Not So Fast

We've been singing the praises of the initial jobless claims data for a while now, particularly as it showed noted divergence vs some of the other labor market data series. This morning we found out that at least a portion of the recent strength (since the start of September) was attributable to shenanigans in California new software for processing claims. For the last 4 weeks, since roughly the start of September, California has had a backlog of claims due to difficulties arising from their new software system. This past week, they finally got the bugs out of it and caught up. The effect was an increase of ~33k SA jobless claims. Total SA claims rose by 66k this week, and half that was attributable to CA, said a Labor Dept spokesperson. Beyond this, there was a further 15k increase this week from defense companies laying people off temporarily due to the government shutdown.

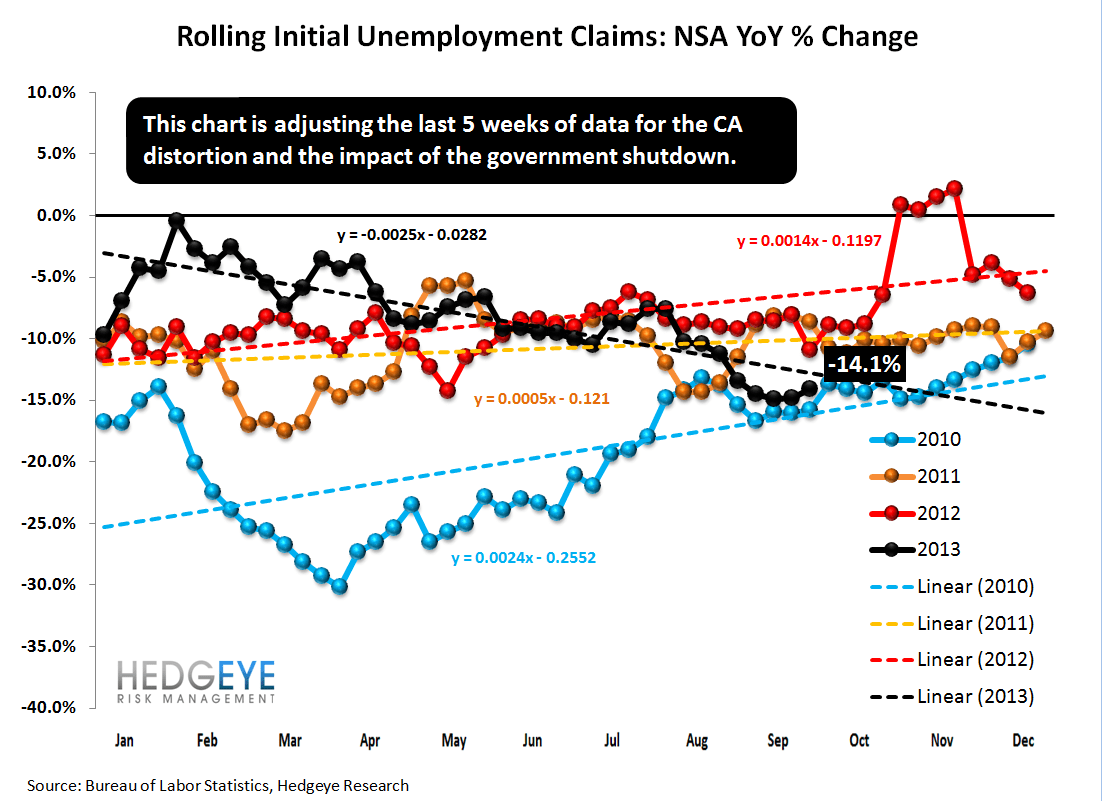

What we've done in the chart below is reconstruct the last five weeks of data to reflect CA's issues and the 15k temp layoffs from defense. The takeaway is that the trend is intact. Rolling NSA claims, adjusted for these issues, was lower by 14.1% in the latest week, which is almost right in line with the trendline since the start of the year, and only nominally weaker than the best print we've seen YTD of -14.9% 3 weeks ago.

The bottom line is that this morning's data looks terrible, but the underlying trends in the labor market remain exceptionally strong. We would reiterate our bullish stance on being levered to the ongoing jobs recovery. This morning we flagged Capital One (COF) in a note as being a great way to play this theme.

