A quick data flow management update here as it relates to the U.S.

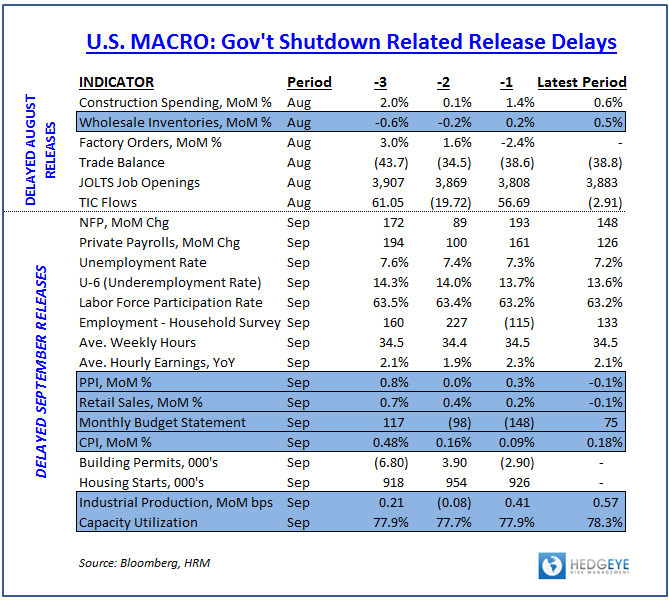

This week was a fairly heavy one for domestic macro data, but much of the flow consisted of delayed government sourced data releases playing catch-up post the government shutdown.

Immediately below is the summary list of delayed releases by period with this week’s releases highlighted in blue. A more detailed highlight of the week’s data follows.

Next week’s domestic macro calendar is equally heavy as we get ISM services for Oct, the latest read on Personal income and Spending, the advance 3Q13 GDP estimate, the 1st monthly read on confidence post the government shutdown resolution, and the BLS Employment data for October. Plenty of speculative fodder for the Taper tea-leaf reading contingent.

