“The great thing in the world is not so much where we stand, as in what direction we are moving.”

-Oliver Wendell Holmes

Yesterday was one of the most humbling days of my professional life. It was Moving Day @Hedgeye. It was our first full day working as a team in our new Stamford, CT studio office space. We had all hands on deck.

I say studio because that’s what we are building – the next evolution of independent research coming out of our firm will include more simplifying communication tools like visualization and video-streaming. As Albert Einstein said about ideas, “if you can’t explain it simply, you don’t understand it well enough.” More on that as we move forward.

On the humbling part, externally at least, that’s not the first word that tends to come to mind beside my name. I don’t care about that as much as how my teammates and I feel when we are grinding it out together. Alongside my two beautiful children, I’ve never been so proud to see my family and firm move forward so selflessly. Thank you, to all of you, who have been a part of it.

Back to the Global Macro Grind…

Selfless, objective, flexible – these aren’t the words you’d use to describe the US government this morning. That means we have to overcompensate for their lack of resolve and prepare for whatever direction they try to take our said free-markets next.

Yesterday was a fascinating day on that score because, after the media monetized all the ad sales associated with “shut-down” drama, markets actually traded on the economic data. As Christian Drake pointed out to me just after 11AM EST on our desk, it’s #OctTaper versus Bernanke.

Put another way, it’s economic gravity (the data) vs. he who promises to bend it (Bernanke). And it’s not just the US stock market that is handicapping this battle of data versus un-elected opinion in real-time. Immediately after the USA posted another “surprisingly” bullish US #GrowthAccelerating ISM report for September (56.2 vs 55.7 in AUG), this is what happened:

- Gold got tapered

- Oil got tapered

- Bonds got tapered

This was kind of cool (for us) because we haven’t liked the Gold Bond thing for all of 2013 (we still have 0% asset allocations to both Fixed Income and Commodities; both are down YTD).

But it was also cool for the one thing that consensus missed alongside US #GrowthAccelerating for the past 10 months which is, of course, growth expectations embedded in the US stock market.

That’s right anti-Bernanke-policy-to-try-to-bend-gravity-fans:

- US Dollar Stabilizing

- And #RatesRising

- = all-time highs in US growth expectations (growth stocks)

As The Champ used to say “Pardon?”

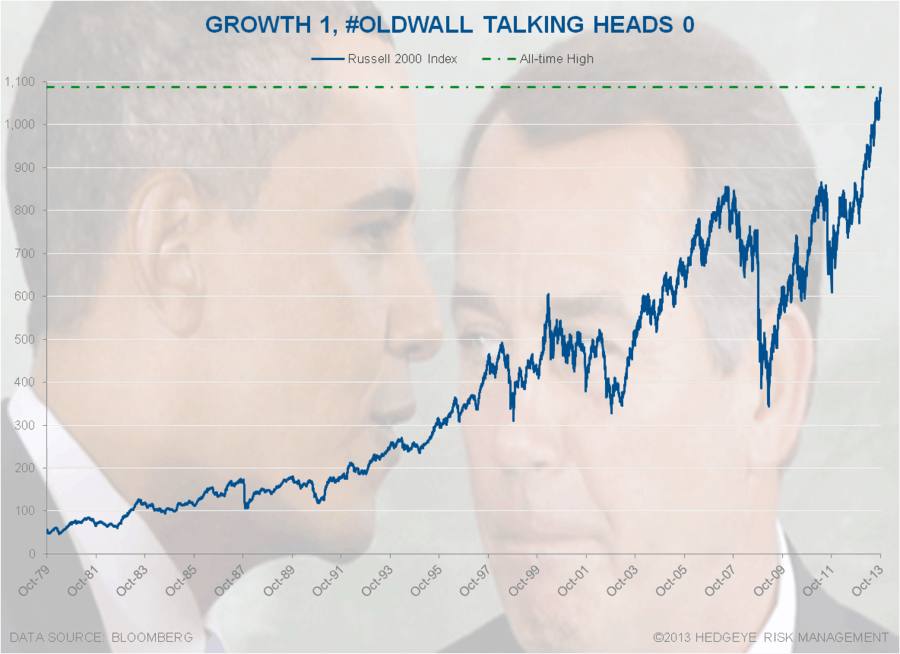

Indeed, Sir Champ. All-time is a long time, bro – and the proxy for US growth stocks (the Russell 2000) closed at an all-time high yesterday of 1087. That’s +28.0% for 2013 YTD!

Yes, I’m sure whatever partisan #OldMedia channel you were watching nailed that.

I’m sure every fear-mongering and end #EOW (end of the world) idle threat thrown at The Rest of Us by the #PoliticalClass was a risk managed one based on selfless, objective, and flexible analysis too. Up next on cable, “the sun no longer rises in the East.”

Where to from here?

As I wrote in yesterday’s rant, I have no idea. I’m just saying that it was nice to see Mr. Market rub it in Washington’s nose for a few more hours. Today is simply another day to embrace the uncertainty and volatility of it all.

Key intermediate and long-term (TREND and TAIL lines) to keep front and center into Friday’s jobs report:

- CURRENCY: US Dollar Index long-term TAIL support = $79.21

- BONDS: US 10yr Treasury Yield intermediate-term TREND support = 2.55%

- STOCKS: US Stock Market (SP500) TREND support = 1660

To be clear, while US #GrowthAccelerating has been the surprise of 2013, A) that’s now old news and B) the slope of US growth’s line can go anywhere from here.

That’s what Big Government Intervention does – it shortens economic cycles, and amplifies market volatility. There’s a deep simplicity in understanding that too. So keep moving out there.

Our immediate-term Risk Ranges are now as follows (we have 12 Macro ranges in our Daily Trading Range product):

UST 10yr Yield 2.58-2.68%

SPX 1

VIX 14.71-16.69

USD 80.02-80.75

Yen 97.04-98.76

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer