores today to 551 over our modeling time horizon.

- On top of that, we have sales productivity going from about $1,200/square foot today to $2,000. This is completely doable for Kate Spade and Jack Spade. We're on the fence with Kate Spade Saturday, as it targets a customer that does not have the same level of disposable income. Nonetheless, if Saturday becomes such a meaningful part of the mix and dilutes price point, our store addition numbers will prove conservative. Six of one, half dozen of another.

- We conservatively assume that new Kate stores open at 40% of the productivity level of existing stores.

- We've got Kate's EBITDA margins going from 16%-24%. There's about 4% of 'DA' in there, so we're really talking an EBIT margin of 20%. We're extremely comfortable with this given the 29% level at KORS and 31% at COH (even though COH should be closer to 20% in order to actually grow its revenue).

- We assume that streamlining charges (which we're getting tired of) go away at the end of 2014.

- We've got interest expense turning into interest income. Only $6mm per year…but hey, they're coming off of $48mm in annual debt service. It matters.

- While this won't be a share repo machine (it's all about growth) we have the share count beginning to come down in 2015 as FNP uses some cash to pluck away at its share count.

- Growth is expensive, so in our cash flow assumptions, we have capex going from 5.5% of sales today to 10% off a much higher sales base. That equates to around $200mm. We're all for that level of spend. The returns are clearly there.

HERE'S OUR NOTE FROM EARLIER THIS WEEK

11/06/13

FNP: 3-Bagger. Add on Weakness

Even after the big move we still think that FNP is a BIG idea, with 3x upside over a 3-4-year time period. That said, we’re neither here nor there on tomorrow’s print. Here’s our thinking into tomorrow…

- FNP remains one of our favorite TAIL ideas, as we think that 1-2 years out the stock starts with a 4 (versus $27.66 today).

- But we don’t feel strongly about it one way or another headed into tomorrow’s print.

- This company gives guidance based on what it thinks it can hit, not on what it can beat. Our point is that if we want to get sucked-in to the game of ‘beat by a penny/miss by a penny’, this can literally go either way.

- There’s not likely to be an announcement on the sale of Lucky or Adelington with the release, though we’ll likely get added color on terms surrounding the previously announced sale of Juicy. All in, don’t expect any thesis-shifting strategic announcements.

- Our bigger picture call is simple. Kate Spade (which accounts for all of FNP’s EBIT) is going from $700mm in revenue at a 12% EBIT margin (with leverage), to $3-4bn in revenue at a debt-free 20% margin. We think people have the revenue trajectory partially correct, but they’re still way too low on the margin. In the end, consolidated EBIT will go from break-even (currently hurt by divisions that are on the block) to $800mm. The stock is expensive on earnings today, but is trading at 3.4x its $900mm EBITDA number.

- The punchline on this name is that an 8x EBITDA multiple on our $900mm EBITDA number gets us to a stock of about $75 vs the current $27.66. It won’t happen overnight, as we all know stock moves aren’t linear, but will grind higher quarter after quarter, year after year.

- This has been and will continue to be the perennial ‘I missed it’ stock for investors, who subsequently watch it go up another 25% in their face.