Summary: The Labor market strength remains ongoing as claims make another YTD and multi-year low. ISM Services declined sequentially with all components losing MoM. Seasonality has shifted to a data tailwind while policy (manifest in Down Dollar & Down Rates) has shifted from benign to discrete growth headwind.

One down datapoint (ISM Non-mfg) does not a trend make, but all trends start as trades - and the probability for a negative macro Trade to evolve into a Trend breakdown in growth heightens considerably when the principal, causal factor in our model (policy) inflects negatively.

Keep the $USD front in center here as it moves towards testing its TAIL line of support at $79.21

INITIAL CLAIMS: STILL IMPRESSIVE

The ongoing strength in the domestic labor market remains impressive. Inclusive of this morning’s release, the 4-week rolling average of non-seasonally adjusted Initial claims, our favored read on underlying labor trends, registered its strongest rate of improvement since July of 2010. To quickly review the data:

NSA Claims: Non-seasonally adjusted claims printed 252K, down 3K WoW while coming in < 300K for the 10th consecutive week. The 4-week rolling average was -18.3% lower YoY, which is a sequential improvement versus the previous week's YoY change of -17.5%

SA Claims: Headline, seasonally-adjusted initial jobless claims fell -1K to 308K vs the prior week (revised) 307K. The 4-week rolling average fell -4K WoW to 304.75K – the lowest level since May of 2007.

As a reminder, in additional to the prevailing organic strength in the claims data, the series will see a building seasonal tailwind over the September to February time period. Separately, it’s worth noting that federal workers are eligible to collect unemployment while furloughed, so that may introduce an upward (albeit transient) bias in next week’s claims data and any subsequent releases so long as the shutdown remain in effect.

ISM: Sequential Softening

The ISM Non-Manufacturing Composite Index declined -4.2 to 54.4 in September with all principal components declining sequentially. Business Activity (-7.1) and Employment (-4.3) led component declines and while Export Orders (+7.0) and Prices (+3.8) were the lone gainers.

The Trend (trailing 3M/6M/12M) across the balance of sub-components remains positive at present and, notably, New Orders was down just -0.90 to 59.6 – only a modest decline in the context of last month’s ( and the cumulative 2-month) material advance and still a solid absolute reading.

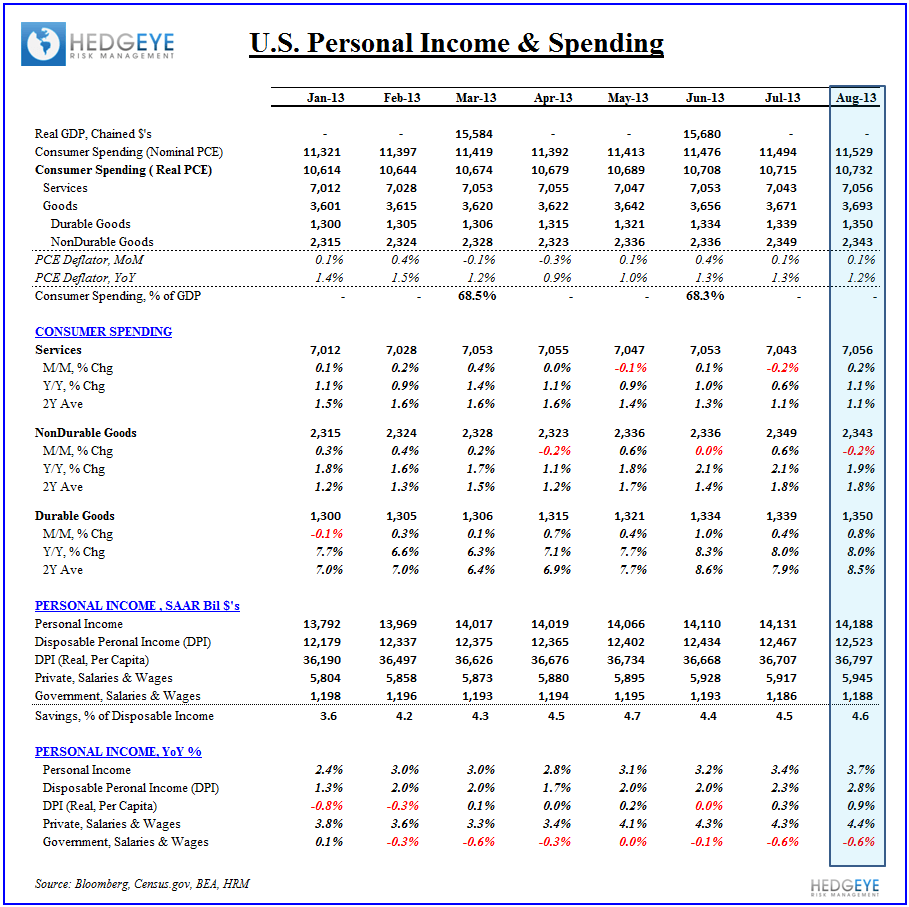

On the consumer side, the recent multi-month trend has been one of improving consumption of Goods while spending growth on Services has been flat to decelerating on both a YoY and 2Y average growth basis (2nd Table below). Coupled with the fiscal policy constraints to an acceleration in disposable income growth over the near-term, today’s ISM data presages another middling growth number for Consumer Spending on Services with the September release.

One marginal negative datapoint does not a trend make, but all trends start as trades - and the probability for a negative macro Trade to evolve into a Trend breakdown in growth heightens considerably when the principal, causal factor in our model (policy) inflects negatively.

Keep the $USD front in center here as it test its TAIL line of support at $79.21.

Christian B. Drake

Senior Analyst