This note was originally published November 04, 2013 at 07:46 in Daily Trading Ranges

Editor's note: What follows below is a complimentary look at Hedgeye's Daily Trading Ranges. Every morning, DTR subscribers receive our proprietary buy and sell levels on major markets, commodities and currencies. Click here to learn more and subscribe.

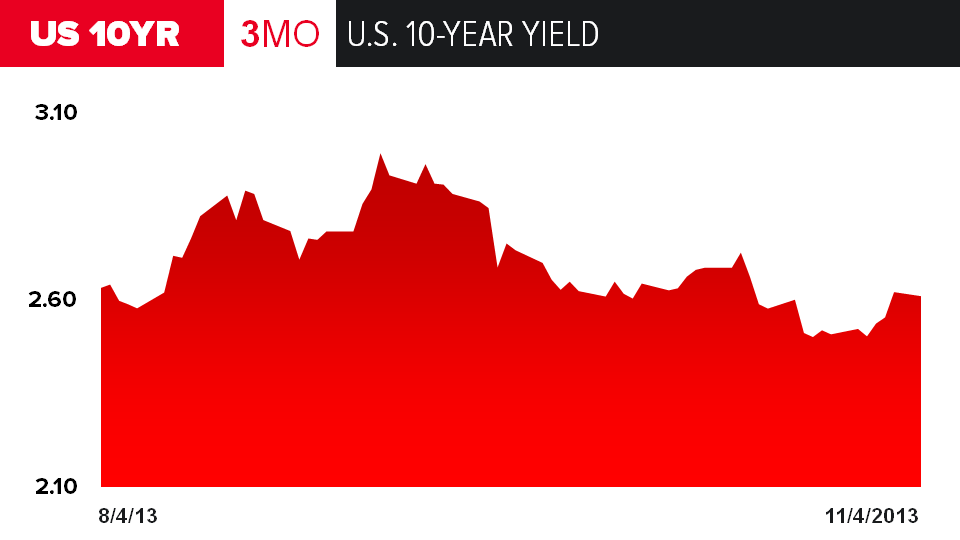

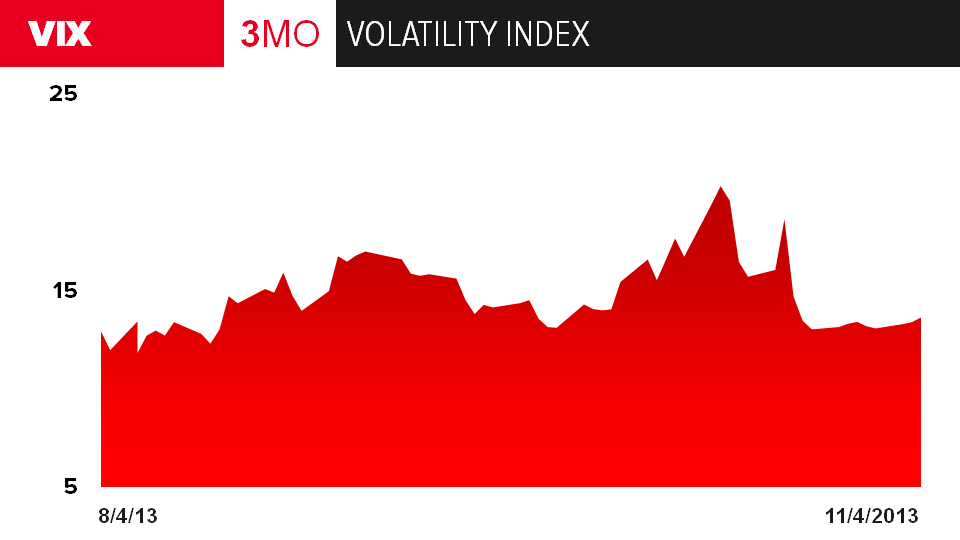

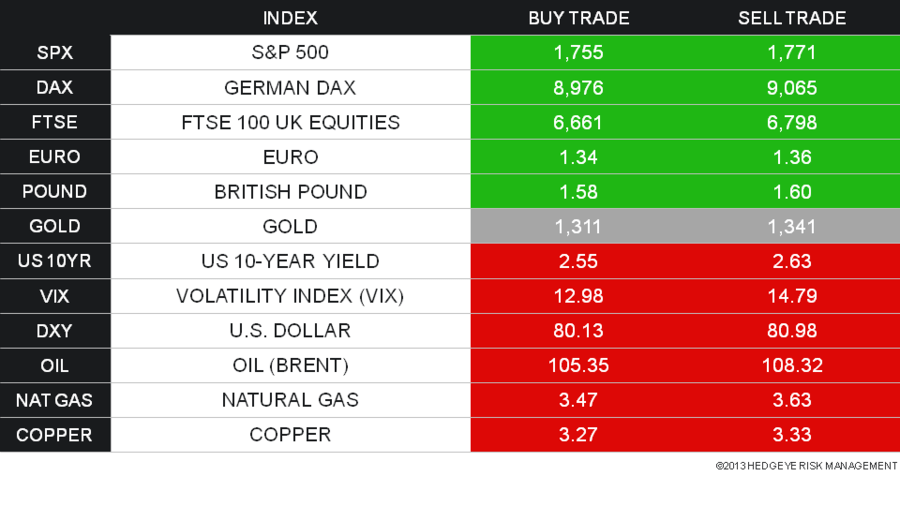

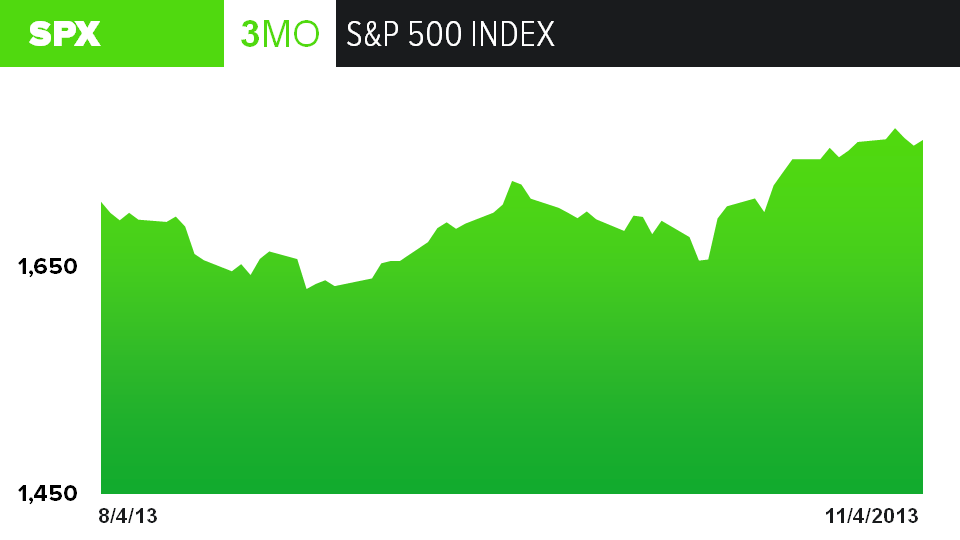

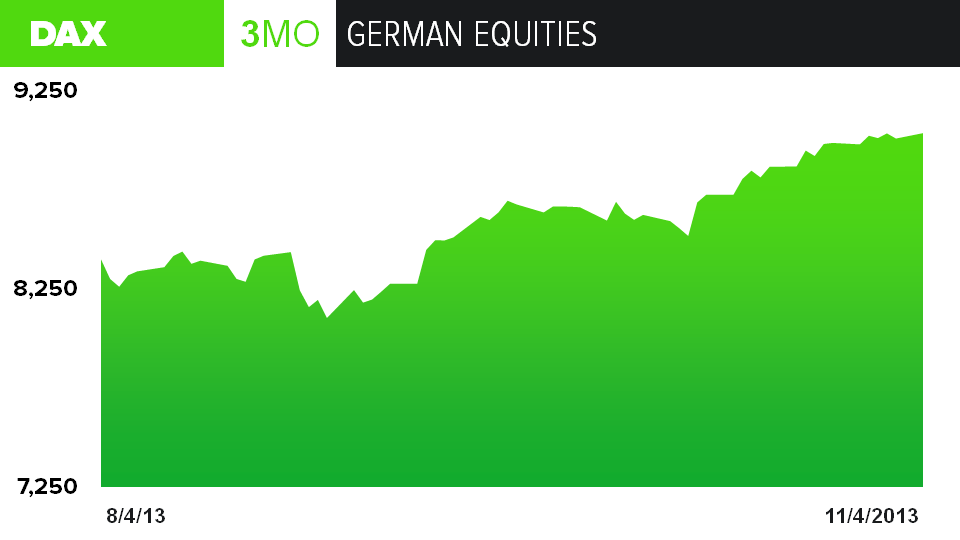

(Click to enlarge)

BULLISH TRENDS

BEARISH TRENDS