This note was originally published October 18, 2013 at 08:43 in Retail

EVENTS TO WATCH

VFC - Earnings Call: Monday 10/21 8:30 am

COMPANY NEWS

HBI - US: Hanesbrands to axe half of Maidenform's workforce

- "...Hanesbrands will lay off nearly half of Maidenform Brands' 1,330 staff worldwide as part of its US$583m merger with the rival intimate apparel maker."

- "...Maidenform's New Jersey corporate operations will be consolidated into Hanesbrands' headquarters in Winston-Salem and its Manhattan offices by the end of 2014."

- "Most of the 300 positions at Maidenform's headquarters will be phased out over the next year, but Hanesbrands said many of the sales, design and merchandising personnel will remain with the company."

Takeaway: I guess we know why they bought MFB -- for the brands, and nothing else. This synchs with our view that this deal will be far more accretive than the company guided towards.

UA - Under Armour challenges techies to develop future products

(http://www.bizjournals.com/baltimore/news/2013/10/16/under-armour-challenges-techies-to.html)

- "The sportswear maker will begin hosting innovation challenges twice a year — instead of annually — for entrepreneurs outside Under Armour...to suggest ideas for new innovations the company can incorporate in future product designs. Under Armour began holding the contests annually three years ago, and the results of the first challenge will hit the market in 2014."

- "The company is searching for developers who can help build on the technology in Armour39, Under Armour’s fitness tracking device that debuted in March. Finalists will present their concepts before Under Armour executives at a Future Show in April 2014."

Takeaway: Taking one right out of Nike's playbook -- again (as they should). Note that Nike held a major competition this summer for people to come up with new commercial product to elevate Nike's technological platform and marry with marketable product.

M - Macy’s strategy for Black Friday sales uncovered when ad leaked

- "Macy’s Inc. this week tried to titillate shoppers when it dangled a sample of what shoppers can expect when it opens stores at 8 p.m. for the first time ever on Thanksgiving day, but it seems its entire 49-page Black Friday deals ad now has been leaked, in perhaps the earliest ever such leak for a major retailer."

Takeaway: They make it sound like it was a leak…but sounds to me like it was intentional.

KER - Gucci Awarded $144.2M Against Online Counterfeiters

- "Gucci America Inc. on Wednesday was awarded $144.2 million in damages by a federal district court in Fort Lauderdale, Fla., against several organizations engaged in an online counterfeiting scheme."

- "The federal court also ordered the immediate surrender to Gucci of 155 domain names used in the counterfeiting operation."

Takeaway: The domain names are enforceable -- and therefore are history. But KER will never see a dime of the $144mm.

HIBB - Hibbett Sports Announces Transition Plan for Mickey Newsome

(http://www.sportsonesource.com/news/article_home.asp?Prod=1§ion=1&id=48398)

- "Hibbett Sports, Inc. announced that effective Feb. 2, 2014, Mickey Newsome will transition from his current position as executive chairman and employee of the company to non-executive chairman. The company also announced that Jeff Rosenthal, president and chief executive officer, has been appointed to the board of directors, effective immediately, thereby increasing the size of the board to ten members."

Takeaway: HIBB might be a tiny company, but Newsome is a major dominant force. Life without him will be a definite change for HIBB.

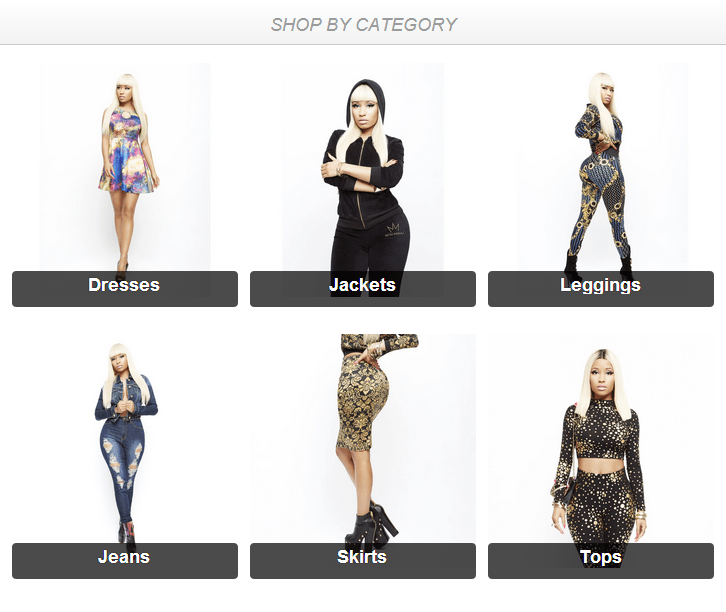

SHLD - Nicki Minaj Launches Fashion Line for Kmart

- "Minaj launched a new clothing line for Kmart and ShopYourWay.com. The Nicki Minaj Collection includes such items as color block skirts, bandage dresses, deconstructed jean jackets and galaxy print bomber jackets."

