Floating lower, for now

In the UK, where fixed rate loans of durations over 10 years are not typically available, floating rate and variable mortgage products comprise a significant portion of the total. According to the Council of Mortgage Lenders, fully 49% of total mortgage debt in the UK is either variable, discounted variable (a variable rate with a teaser) or a tracker, which follows the BOE rate in lock step.

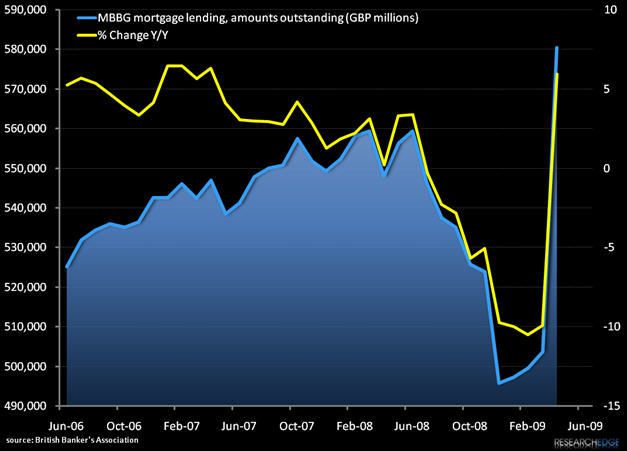

As such, the current low rate environment is having a significantly larger impact on the UK consumer than their US counterparts. National Statistics Office retail price Index levels reported today registered at -1.07% on a year-over-year basis but at +1.58% Y/Y with mortgage payments excluded from the basket (see chart below).

Clearly the impact of changing rates will be felt earlier and harder by consumers in the UK than in the US.

Andrew Barber

Director