With the DC drama sideshow shelved for a few months, confused monetary policy positioning out of the Fed can again return as the attendant driver of investor angst. Alongside the market re-shift in focus today, the dollar is down, rates are down, and stocks are struggling to mount a reversal of early weakness

Essentially, we are back to where we were about a week and a half ago with both the dollar & the 10Y testing their breakdown lines. Keith will be home from London and back in the PM seat tomorrow, but the levels that matter are still:

- DXY ($USD): TAIL Support = 79.21

- 10Y Treasury: TREND Support = 2.58%

We are currently running fairly low gross exposure with 6 longs, 3 shorts. From here, we need to see the $USD and 10Y Treasury support lines hold alongside some fundamental confirmation with next week’s data deluge to take our gross & net exposure to domestic equities higher again. Conversely, if the dollar and 10Y breakdown alongside marginal weakness in the macro data and an overbought signal in equities, we’ll continue to tighten up/reverse our positioning.

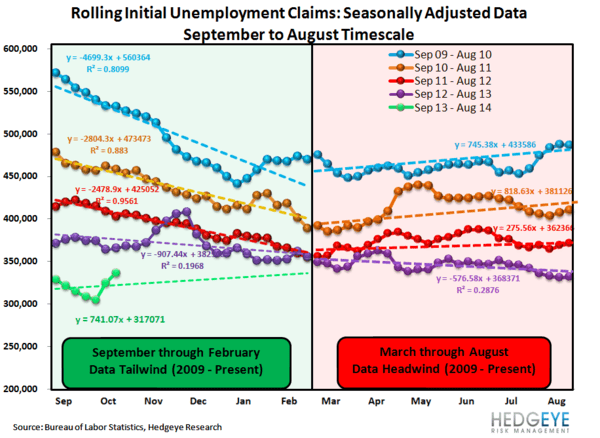

Meanwhile, on the labor front, the ongoing distortion in the only currently available government data series – Initial Jobless Claims - continues to perpetuate uncertainty around both the underlying strength of the domestic labor market and the read through to probable, forward monetary policy adjustments.

We work through this weeks claims numbers in detail below, but the bottom line is that, after adjusting for the impacts of the government shutdown and California catch-up, the Labor Market’s trend line of improvement remains intact.

Below is the detailed breakdown of this morning's claims data from the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

- Hedgeye Macro

--------------------------------------------------------------------------------------------------------

Lots of Needed Adjustments

The Golden State has been the source of considerable and ongoing distortion in the only currently-available government labor market data series, initial jobless claims. We thought that last week's sharp spike in claims reflected the full catch-up of California's temporary IT systems-related issues, but that was wrong. This morning's number is again distorted by California's ongoing catch-up. While we received data last week indicating that there were 33k additional claims from California due to the backlog catch-up, this week we received no such number. Comments in the media, however, have alluded to the impact being of comparable size.

In the first chart below we look at the distortion being created with California and then in the second chart we examine the impact this is having on the national data. The first chart shows weekly NSA initial claims for CA through 10/4. Unfortunately, state level data is only available on a 1-week lag. The blue line shows 2013 while the red line shows the corresponding period in 2012. It's clear that the IT system effect occurred the week of Sep 6, when the spread between 2012 and 2013 jumped to -25k claims. The following week it remained wide at -21k. In the most recent week the spread reversed to +26k. However, it's the cumulative size of the distortion that now needs to be reversed. As such, we would expect next week's number to again be overstated. Thereafter, we would expect to see the series revert back to normal.

Separate from California's distortive effects, there is also the effect of the govt shutdown. While Federal employees file under a separate system (~70k of them filed the week of Oct 4), there are private workers who were laid off because they work in govt-related fields. These people were reported to have accounted for 15k additional claims in the week of Oct. 4. This past week no such similar disclosure was provided, but we did see reference from Reuters quoting a labor dept analyst saying "There had not been a perceptible increase in filings last week from non-federal workers furloughed because of the just-ended government shutdown."

The bottom line is that when making the adjustments for both California and the temporary distortions from the govt shutdown, the labor market's trend line rate of improvement remains intact.

Nuts & Bolts

Prior to revision, initial jobless claims fell 16k to 358k from 374k WoW, as the prior week's number was revised down by -1k to 373k. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 12k WoW to 336.75k.

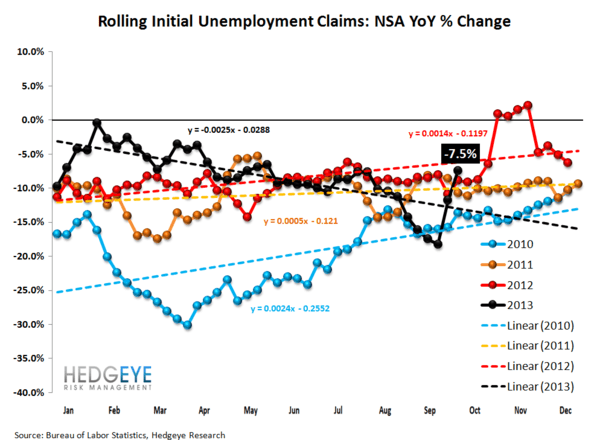

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.5% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -11.8%, but again this is an unadjusted number.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT