We believe we’ve been very clear on how this will end for DRI, we just don’t know the timing. As analysts, trying to advocate for significant change, the biggest issue we need to deal with in the immediate-term is business trends. We can summarize the current trends in two words – not well!

The being said, the FY2Q114 earnings call will be the most important call of CEO Clarence Otis’ career. His ability, or inability, to handle the current pressure should help shed light on the timing of future events.

On some level, we believe the case for significant change at Darden could be strengthened on December 20th, when the company reports FY2Q14 results. In our view, current street estimates remain disconnected from reality. The current estimate for DRI's FY2Q14 is $0.22 and we believe that $0.12 - $0.15 is a better number.

Below, we share incremental thoughts on DRI’s fundamentals.

- The 2nd quarter is traditionally the lowest for the company, seasonally.

- Seafood inflation will accelerate meaningfully q/q and will continue for the balance of the year.

- Same-restaurant sales trends have been disappointing so far.

- DRI has not introduced any new promotional items and still has the promotional items that have not been working.

- There is no cohesive plan to fix the crown jewel – Olive Garden.

Sales Trends

For the year, Darden is still guiding to sales growth of +6-8% and blended same-restaurant sales growth for the Big 3 to be +0-2% -- this is after the company reported -2.3% blended same-restaurant sales growth in FY1Q14. The current consensus estimate for blended same-restaurant sales growth in FY2Q14 is +0.6%. Given anemic casual dining trends and DRI’s lack of a cohesive strategy to fix the core business, we believe these estimates may be off by 1-2%.

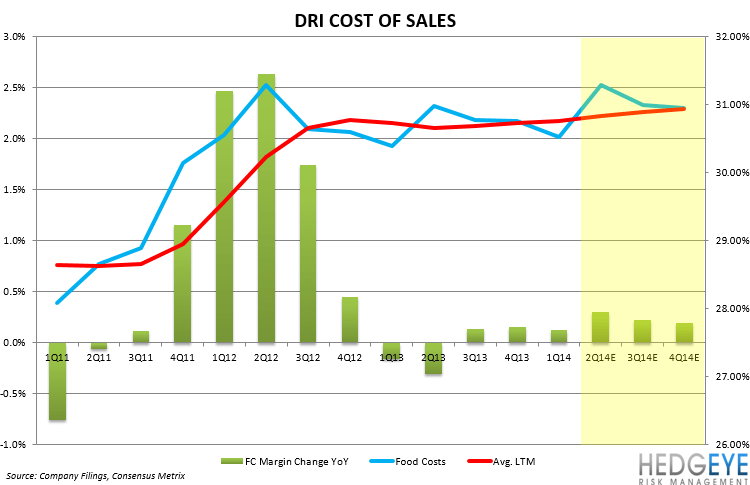

Food Costs – Seafood Inflation Acceleration

Management Commentary on the FY4Q13 Earnings Call – June 2013

“In terms of specific food categories and items, total seafood prices for fiscal 2014 are expected to be higher than fiscal 2013, because of the shrimp supply disruptions.”

Management Commentary on the FY1Q14 Earnings Call – September 2013

“Seafood inflation was normal in [FY1Q14], but we now expect double-digit inflation in the second, third, and fourth quarters, primarily related to the shrimp production issues in Asia. The source of the problem has been identified, but getting solutions in place is taking a little longer than we expected when we spoke to you in June.”

As you can see, management was not prepared for the spike in shrimp costs back in June. Fast forward to September, and management finally realized there is going to be a significant increase in shrimp costs. Red Lobster is currently promoting Endless Shrimp Tuesday’s, which is very likely to pressure margins in the quarter.

Labor Cost Deleverage

Current consensus estimates are for labor costs to increase +30 bps y/y in the quarter, after increasing over +100 bps y/y in each of the last three quarters. In FY1Q14, restaurant labor expenses were +100 bps higher due to lower average wage inflation, reduced productivity and sales deleverage at Olive Garden and Red Lobster. Given the current sales trends, we do not see how the trends in FY2Q14 are going to improve sequentially.

Other Expenses

Other restaurant expenses have been up significantly (+100 bps on average) for the past four quarters, due to the acquisition of Yard House and other reasons. Currently, street estimates are for other expenses to increase +10 bps y/y in FY2Q14. In our opinion, this estimate does not fully account for a large enough impact from sales deleveraging at Olive Garden and Red Lobster.

G&A – The Wild Card

In an effort to cut some fat from the company cost structure, we are expecting to see approximately a $7 million (net) expense associated with G&A cuts in FY2Q14.

Howard Penney

Managing Director