“Get comfortable with being uncomfortable.”

-Jillian Michaels

That’s a varsity quote from one of the original trainers on NBC’s “The Biggest Loser.” To a degree, Jillian Michaels typifies the attitude of my generation of entrepreneurs in America. She’s a 39 year old self-made business woman. She didn’t get anything handed to her in life. She bartended her way through college, sucked it up, and lived the American dream.

What is the American dream? Is it a bunch of big political and media losers getting paid to perpetuate fear and crisis on cable TV? Or is it the polar opposite of that? Bernanke, Boehner, and Obama can’t shut us down. No, no, no ladies and gentlemen. Today we are going to do what we do at the top of every risk management morning – we are going to grind.

Grinding in the arena of business life has been celebrated by this country for generations. In 1925, President Calvin Coolidge reminded the American Society of Newspaper Editors that “the chief business of the American people is business” (The History of Money, pg 169). So that’s the headline coming out of this 2.0 Financial Media upstart from Stamford, CT this morning. Rise Above that.

Back to the Global Macro Grind…

What’s fascinating about watching both the US stock market futures and the bond market this morning is that neither of them seem to care whatsoever about Old Media’s politicized fear-mongering. Mr. Market is shutting the media’s message down.

That shouldn’t surprise you. As newspaper editors and television producers look backward, markets look forward. Up next is the US Employment Report for the month of September.

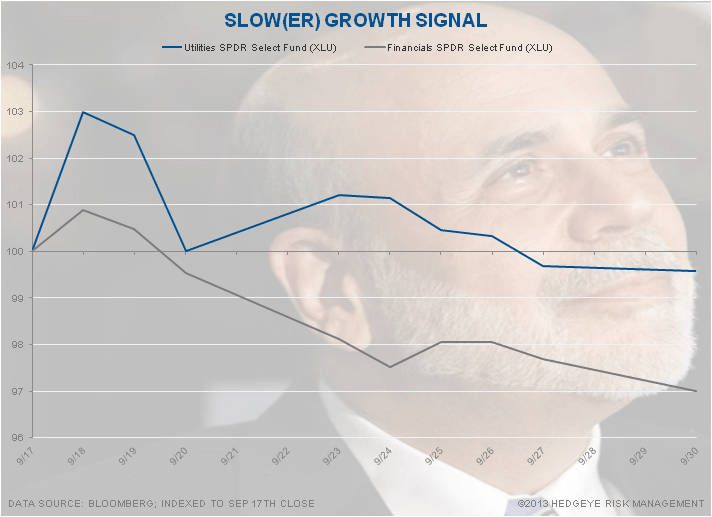

September (and the 3rd quarter in general) was one of the best quarters for US growth expectations in half a decade:

- US Growth Stocks hit all-time highs (for SEP Industrials (XLI) +5.4% and Consumer Discretionary (XLY) +5.1%)

- US (slow growth) Bonds and Utility stocks hit their YTD lows (for SEP Utilities (XLU) only +0.18%)

- US Equity Volatility (VIX) hit YTD lows as well

Then, mid-September, along came Bernanke, Boehner, and Obama …. and:

- US Growth Stocks started making a series of lower highs (down for 7 of the last 8 days)

- US (slow growth) Bonds and Utilities outperformed everything growth

- US Equity Volatility (VIX) ripped a +26% move to the upside in less than 2 weeks

Congrats to the Fed, Democrat, and Republican parties. It’s a tie – you all get a Hedgeye sticker for America’s biggest losers!

Looking forward to the US employment report on Friday:

- US Growth Stocks may very well put in yet another higher-low (SP500 = 1660 TREND support)

- US Treasuries appear to be making another lower-high (10yr Yield = 2.55% TREND support)

- And front-month fear (VIX) is making yet another lower-YTD-high as well (VIX = 18.98 TREND resistance)

What say you Mr. Market about all of that?

I say it’s government versus gravity!

That would be economic gravity of course. As in the stuff that Bernanke has been trying to bend. And while bending gravity appears to be quite innovative to the Central-Market-Planner-in-Chief-of-anti-dog-eat-dog USA, that doesn’t mean it’s going to work.

So play this out – the US jobs report on Friday has a binary outcome:

- It’s a moon-shot to the upside and bond yields rip (again) to the upside

- It’s in line to a “miss” and Bernanke and his old-boys from anti-gravity-smoothing headquarters say “we nailed it”

Which of the two will it be?

I’m proud to say that I have absolutely no idea. That’s why the Hedgeye Asset Allocation Model has a 50% Cash position and in our #RealTimeAlerts I only have 5 LONGS, and 4 SHORTS. Getting out of the way of this political gong show was a risk managed decision.

I’m very comfortable grinding out another business building day. I’m uncomfortable with risking what’s been a great year for us on a government report that could go either way.

UST 10yr Yield 2.59-2.68%

SPX 1

Nikkei 142

VIX 14.64-16.99

USD 80.02-80.77

Brent 107.08-108.98

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer