TODAY’S S&P 500 SET-UP – October 31, 2013

As we look at today's setup for the S&P 500, the range is 16 points or 0.47% downside to 1755 and 0.44% upside to 1771.

SECTOR PERFORMANCE

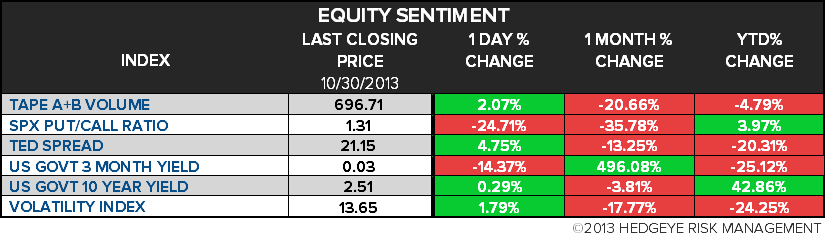

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.21 from 2.22

- VIX closed at 13.65 1 day percent change of 1.79%

MACRO DATA POINTS (Bloomberg Estimates):

- 7:30am: RBC Consumer Outlook Index, Nov. (prior 50.7)

- 8:30am: Init. Jobless Claims, Oct. 26, est. 338k (prior 350k)

- 9am: ISM Milwaukee, Oct., est. 53 (prior 55)

- 9:45am: Chicago Purchasing Mgr, Oct., est. 55 (prior 55.7)

- 9:45am: Bloomberg Consumer Comfort, Oct. 27

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural-gas storage change

GOVERNMENT:

- President Obama to speak on private-sector jobs, new business investment at Commerce Dept.’s Select USA Investment Summit

- NRC, FEMA meet to discuss preliminary draft changes to Emergency Preparedness Criteria

- 10am: Sen. Banking Cmte hears from Fed-New York’s EVP on revising guarantee for mortgage-backed securities

- 10:15am: Sen. Foreign Relations Cmte. holds hearing on Syria

WHAT TO WATCH:

- Facebook to limit ads as younger teens using site less

- Deficit in U.S. narrows to five-year low on record revenue

- ECB makes crisis cash lines at central banks permanent backstop

- Morgan Stanley said to take 30% stake in Mitsubishi UFJ firm

- Bank of Japan sticks with campaign of record monetary easing

- Starbucks forecast trails ests. as Asia gains slow

- Goldman shrinking pay shows Wall Street poised for bonus gloom

- Citigroup, JPMorgan said to put currency dealers on leave

- Oracle pay under fire from pension funds before annual meeting

- Twitter mum on profit has roadshow attendees questioning value

- Visa profit matches estimates as $5b buyback plan is set

- Allstate profit slides 57% on loss tied to sale of life unit

- Metlife misses estimates as insurer incurs costs in Australia

AM EARNS:

- Advance Auto Parts (AAP) 8:30am, $1.42

- Alamos Gold (AGI CN) 6am, $0.07

- Alpha Natural Resources (ANR) 7am, $(0.76) - Preview

- AmerisourceBergen (ABC) 7am, $0.74 - Preview

- Avon Products (AVP) 7:01am, $0.19 - Preview

- Barrick Gold (ABX CN) 6:30am, $0.50 - Preview

- Beam (BEAM) 7:30am, $0.58

- Bell Aliant (BA CN) 6am, C$0.42

- Belo (BLC) 6am, $0.12

- Bombardier (BBD/B CN) 6am, $0.10

- Boyd Gaming (BYD) 7am, $0.01

- Cardinal Health (CAH) 7am, $0.85 - Preview

- Catamaran (CCT CN) 6am, $0.48

- Cigna (CI) 6am, $1.62

- Clorox (CLX) 8:30am, $1.01 - Preview

- ConocoPhillips (COP) 7am, $1.45 - Preview

- Discovery Communications (DISCA) 7am, $0.73

- Enterprise Products (EPD) 6am, $0.69

- Estee Lauder (EL) 7:30am, $0.73 - Preview

- Exxon Mobil (XOM) 8:02am, $1.77 - Preview

- GrafTech International (GTI) 7:04am, $0.02

- Harman International (HAR) 8am, $0.84

- Hillshire Brands (HSH) 7:30am, $0.35 - Preview

- Imperial Oil (IMO CN) 7:55am, C$0.99

- Incyte (INCY) 7am, $(0.09) - Preview

- Invesco (IVZ) 7:30am, $0.52

- Iron Mountain (IRM) 6am, $0.30

- LKQ (LKQ) 7am, $0.25

- Magellan Midstream Partners (MMP) 8:02am, $0.59

- Marathon Petroleum (MPC) 7:14am, $0.63

- MasterCard (MA) 8am, $6.94

- MGM Resorts (MGM) 8am, $(0.03) - Preview

- Mylan (MYL) 7am, $0.79 - Preview

- New York Times (NYT) 8:30am, $(0.03)

- NII Holdings (NIHD) 6:30am, $(1.17)

