Potbelly is on deck for an IPO tomorrow. The company plans to sell 7.5 million shares and recently raised the expected price of its IPO to $12 to $13 per share.

In this note, we offer up our take on the latest IPO in the restaurant space. It is important to note, however, that we did not have the opportunity to meet with management nor did we attend any of the company’s road show presentations.

With that said, we believe Potbelly will be the beneficiary of a recently hot market for growth related restaurant stocks. The offering size is rather small at slightly over $95 million and demand should be high. A number of veteran restaurant analysts will be comfortable with the CEO, Alwin Lewis, who is a familiar name in the industry. Lewis spent 13 years at YUM, including a stint as COO, before leaving in 2004 to become the CEO of Sears.

Potbelly should do fine initially, but it could be on a short leash. It is a premium player in a very crowded, highly competitive sandwich (sub) market. Regarding the latter point, all of the company’s direct competitors, including, but not limited to, Subway, Jimmy John’s, Firehouse Subs and Jersey Mike’s, are private companies, which makes direct comparisons difficult to come by.

Its important to note that IPOs, particularly those from companies with strong growth stories, have fared extremely well lately. NDLS, for example, gained +104% on its first day of trading. But, investors expecting another Noodles-like performance should heed caution, as we believe this was more of an aberration than the norm. In fact, despite their similarities as fast casual operators, the two have stark contrasts. Potbelly competes in a crowded segment of the industry as opposed to Noodles, which brought more of an innovative, fresh concept to the table. In addition to competing in a less-crowded Asian segment, we would argue that NDLS is also perceived to be healthier than PBPB.

All told, Potbelly does have compelling unit economics and plenty of room to grow. The company currently has a domestic base of 286 locations in 18 states and the District of Columbia. However, the units are incredibly concentrated, as over 50% of its units are located in Illinois, Texas and the District of Columbia. Furthermore, the company has little presence outside the Midwest and Northeast. Recent expansion efforts have been strong, as management opened 21 and 31 company-operated shops in 2011 and 2012, respectively, and plan to open an additional 32-35 company-operated shops in 2013. At this time, the company does very little franchising.

The unit growth story will have to save the day, as the trajectory of same-store sales is below average for a chain this size. The company’s same-store sales grew +1.5% in 1H13, but traffic declined by -1.1%. It appears the segment is having a difficult time amid increased competition from peers and convenience stores. Subway recently saw sales decline -2% this past summer – its first decline in recent memory.

Portelly construction costs range from $450,000 to $770,000 per store and new stores are averaging about $1.1 million in sales per year, which is quite strong for a "sub" chain. Management currently targets shop sizes between 1,800 and 2,200 square feet and dining areas that typically seat between 50 to 60 people.

As it stands, we have several positive and negative takeaways from our analysis.

Positives

- Fits the current “growth” style investing theme

- Compelling unit economics

- Strong brand presence in its communities

Negatives

- It will be difficult to expand the day-part mix

- Traffic trends have been weak lately

- Two states and the District of Columbia account for 53% of company-owned units

Below, we examine how PBPB’s margins stack up against some of its publicly traded peers.

Average Unit Volumes

Average unit volumes are below the publicly traded peer group, but are strong relative to other sub chains. While there is certainly room for improvement, day-part expansion will be difficult to achieve.

Cost of Sales

Food costs are in line with the peer group. Higher food costs suggest that the company is focused on selling a better product than the average QSR chain. If food costs begin to head lower over time, this could be a bad sign. In our view, a decrease in food costs would be a leading indicator of negative traffic.

Labor Cost

We’re not close enough to the company to know what they can do to bring labor costs down from here. As for the company’s peers, we believe PNRA’s labor costs are headed higher and view CMG as the model of efficiency in the restaurant industry. PBPB’s labor costs falling between the two suggests that they are not excessive and there still may be room to the downside.

Restaurant Level Margins

Potbelly’s restaurant level margins are very strong. That said, it is hard to tell if there is significant room for improvement without leverage from higher AUVs.

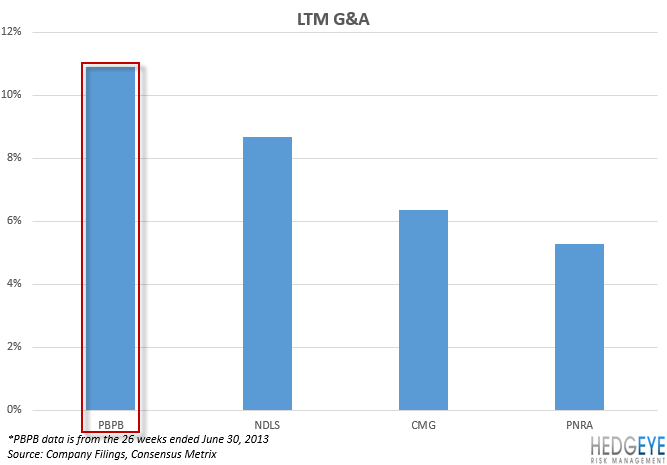

G&A

PBPB is currently investing for future growth and, we believe, this is where the majority of the leverage is in Potbelly’s business model. The company must successfully execute on its unit opening strategy in order to eventually leverage its G&A costs.

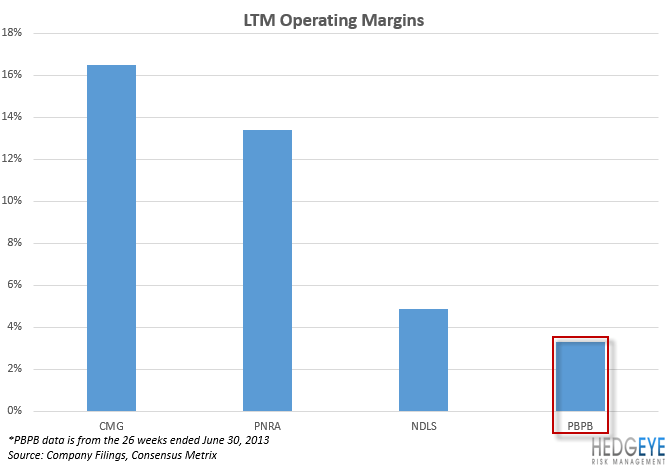

EBITDA & Operating Margins

We believe there is significant room for improvement in operating margins. Given current restaurant level margins, most improvement in EBITDA & operating margins is likely to come from management leveraging its G&A.

Howard Penney

Managing Director