Summary: The strength in headline GDP is belied by rising inventory accumulation and decelerating consumption growth. Residential Investment drove further acceleration in total Private Investment while Government Expenditures and Net Exports both returned to positive GDP contributions. All in, domestic economic activity was largely flat sequentially with the headline print modestly overstating underlying strength.

REAL GDP: +2.8% QoQ (vs. 2.5% prior and +2.0% expected)

C: Consumption growth decelerating to +1.5% QoQ from 1.8% last quarter. Contributed +1.04 to Total GDP. Sequential growth in Durables was strong, NonDurables moderate, Services flat

I: Investment growth accelerating to +9.5% QoQ. Biggest contributor to Total GDP at +1.45.

G: Government expenditure growth moving back to positive (barely) after 3 qtrs of negative growth. Contributing 0.04 to Total GDP.

E: Exports (+4.5% QoQ) growing at a premium to imports with Net Exports contributing +0.31 to Total GDP.

Inventories: Inventories helped juice Headline GDP growth with inventory accumulation providing a positive contribution of +0.8 to GDP. Up from a positive contribution of +0.4 last quarter.

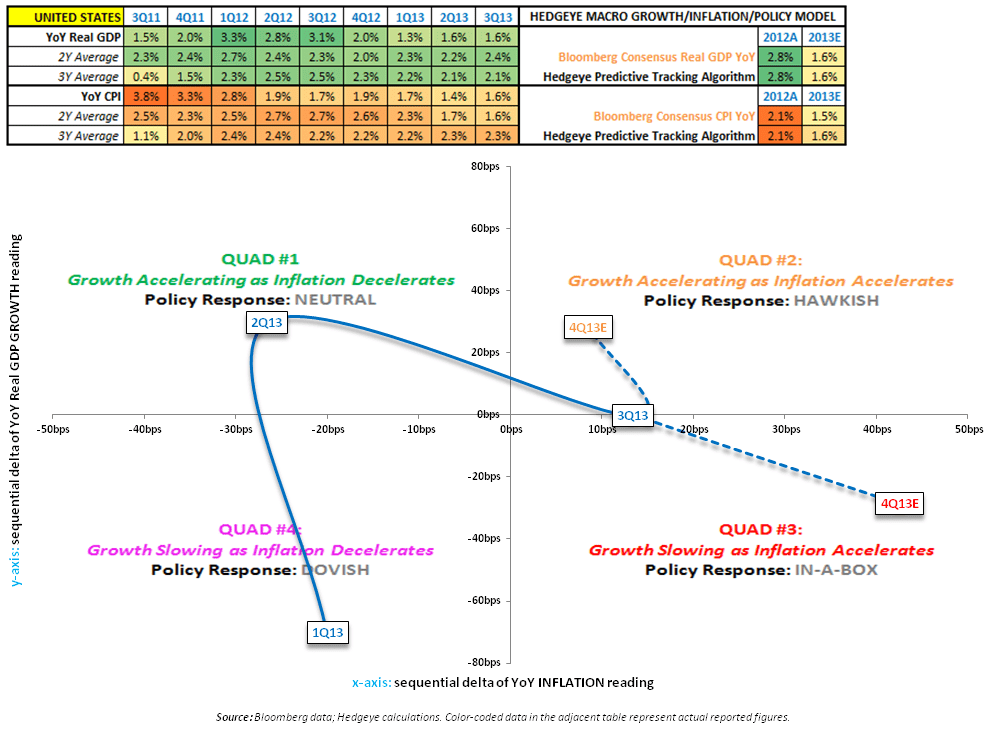

Inflation: Core PCE Inflation accelerated to 1.4%, off the near record low of 0.6% recorded in 2Q13. With Core PCE remaining the Fed’s preferred inflation reading, at 60bps below the 2.0% target, inflationary pressures should not serve as a constraint to a continuation of easy policy.

Real Final Sales (GDP less Inventory Change): Still healthy at +2.0% QoQ vs +2.1% in 2Q

Gross Domestic Purchases (GDP less exports, including imports): Flat sequentially at 2.5%

Real Final Sales to Domestic Purchasers (GDP less exports less inventory change): In measuring total U.S. demand from both domestic and international sources this measure, arguably,offers the cleanest read on the health of the domestic private sector. Growth in Final Sales to Domestic Purchasers decelerated modestly from 2.1%in 2Q13 to 1.7% 3Q13.

Consumption: Consumption growth decelerated 30bps QoQ to +1.50% in the third quarter – the lowest pace of growth since 2Q11.

The deceleration was not unexpected as disposable personal income growth, and consumer spending by extension, was constrained in 3Q by the ongoing reduction in the federal workforce and the implementation of sequestration related furloughing of federal employees.

Federal job loss and furloughing has not been inconsequential as salary and wage income for government workers (~17% of the national workforce) has been growing at -0.6%.

Private sector personal income growth has emerged as a positive offset, however, with wage/salary income accelerating in recent months. Forthcoming results out of the bipartisan budget committee (tasked with finding a budget resolution and alternate path to sequestration) in early January 2014 will have a meaningful impact on the trajectory of household disposable income and aggregate consumption growth.

Given the existing constraints, and a rising savings rate, consumption growth in 3Q13 could probably be best characterized as 'decent'.

We’ll provide an update on consumer income/spending alongside the detailed release tomorrow.

Christian B. Drake

Associate