This note was originally published at 8am on October 14, 2013 for Hedgeye subscribers.

“Even when you have three strikes, you’re still not out. There is always something else you can do.”

-Tony La Russa

This weekend I read Malcolm Gladwell's most recent book, "David and Goliath - Underdogs, Misfits and the Art of Battling Giants." Now many of my academic friends are critical of Gladwell suggesting he cherry picks studies, but I sort of take his books for what they are: a compendium of interesting studies. Ultimately, it is up to the reader to accept or not accept his conclusions.

As the title denotes, his most recent book is about perceived underdogs overcoming serious odds. He discusses why certain learning disorders may actually improve the chances of success of individuals (causes them to focus more intently), discusses the long term impact of California's three strikes laws (not positive for communities), analyzes how unconventional tactics in basketball can lead to outsized success (more full court pressing!), and a number of other interesting topics.

One of the topics I found most interesting was the long run analysis of success in military conflicts. As Gladwell writes, suppose you were to look at the conflicts that happened between very large countries and much smaller countries over the past 200 years. In fact, let’s assume the size difference was 10x. How often would you assume the larger country wins?

Logically, and intuitively, it would seem likely that with that type of size advantage the larger country would dominate and likely win the conflicts close to 100% of the time. The reality is much different as the weaker countries have won almost 29% of the time.

Even more insightful is the fact that the weaker side wins 64% of the time when employing unconventional, or guerrilla attacks. Put another way, if the United States were to go to war with my home country of Canada (about 1/10 the population of the United States), you should put your money on Canada to win if the Canadians employed guerrilla tactics

Back to the global macro grind ...

We've had our own David and Goliath battle this year at Hedgeye as our Senior Energy Analyst Kevin Kaiser has taken on a couple of billionaire CEOs by making short calls on Linn Energy and the Kinder Morgan companies. As always, even though we believe our research supports a revaluation lower of both companies, time and Mr. Market will determine whether this call, versus the views of the energy Goliaths, is the right one. (Ping us at sales@hedgeye.com if you’d like to learn more about subscribing to the energy vertical.)

More practically, in investing, a bet against Goliath is often a bet against consensus. Internally we run a number of screens to assess whether we are with or against consensus on any of our Best Ideas. As an example, is if company has 30 ratings from Wall Street and 29 of them are Buys that is likely more supportive of a short thesis, and conversely make us question whether we have differentiated enough insight to justify it as a stock to own. Thinking unconventionally in investing is just as important as it is in warfare.

The conventional thought according to the global macro pundits this morning is that some form of U.S. default is imminent. This chatter has reached such an extreme that this morning Bloomberg was actually comparing the U.S. to the last major nation to completely stop paying back its debt – Nazi Germany. Certainly, we have a good degree of respect for Bloomberg (in fact we all use their terminals), but a comparison like that seems erroneous, at best.

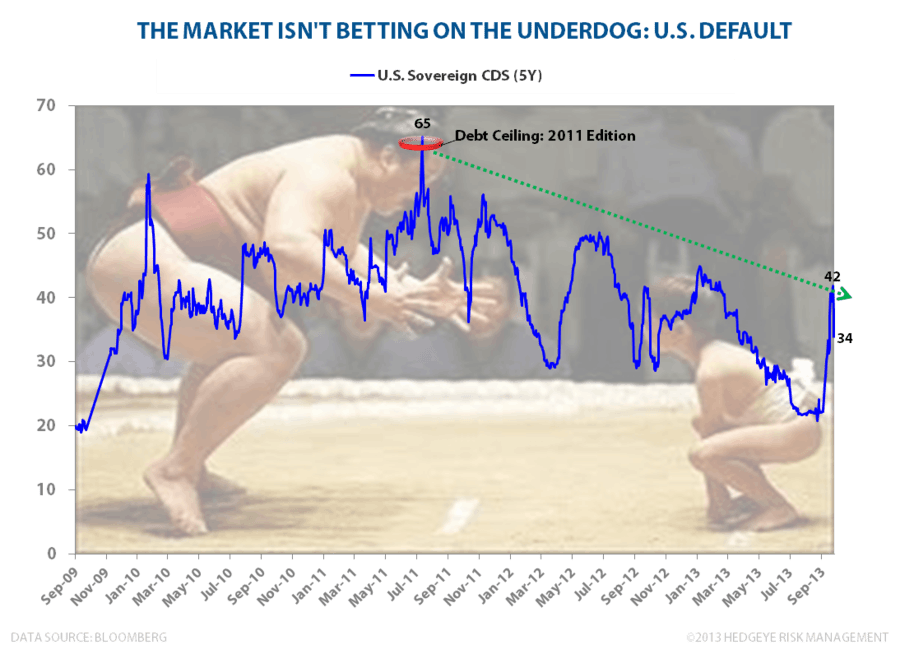

In the Chart of the Day, we once again look at credit default swaps for 5-year U.S government debt. Not only are CDS not at the same heightened levels of 2011 when they peaked at near 65 basis points, they are actually well off recently levels and currently trading at 34 basis points. Given all of the fear mongering this weekend and headlines of discord in Washington D.C. perhaps they will spike again, but, certainly there is literally no chance that the U.S. government turns her back on the U.S. government debt obligations according to this market tell.

That all said, just because the probability of debt default is unlikely doesn’t mean you should be aggressively long of risk assets. We trimmed the exposure in our real-time alerts products late last week going from a 3:1 long/ short ratio to 1:1. Now most money managers can’t move this fast for reasons of scale, but the fact remains this is a market that will reward those who trade around positions.

This is especially relevant broadly to the hedge fund industry this year. According to Cambiar Investors LLC, shares that have been the most shorted are up 38% since the start of the year. This is almost double the return of the SP500 in the same period. Furthermore, according to the HFRI Equity Hedge Fund Index, hedge funds are up only 9.2% in the year-to-date. So far anyway, this has been a tough year for hedge funds to earn their 2 and 20.

In part it has been challenging for hedge funds and other active managers to out-perform because the variance between sectors has been abnormally low. In our Q4 themes deck we show this graphically and the data indicated that this year is the second lowest year going back to 1990 for variance between sector returns at 0.50%. The lowest was 2006 at 0.27%. The historical mean since 1990 is 2.25%. So if there is one asset allocation bet you might want to consider, it is to #GetActive as sector variance is likely to only increase from these abnormally low levels.

Good luck out there today and feel free to ping us if you want to discuss how this week might play out from a catalyst perspective down in the nation’s capital.

Our immediate-term Risk Ranges are now:

UST 10yr Yield 2.61-2.71%

SPX 1683-1708

ShangHai Comp 2191-2247

VIX 15.19-18.98

USD 80.11-80.69

Brent 110.04-111.99

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research