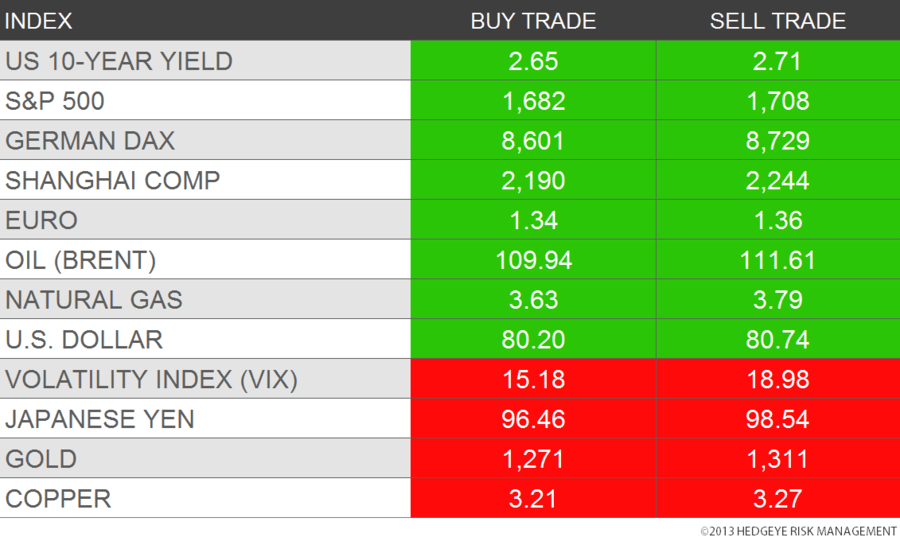

Editor's note: Here is a complimentary look at Hedgeye's Daily Trading Ranges product for 10/11. These are CEO Keith McCullough's proprietary buy and sell levels on major markets, commodities and currencies. To learn more and to sign up, click here.

Editor's note: Here is a complimentary look at Hedgeye's Daily Trading Ranges product for 10/11. These are CEO Keith McCullough's proprietary buy and sell levels on major markets, commodities and currencies. To learn more and to sign up, click here.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.