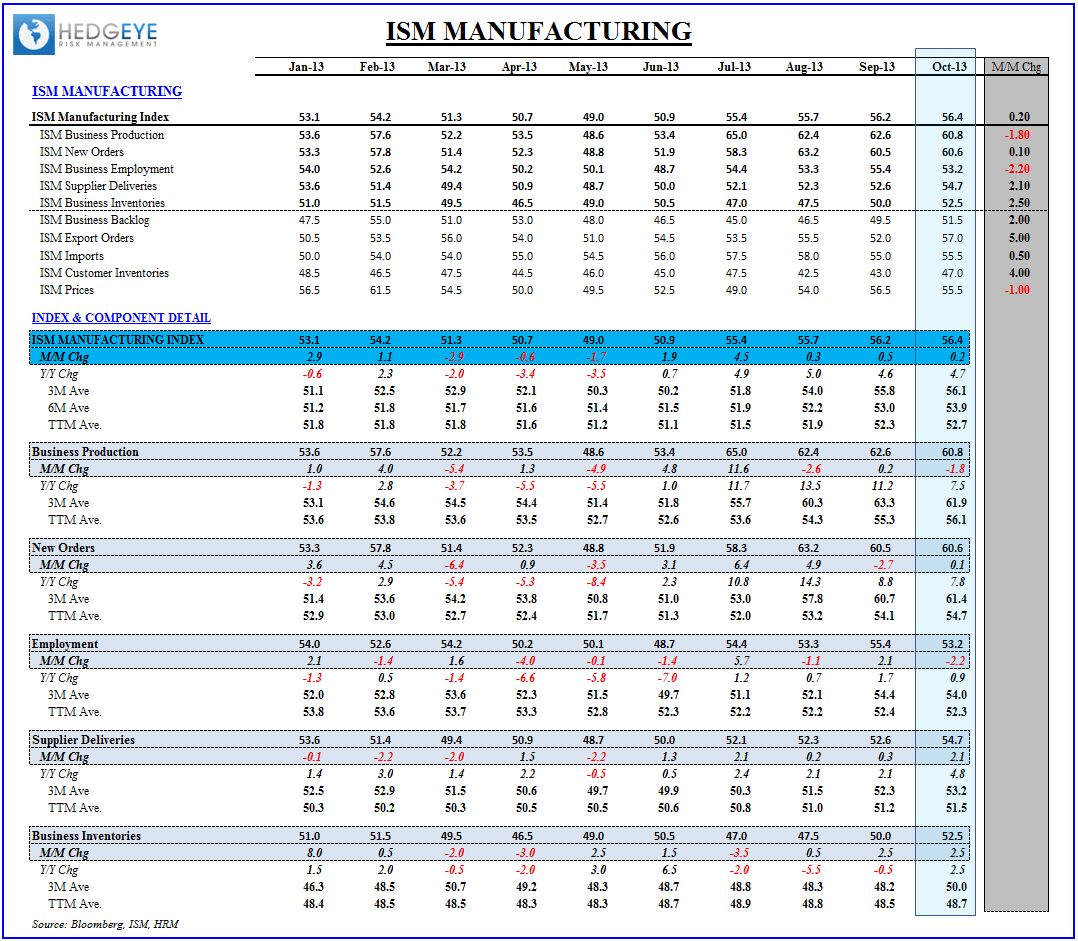

ISM: Strongest Reading Since April 2011

Today’s ISM Manufacturingrelease – the 1st and most consequential private sector release of the month – showed domestic manufacturing activity remained healthy to start the fourth quarter. The composite indexed advanced 20bps MoM to its highest level since April 2011 with new orders holding >60 for a 3rd consecutive month.

Manufacturing and consumption of goods has accelerated and helped to provide an offset to muted services consumption growth as real disposable personal income growth has remained constrained alongside (still) lackluster private sector wage inflation and the negative, furlough/sequestration impacts at the Federal level.

