We contend that buying DRI today represents a generational opportunity in the Restaurant space, as the stock is currently trading at a significant discount to its underlying asset value. In our view, there remains the potential for tremendous upside if the core company can improve its operational execution.

We understand that DRI is different from the companies below, but the point we are trying to make is that they have all been in similar situations, and have once felt the pressure, that DRI is feeling today. We believe part of the upside in DRI is significant, but unquantifiable and could be realized if management is ousted (or they adopt our operating beliefs), and the company returns to a more streamlined operating structure.

In our opinion, Darden needs a forward-thinking, seasoned restaurant operator, with public company experience, to deliver an effective turnaround plan that is focuses on restoring Olive Garden profitability. In this regard, the current Chairman and CEO, Clarence Otis, has proven his incompetence. His lack of restaurant operating experience is a major reason the current management team has been decidedly unsuccessful.

The plan of action for DRI should be comprehensive, clear, and must offer a compelling solution that would help Darden, and specifically the Olive Garden, regain its stature as one of the premier casual dining chains in the business.

The most important pillar for the new Darden, is the formation of a closely aligned and well-functioning team of qualified, talented, experienced, and motivated personnel, that would come together to execute on the following business philosophy:

- Superior financial results come from inspired, principled leadership

- A clear, focused vision

- A consumer-driven culture

- Innovation

- Measurable operational excellence

- Distinctive brand consistency

- Appropriate cost controls

Darden’s current business plan has done nothing but destroy shareholder value over the past five years. Our recent Black Book, “Dismantling Darden”, describes, in detail, why DRI is having such a difficult time.

The company finds itself in an eerily similar position as MCD, SBUX, and EAT, not too long ago, when these companies tried appealing to the masses and began growing units too fast. Not surprisingly, the road to recovery for each company was essentially the same, barring some obvious nuances.

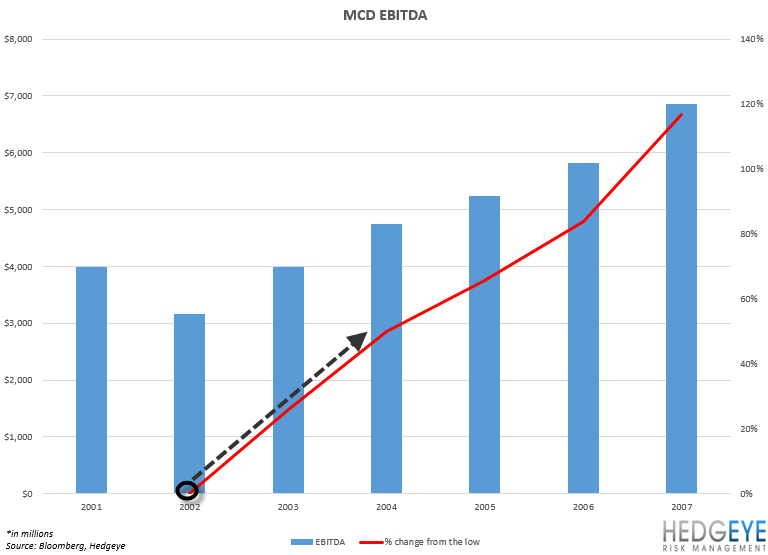

McDonald’s (2002-2007): MCD formulated the “Plan to Win” in 2002, which later became a template for success at Brinker.

- MCD cut capital spending from $2.0 billion in FY02 to $1.3 billion in FY03

- EBITDA bottomed at $3.2 billion in 2002 and increased 117% over the next five years

- The stock bottomed in March 2003 at $12 and rose to $57 by the end of 2007

Starbucks (2007-2012): With Schultz back at the helm, SBUX focused on attacking the middle of the P&L and improving the guest experience.

- SBUX cut capital spending from $985 million in FY08 to $446 million in FY09

- EBITDA bottomed at $1.3 billion in 2008 and increased 88% over the next four years

- By 2QFY09 (June) the fundamentals had improved; the stock was traded at $14 and rose to $78 five years later

Brinker (2008-2013): Facing an industry in the midst of a secular decline, senior management formulated a “Plan to Win”, which entailed attacking the middle of the P&L and driving traffic.

- EAT cut capital spending from $431 million in FY07 to $273 million in FY08; the company further reduced capital spending to $88 million in FY09

- EBITDA bottomed at $248 million in 2009 and increased 64% over the next four years

- By 2QFY09 (January) the fundamentals had improved; the stock traded at $10 and rose to $40 five years later

We don’t know exactly where DRI will shake out in the process, but we do know the company finds itself in a hole that MCD, SBUX, and EAT all managed to climb their way out of.

Howard Penney

Managing Director