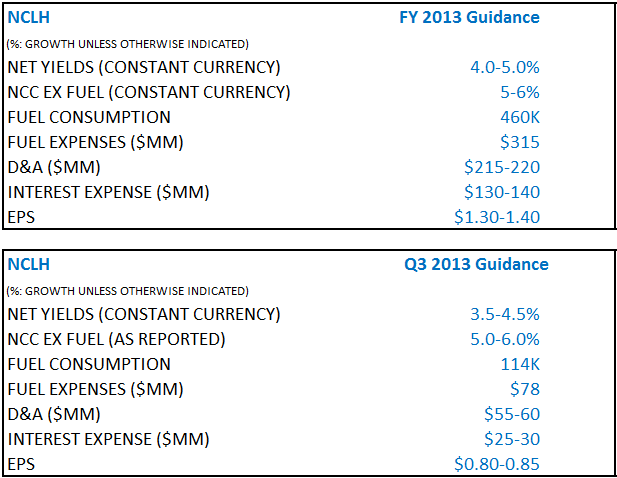

In preparation for NCLH's F3Q 2013 earnings release tomorrow, we’ve put together the recent pertinent forward looking company commentary.

GETAWAY

- Norwegian Getaway, is getting ready for her debut in Miami early next year.

3Q CAPACITY SCHEDULE

- Looking at deployment for the third quarter, our capacity in each itinerary is as follows. Our Europe program has 28% in the Mediterranean and 8% in the Baltic. We have approximately 20% each in Alaska and Bermuda, 13% in the Caribbean, 7% in Hawaii, and the balance made up of other itinerary.

PROMOTIONAL SPENDING

- I would say that we've had some promotional activities going on following that. And when I look at it right now, I would say that things in the last few weeks seem to have been a little bit better. And I think some of the noise as well is – some of the players may be doing a little bit more from a promotional standpoint to fill up their ships. Having said that, what I'm seeing now is that will play out over the remainder of this year.

ONBOARD REVENUE

- Onboard, we have a great quarter – some of it is Breakaway, some of it is just the continuing efforts we have. I would tell you that the remainder of the year is built into our forecasted guidance and yields...But it is a little lumpy.

EUROPE

- We've been able to bottom out in Europe market with yields and we're starting to see the ticket yields improving. But there are a few more Europeans on the ships than what has been the trend.

- On the margin, we're seeing a bit more of the Americans, but we're also seeing quite a few – and you look at the European economic situation, you're getting a little bit of a later booking from some of these countries. And we're all fighting for the same number of consumers. So in some cases, you're getting people that are spending a little bit less from the European side.

2014

- We're feeling pretty decent about what's going on for next year, although it's early. We're feeling pretty good about the booking patterns for 2014. First quarter, we're feeling very good about both on the load and the price.

SHARE REPURCHASE 2H 2014?

- My preference would probably be given where we are, it would probably to be in the stock repurchase program.