- NiSource (NI) 6:30am, $0.17

- Ocwen Financial (OCN) 7:30am, $1.09

- Perrigo (PRGO) 7:44am, $1.39

- Pinnacle West (PNW) 8am, $2.17

- PPL (PPL) 6:57am, $0.68

- Quanta Services (PWR) 6:07am, $0.45

- Realty Income (O) 9:15am, $0.61

- SCANA (SCG) 7:30am, $0.92

- TECO Energy (TE) 7:30am, $0.33

- Teradata (TDC) 6:55am, $0.70

- Teva (TEVA) 7:30am, $1.25

- Time Warner Cable (TWC) 6am, $1.64 - Preview

- TransAlta (TA CN) 7:45am, C$0.18

- Valeant Pharmaceuticals (VRX CN) 6am, $1.41

- ViroPharma (VPHM) 7:30am, $0.15

- Western Refining (WNR) 6am, $0.50

PM EARNS:

- American International Group (AIG) 4pm, $0.96

- Apartment Investment & Management (AIV) 4:05pm, $0.50

- Camden Property Trust (CPT) 4:17pm, $1.02

- DCT Industrial Trust (DCT) 4:10pm, $0.11

- Fairfax Financial (FFH CN) 5:02pm, $4.26

- First Solar (FSLR) 4:02pm, $0.95 - Preview

- Fluor (FLR) 4:05pm, $1.03

- Kodiak Oil & Gas (KOG) 4:01pm, $0.23

- Mohawk Industries (MHK) 4:01pm, $1.90

- MRC Global (MRC) 4:01pm, $0.45

- Newmont Mining (NEM) 4:43pm, $0.32 - Preview

- Northeast Utilities (NU) 4:15pm, $0.73

- Omega Healthcare (OHI) 6pm, $0.62

- ON Semiconductor (ONNN) 4:05pm, $0.16

- Piedmont Office Realty Trust (PDM) 5:02pm, $0.35

- Public Storage (PSA) 5:05pm, $1.89

- Republic Services (RSG) 4:10pm, $0.49

- Southwestern Energy (SWN) 4:30pm, $0.50

- Standard Pacific (SPF) 4:02pm, $0.12

- Trimble Navigation (TRMB) 4:05pm, $0.36

- Western Forest Products (WEF CN) Aft-mkt, C$0.04

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Crude Trades Near Four-Month Low as U.S. Stockpiles Climb

- Oil Gambit Helps India Mining Billionaire Lead Rio: Commodities

- Palm Oil Has Biggest Monthly Gain in Three Years as Supply Drops

- Gold Extends Decline as Fed Sees Growth While Keeping Stimulus

- Copper Heads for First Monthly Drop in Four on Taper Speculation

- Cocoa Pares Fourth Monthly Gain as Demand for Halloween Is Over

- Rebar Posts Monthly Loss on China’s Weak Winter Demand Outlook

- Wheat Declines to Four-Week Low as India Seen Boosting Shipments

- Barrick to Stop Pascua-Lama Mine Construction to Conserve Cash

- Exchange Failure Prompts Commodity Bourse Audit: Corporate India

- West African Oil Surge to Asia Seen Threatened: Energy Markets

- Singapore Challenged as LNG Hub by Trading Delay: Southeast Asia

- Copper 2014 Forecasts Slump to Low on Supply Additions: BI Chart

- Glencore Xstrata Says Third-Quarter Copper Output Gains 34%

CURRENCIES

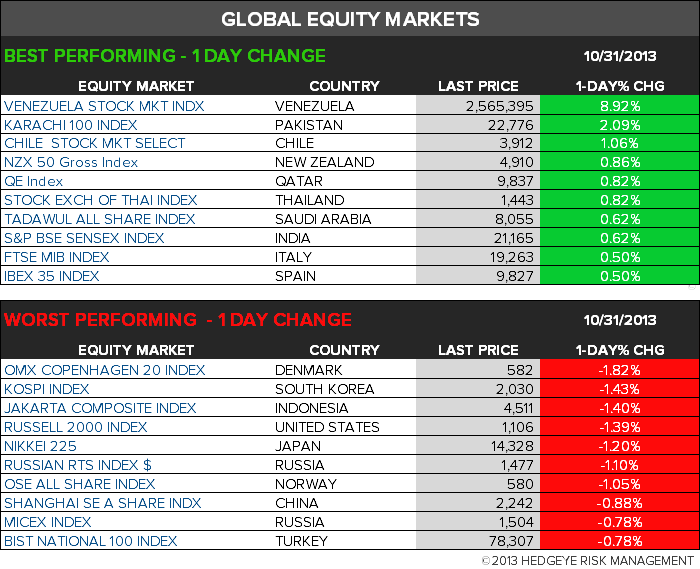

GLOBAL PERFORMANCE

EUROPEAN MARKETS

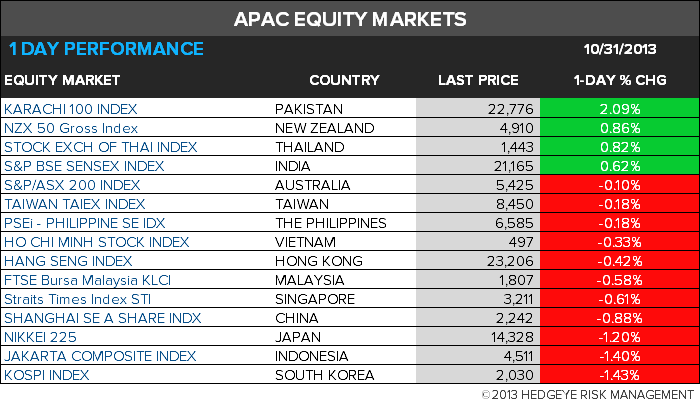

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team