- "The new collection by Minaj...has items that range from $3.99 to $37.99."

Takeaway: Nicki is definitely an influencer, but does her fan base shop at K-Mart? This is a binary event for SHLD, but the upside potential is greater than the downside risk.

TOYS - No Joy in Toys 'R' Us Land

- "The problems have their roots in a $6.6 billion leveraged buyout in 2005 that piled on the debt and left it beholden to three investor groups—Bain Capital Partners LLC, KKR & Co. and Vornado Realty Trust —each with differing game plans."

- "The three had hoped to exit the investment with an IPO a few years ago, but they disagreed over exact timing, according to people familiar with the situation, and the window of opportunity has since closed because of the retailer's steady declines in profit."

- "Vornado in particular is ready to get out, according to people familiar with the matter. Vornado has written down the value of its holding by $118.5 million. But because the stake had appreciated before the write-downs a year or so ago, the investment is now worth $418 million, roughly what Vornado paid for it."

Takeaway: Interesting article showing the dynamics behind the ownership structure at TRU. Be careful who you partner up with when when buying something.

Bonmarché - Bonmarché prepares stock exchange flotation

(http://www.theguardian.com/business/2013/oct/18/bonmarche-stock-exchange-flotation-fashion-aim)

- "Bonmarché, the fashion chain aimed at women over 50, is preparing to float on the London stock exchange in November…"

- "The retailer, best known for its plus-size ranges, announced on Friday that it plans to sell shares on the Alternative Investment Market next month…"

- "As well as re-fitting some of its 264 shops, the group is now scouting for new locations and plans to open stores in garden centres, as part of a tie-up with the Garden Centre Group."

- "Since Sun European Partners took over, the company has earned £9.1m on an income measure that counts earnings before interest, tax, depreciation and amortisation."

Takeaway: Does Bonmarché really deserve to be public?

INDUSTRY NEWS

New Research Uncovers Which Email Promotions Generate the Most Revenue for Online Retailers

- "...we have released new research today that identifies the types of promotional offers that work best – and when they should be sent – to generate maximum revenue for online retailers. The data was derived from an analysis of 100 million online transactions, 20 million user profiles and 100 email campaigns."

Japan’s August Clothing Imports Up 21.4%

(https://www.sourcingjournalonline.com/japans-august-clothing-imports-21-4/)

- "Japan’s apparel imports for August were up in value by 21.4% over the same period last year, an increase to 280,732 million yen. "

- "By units Japanese apparel imports increased by 2.9% over the same period last year, hitting 371.059 tons, according to government data."

- "Japan’s apparel imports have increased by both value and volume for five consecutive months…"

Takeaway: The biggest import number we've ever seen out of Japan. Ever is a long time.

E-Commerce Trends in China: By the Numbers

- " E-commerce sales in Mainland China may be growing, but the actual order submission rate is still just 10 percent and apparel as a segment represents only 9 percent of online sales."

- "Apparel and accessories represent 80 percent of sales in China through Borderfree’s shopping service. The service allows consumers to buy at an international brand’s site, but with the Borderfree interface that automatically does currency conversions and is in the language of the country where the consumer is located…"

- "Shirts and tops rank first, followed by dresses, shoes, outerwear, pants and handbags in top categories for sales year-to-date, but when calculated by units sold, more shirts and tops were sold than any other category, followed by dresses, pants, shoes, outerwear and then handbags."

- "The top brands sold online occupy the luxury space, such as Gucci, Michael Kors, Tory Burch, Giorgio Armani, Kate Spade, Marc Jacobs, Prada and Stella McCartney."

- "By demographic, 63 percent of shoppers are male, with the average age range for those who did the most shopping online between 18 and 30 and an income range of between 1,000 and 3,000 yuan a month, or $163.16 to $489.48 at current exchange."