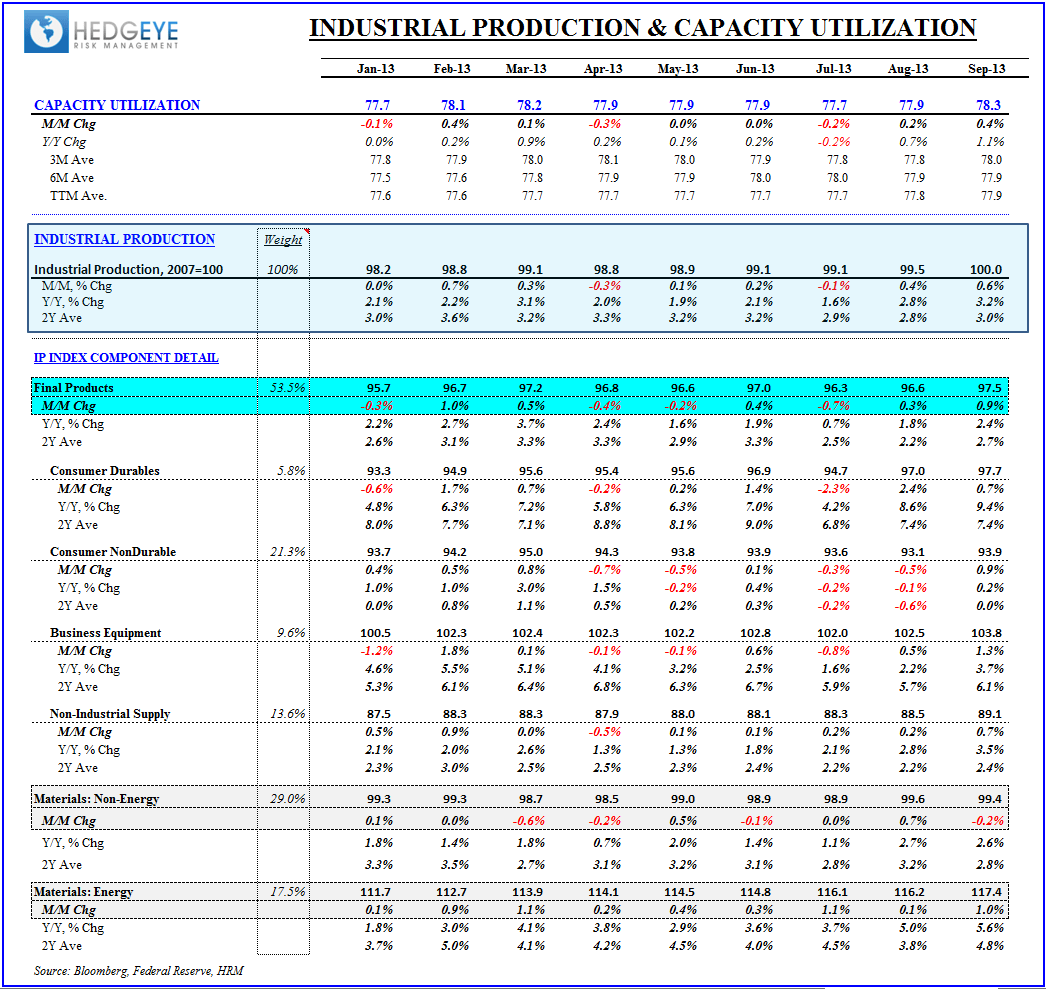

INDUSTRIAL PRODUCTION & RETAIL SALES: Delayed, September IP and Retail Sales numbers reflect the same trend prevailing in the (leading) ISM data for October.

- Retail Sales: Headline Retail Sales declined in September but that was mostly on the back of sequential weakness in auto sales as Retail Sales ex-Auto’s and ex-Autos & Gas both improved sequentially. At the industry level Food and beverage gained against an easy comp and Electronics were strong with i-products and the Grand Theft Auto release helping support sales in the category.

- Industrial Production: Solid print as Industrial Production and Capacity Utilization hit their strongest levels since Feb. 2008 and July 2008, respectively. Growth in Durables (6% weight) decelerated sequentially on a MoM basis but accelerated on a YoY and 2Y basis while growth in NonDurables (21% weight in Index) accelerated sequentially, moving back to positive growth after two consecutive months of decline.

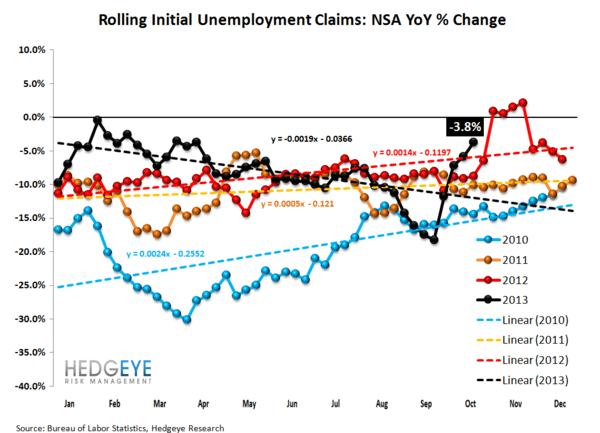

Initial Claims: Inconclusive

Taking this week’s figures at face value, the labor market appears to be decelerating modestly. However, it’s unclear whether the the distortive impact of the CA technology upgrade issue has fully resolved.

If California has, indeed, trued up its backlog of unprocessed claims in full than the observed deceleration in labor market improvement could be taken to accurately reflect deterioration in organic trends. If, on the other hand, a residual drag from the computer upgrade persisted through the latest week, we would expect a return to trend line improvement (approx -10% YoY) over the next couple weeks. The picture should be clearer next week when we get the state level data.

Please see this weeks note: INITIAL CLAIMS: INCONCLUSIVE for detail.

Christian B. Drake

Associate