Nuts & Bolts

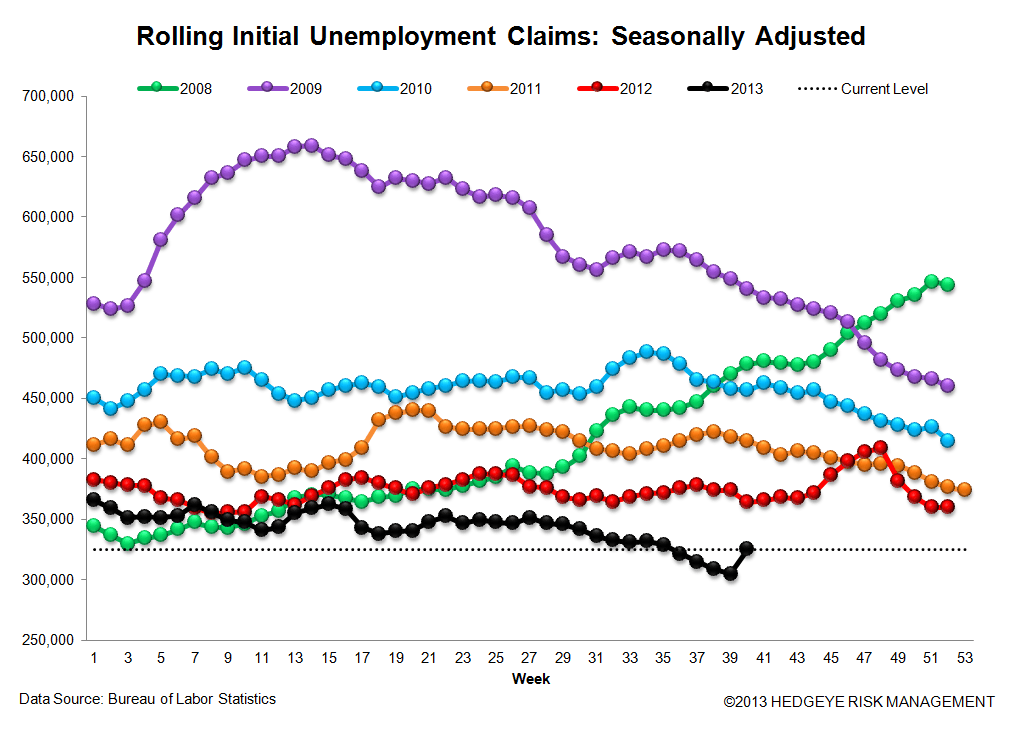

As there was no revision to the prior week's data, SA initial jobless claims rose 66k to 374k from 308k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 20k WoW to 325k.

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -11.7% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -18.2%, but this reflects the impact of the CA distortion.

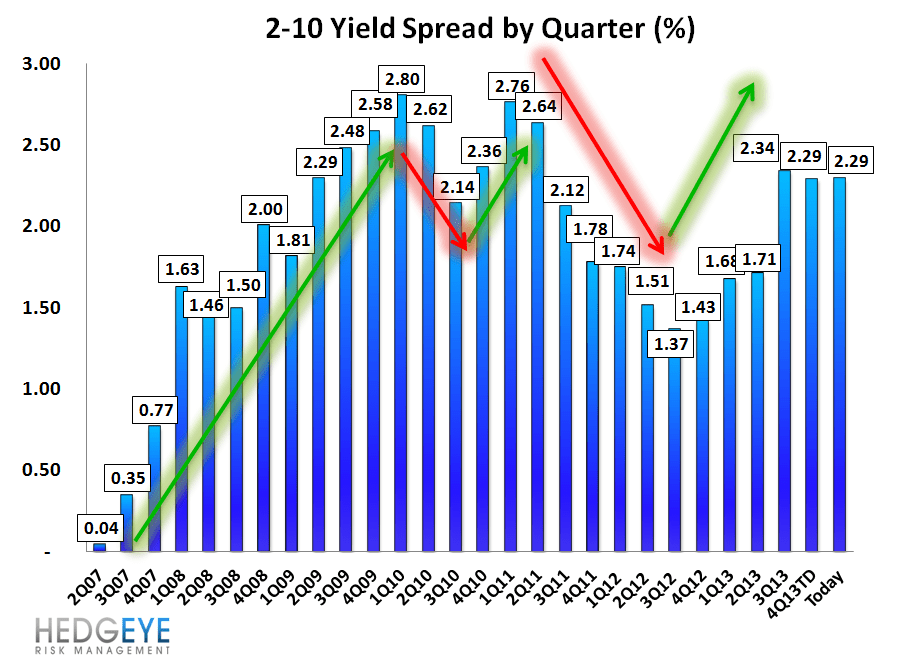

Yield Spreads

The 2-10 yield spread was unchanged at 229 bps in the past week. The third quarter average yield spread was 234 bps, a 63 bps increase vs the 2Q average of 171 bps. While the curve has come under some pressure of late with tapering speculation waning, the bottom line is that thus far 4Q is running at an average spread of 2.29%, or just 5 bps lower than the average for the third quarter. This 3Q lift will help alleviate some of the pressure on bank NIMs, but what it will really take ultimately will be the Fed lifting the short end of the curve.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT