EVENTS TO WATCH OVER THE NEXT 24 HOURS

NKE - Earnings Call: Thursday 9/26 5:00 pm

FINL - Earnings Call: Friday 9/27 8:30 am

Takeaway: We’re looking for a modest beat out of Nike this evening -- $0.82 vs the Street at $0.78. While this is positive, we’re not expecting one of those ‘beat by a 25%’ quarters out of Nike. That, plus the fact that it has performed so strongly since being added to the Dow, makes us think that this quarter won’t be a major catalyst for the stock. Fortunately, it is hosting its analyst meeting at it’s WHQ in 2-weeks, which should give investors a lot more to sink their teeth in to.

ECONOMIC/INDUSTRY DATA

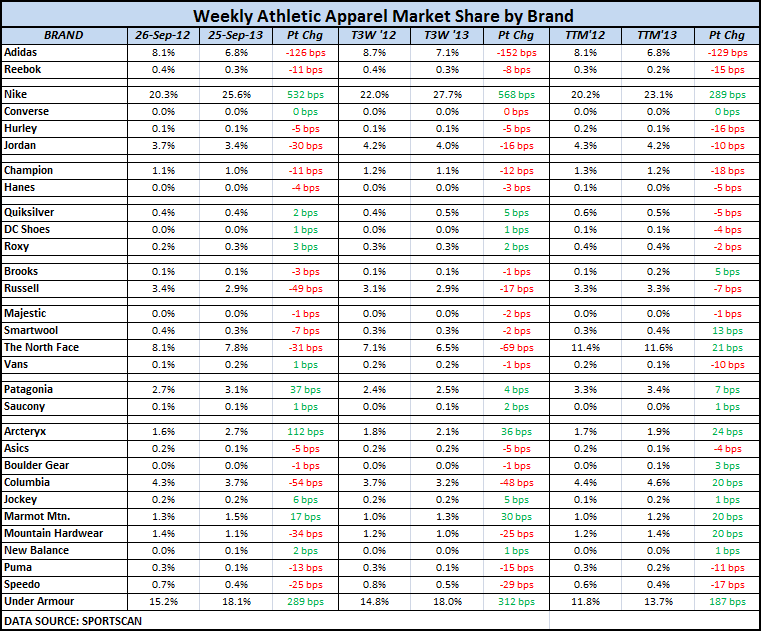

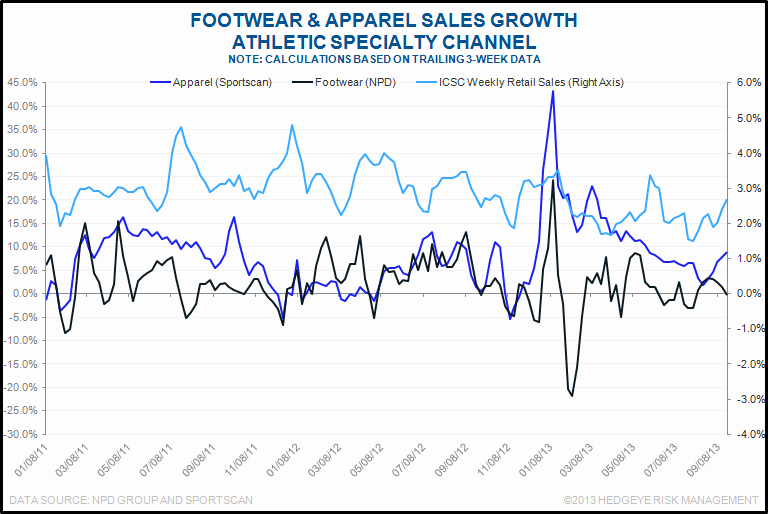

Takeaway: Athletic apparel sales continue to be extremely robust, which is particularly noteworthy because a) retail in general has been so slow, and b) there’s been a marked slowdown in Athletic footwear. The strongest and most consistent brands continue to be Nike and UnderArmour.

UK Survey Shows Strong Growth in Sporting Goods Sales in September

(http://www.sportsonesource.com/news/article_home.asp?Prod=1§ion=5&id=48105)

- "More than 65 percent of the United Kingdom's recreational goods retailers said sales grew in September, while none reported sales declines, according to the Confederation of British Industry’s (CBI) latest monthly Distributive Trades Survey of 111 retail and wholesale firms."

- "The survey indicated overall U.K. retail sales in September grew at their fastest pace since June 2012, and exceeded already solid expectations. September marked the third consecutive month of growth retail sales growth in the U.K. with growth reported across a number of sectors. CBI saiid the survey indicates retailers and wholesalers expect retail sales to grow robustly again in October."

- Key findings of the survey include:

- 46 percent of respondents reported that sales volumes were up on a year ago, while 12 percent said they were down, giving a balance of +34 percent - the strongest since June 2012 (+42 percent) and exceeding expectations (+26 percent)

- Retailers expect sales volumes to grow at a similarly strong pace next month (+31 percent)

- 52 percent of department stores said business volumes were up, while 0 percent said they were down, giving a balance of +52 percent

- Overall, 22 percent of retailers said that sales volumes were above average for the time of year, while 10 percent said they were below average, giving a balance of +12 percent - the highest survey balance since December 2010 (+18 percent)

- 36 percent placed more orders with suppliers than they did a year ago and 22 percent placed fewer, with the resulting balance of +14 percent.

Takeaway: We’d already gotten a sense about these trends through Foot Locker, and then Sports Direct. But this definitely confirms the fact that things are getting better in the UK.

COMPANY NEWS

JCP - Penney leaning toward $1 billion equity raise

- "[JCP] is looking to raise as much $750 million to $1 billion in new equity to build up its cash reserves as the holiday season approaches, according to three people with knowledge of the matter."

Takeaway: What’s odd is that it already has about another $1bn in assets it can access/liquidate before having to issue equity. Regardless, there are two reasons people are short JCP. 1) Because they think it is a zero. Or 2) Because they think a deal is coming. Once the cash is in hand, the ‘zero’ call is tough to make – at least near-term (especially with the company’s announcement today that it is comping positively). In addition, with liquidity not an issue, the pool of candidates it can tap for the CEO role grows significantly.

JCP - Report: J.C. Penney will hire 35K holiday workers

(http://www.chainstoreage.com/article/report-jc-penney-will-hire-35k-holiday-workers)

- "J.C. Penney Co., Inc. will reportedly hire about 35,000 seasonal workers for the upcoming holiday season. "

- "J.C. Penney also hired about 35,000 seasonal employees during the 2011 holiday season. The retailer did not release holiday hiring figures last year."

Takeaway: Doesn’t look like a bankrupt retailer to me.

JCP - J.C. Penney Looks to Unwind Martha Stewart Pact

(http://online.wsj.com/article/SB10001424052702303796404579097424086074190.html)

- "[JCP] is trying to find an amicable way to unwind a merchandising agreement with [MSO] that has been the subject of a court battle with Macy's Inc., people familiar with the matter said."

- "A ruling in the case by Justice Jeffrey Oing of the New York State Supreme Court was expected this fall. In a hearing Wednesday, Judge Oing said he planned to issue a decision 'hopefully in a shorter time, rather than a later time.'"

- "The companies have had discussions about modifying the relationship, the people familiar with the matter said. Under one scenario, Penney would exit categories in which it has a direct conflict with Macy's, including bedding, bath and housewares, which can't carry the Martha Stewart brand, one person familiar with the situation said. Another person cautioned that no deal was imminent."

- Martha Stewart spokeswoman Claudia Shaum said Wednesday, 'J.C. Penney remains one of our many retail partners. Our agreement with them is in force, and we have no intention of ending it.'"

Takeaway: If JC Penney wants to ditch Martha, she’s history.

WMT - Wal-Mart Cutting Orders as Unsold Merchandise Piles Up

(http://www.bloomberg.com/news/2013-09-25/wal-mart-cutting-orders-as-unsold-merchandise-piles-up.html)

- "[WMT] is cutting orders it places with suppliers this quarter and next to address rising inventory the company flagged in last month’s earnings report. Last week, an ordering manager at the company’s Bentonville, Arkansas, headquarters described the pullback in an e-mail to a supplier, who said others got similar messages. 'We are looking at reducing inventory for Q3 and Q4,' said the Sept. 17 e-mail, which was reviewed by Bloomberg News."

- "Walmart spokesman David Tovar said, 'We are managing our inventory appropriately. We feel good about our inventory position.'" "The order pullback isn’t 'across the board' and is happening 'category by category."

Some subsequent comments

- "Global exporter Li & Fung defended Wal-Mart as well: 'There has been no cancellation of orders from Wal-Mart and we continue to do business with them as usual. Also, Wal-Mart is continuing to place orders for 2014 as a normal,' said a spokesperson from Li & Fung, speaking to Reuters."

- David Tovar, Wal-Mart’s vice president of communications called the Bloomberg report 'completely irresponsible.' He added: 'I think they (Bloomberg) are taking a huge leap and drawing a very broad conclusion on one email from one buyer to one supplier.'

ADS - Reebok CEO talks to German newspaper

- Reebok CEO Matt O'Toole pointed to the fact that the brand's revenue and margins increased for the first time in years in the second quarter. He believes that the brand's margins will continue to improve and revenue will grow steadily.

Takeaway: This is notable, if true. But let’s keep in mind that just two weeks ago Adidas issued a big negative preannouncement due to top line weakness and product availability.

BBBY Earnings Quantitative Summary

NKE - Nike to release LeBron 11 iD and Zebra print pants

- The Lebron's will be available exclusively on Nike.com starting 10/11 and the pants are set to hit retailers this Friday.

Takeaway: The shoes make sense. The pants, however....

LVMH - Future of Marc Jacobs at Louis Vuitton in doubt

- "Marc Jacobs may be on the verge of leaving Louis Vuitton when his contract ends next month as designer's future at the French luxury brand remains unresolved, an industry source told Reuters."

- "'His contract may not be renewed,' the source told Reuters on condition of anonymity, without going into further detail. The French magazine Challenges this week said his departure had already been approved internally."

- "Marc Jacobs helped develop Louis Vuitton's women and men's ready-to-wear lines and runs his own eponymous brand which ranks among the most profitable smaller fashion subsidiaries within LVMH, fuelled by demand in the United States and Japan."

AMZN - Amazon to take on 15,000 new seasonal UK staff for Christmas crunch

(http://www.theguardian.com/business/2013/sep/24/amazon-christmas-15000-seasonal-staff-uk)

- "Amazon has announced it is hiring more than 15,000 seasonal staff across the UK to meet customer demand in the runup to Christmas."

- "The US internet retailer, which is expanding operations in the UK, said it expected hundreds of the temporary staff would later be able to take up permanent jobs."

- "Amazon said it was creating a variety of roles across its eight 'fulfilment centres' and its Edinburgh customer service centre.""

- "Amazon said that last year it hired 10,000 seasonal staff in the runup to the festive season and by the end of January had offered roles to 1,000 temporary workers."

GOOG, WFM, TGT, SPLS - Google Brings Retail Delivery Service to San Francisco Bay Area

- "Google announced on Wednesday that it will expand its same-day retail delivery service, Google Shopping Express, to cover all residents of San Francisco and the southern Peninsula part of the Bay Area."

- "The service allows users to shop from a number of large chain stores, including Target, Staples and Whole Foods, as well as some regional and local retailers, the company said."

- "In conjunction with the expansion, Google also launched iOS and Android apps for Shopping Express, allowing for mobile-based purchases to be delivered to users’ homes until nine in the evening."

- "Google isn’t the only one testing a same-day delivery retail program. EBay is working on eBay Now, which aims to deliver retail goods within an hour. And Amazon continues to test its 'Fresh' grocery delivery service with Los Angeles and Seattle residents."

PVH - PVH Expands Van Heusen Traveler for Fall

- "Van Heusen...is introducing a full travel-inspired collection that is targeted to a man on the go. Called Van Heusen Traveler, the multicategory collection is flowing into Kohl’s, J.C. Penney and Macy’s stores now for fall. A limited number of items had been tested for spring."

- "Retail prices are $19.99 for core crewnecks, $24.99 to $34.99 for shirts and $250-$300 for suit separates with out-the-door prices of $129 to $149, and pants are priced at $70-$80 with out-the-door prices of $34.99 to $39.99."

COLM - Columbia Sportswear Company Announces Appointment of Franco Fogliato as Senior Vice President of Europe

(http://online.wsj.com/article/PR-CO-2013049.html?mod=googlenews_wsj)

- "[COLM]...announced today the appointment of Franco Fogliato as senior vice president of Europe, reporting directly to president and CEO Tim Boyle, effective November 4, 2013."

- "Fogliato, 44, will be responsible for establishing and executing sales, distribution, and marketing strategies for the company's Columbia Sportswear(R), Mountain Hardwear(R), and SOREL(R) brands, sold through more than 5,000 wholesale customers across Europe."

- "Mr. Fogliato brings 17 years of European sales and marketing experience in the action sports and outdoor footwear and apparel industries. Since 2004 he has served as general manager of Europe for the Billabong Group...and as a member of company's executive board."

INDUSTRY NEWS

Denim Imports On The Rise

(https://www.sourcingjournalonline.com/denim-imports-rise/)

- "After declining 5% in 2012, total blue denim apparel imports are up 1.2% so far in 2013. A slight decline in the men’s segment has been more than offset by strength in women’s."

- "Import data from the Office of Textiles and Apparel, or OTEXA, show that in the first seven months of 2013, imports of denim totaled $2.27 billion. Total units rose 1.4% to 23.8 million dozen (286 million units), resulting in an average cost per unit of $7.94, virtually flat with last year."

- "China and Mexico are the largest sources of U.S. denim imports, with 29.7% and 25.8% of total dollar volume, respectively. So far this year, China’s share has increased by .1 percentage points, while Mexico’s has grown by .5 points. The fastest growing trading partners in denim apparel are Bangladesh, whose jeans are also the cheapest, and serve the fast fashion business, and Indonesia, which has grown its U.S. jeans business by 7.8% in the first seven months of the year."

Indian Shopping Rushes Online

(https://www.sourcingjournalonline.com/indian-shopping-rushes-online/)

- "Consumers across India are increasingly opting to shop online and retailers are joining the e-commerce space to keep up. Branded apparel has seen a year-on-year growth of 84 percent, according to a 2013 Internet Economy Watch Report by IAMAI, with 27.5 percent of apparel retailers taking up online sales."

- "The online shopping industry in India is fast catching on, not just in the larger metros but also in the smaller cities. The market is currently estimated at Rs 52,000 and is growing at 100 percent per year, ASSOCHAM notes."

- "With more than 100 million Internet users in India, half of which are choosing to make purchases online, both retail and consumer goods stores are getting into the e-commerce market, the survey noted."

Garment Industry Gets an Eco-Friendly Makeover

(https://www.sourcingjournalonline.com/garment-industry-gets-eco-friendly-makeover/)

- "Greenpeace began its Detox Campaign in 2011 with the goal of challenging major clothing brands and retailers to cease all discharge of hazardous chemicals from their supply chains and products."

- "Since then, 15 big brands including Nike, Adidas, Puma, H&M, Marks & Spencer, C&A, Li-Ning, Zara, Mango, Esprit, Levi’s, Uniqlo, Benetton, Victoria’s Secret, G-Star Raw and Valentino have publicly committed to the cause."

- "The first goal of the eco-group is to eliminate or substitute all hazardous chemicals from the manufacturing processes of its members. Other objectives ZDHC aims to achieve by 2020 include developing a process to screen and get rid of chemicals in the industry, create common chemical assessment tools and offer guidelines on best practices for supply chain stakeholders."