TODAY’S S&P 500 SET-UP – September 26, 2013

As we look at today's setup for the S&P 500, the range is 21 points or 0.58% downside to 1683 and 0.66% upside to 1704.

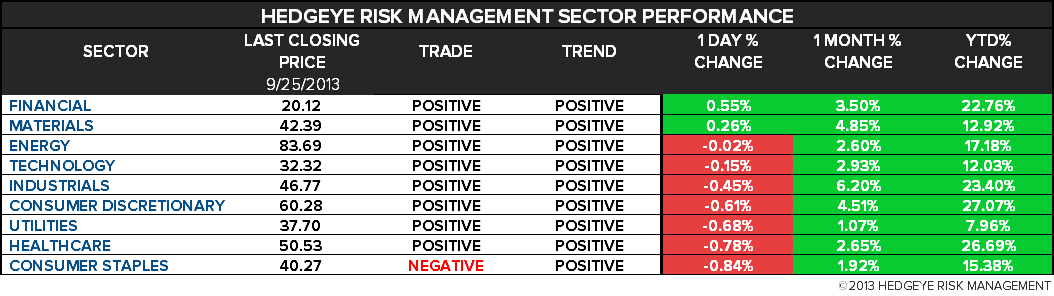

SECTOR PERFORMANCE

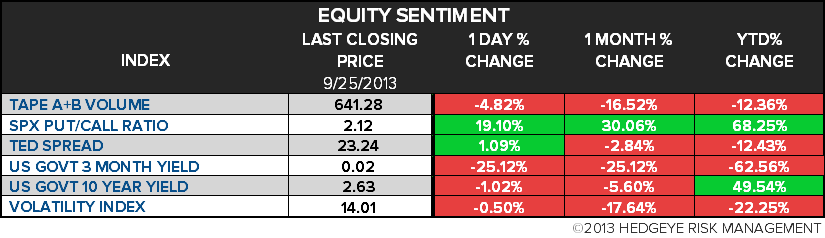

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 2.30 from 2.29

- VIX closed at 14.01 1 day percent change of -0.50%

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Init. Jobless Claims, Sept. 21, est. 325k (pr 309k)

- 8:30am: GDP Annualized Q/q, 2Q revised, est. 2.6% (pr 2.5%)

- 9:30am: Reserve Bank of India’s Rajan speaks in Frankfurt

- 9:45am: Bloomberg Consumer Comfort, Sept. 22

- 10am: Pending Home Sales M/m, Aug., est. -1% (pr -1.3%)

- 10am: Freddie Mac mortgage rates

- 10:10am: Fed’s Stein speaks in Frankfurt

- 10:30am: EIA natural-gas storage change

- 11am: Kansas City Fed Manufacturing, Sept., est. 8 (pr 8)

- 11am: Fed to purchase $1.25b-$1.75b in 2036-2043 sector

- 12:15pm: Fed’s Kocherlakota speaks in Houghton, Mich.

- 12:35pm: Fed’s Pianalto speaks in Cleveland

- 1pm: U.S. to sell $29b 7Y notes

- 6:15pm: ECB’s Coeure speaks in New York

- 9:15pm: Fed’s George speaks in Denver

GOVERNMENT:

- Canadian Minister of Intl Trade Ed Fast meets with Sec. of Commerce Penny Pritzker, U.S. Trade Representative Michael Froman to discuss job creation and trade

- 8:30am: Atty General Eric Holder delivers remarks at Justice Dept’s Summit on Preventing Youth Violence

- 10am: Senate Homeland Security Cmte hears testimony on overhauling U.S. Postal Service

- 10am: Senate Commerce Cmte hears from airline industry, manufacturers on jobs

- 10am: House Budget Cmte meets on long-term budget outlook

- 10:55am: President Obama to speak on Affordable Care Act at Prince George’s Community College

- 2pm: Senate (Select) Intelligence Cmte holds hearing on FISA

WHAT TO WATCH:

- JPMorgan said to see possible $11b mortgages settlement

- Citigroup to pay Freddie Mac $395m to end mortgage claims

- Lacker says expanding Fed assets increases costs of any missteps

- U.K. prosecutors said to plan more Libor charges in Oct.

- NYSE, Nasdaq said to weigh plan to collaborate on backups

- Deutsche Bank said to propose creating bond platform w/ rivals

- Icahn-backed Ferrous hires Itau to seek $1.5b in funding

- J.C. Penney seeks to raise $750m-$1b in new equity: Reuters

- U.S. data providers hit with cyber attack: Reuters

- Caesars selling 10m shrs in fresh public offering

- Takeda duped patients, doctors on Actos risks, lawyer says

- U.K. eco. growth accelerates in 2Q as consumer spending rises

- H&M gains most in more than 3 yrs after beating estimates

- Fed monetary policy didn’t leak early, firm’s study finds: FT

- Apple ordered to pay 330m yen in Japan on iPod patent: Kyodo

- Cargill, Bunge study bids for Deoleo, Economista says

EARNINGS:

- Accenture (ACN) 4:01pm, $1.01

- Cantel Medical (CMN) 8:30am, $0.23

- Ferrellgas Partners (FGP) 7am, $(0.31)

- McCormick (MKC) 6:30am, $0.79

- Nike (NKE) 4:15pm, $0.78

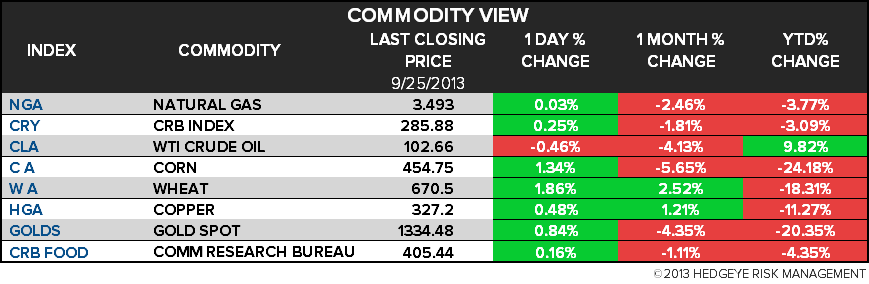

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Commodity Constraints Show ‘Super Cycle’ Endures, McKinsey Says

- U.S. Corn Sales Fall Most Since ’75 as Farmers Reap: Commodities

- WTI Trades Near 12-Week Low; BofA Sees Iran Diplomacy Limited

- Wheat Near One-Month High as U.S. Sales, China Demand May Climb

- Copper Climbs Before Report Seen Showing Stronger U.S. Growth

- Gold Advances for Third Day in London on U.S. Budget Impasse

- Cocoa Swings as Ivory Coast Sells Amid Shortages; Coffee Drops

- Abenomics Peaking for Tocom Volume Means Focus on China, India

- Rebar Declines to 11-Week Low as China Affirms Property Curbs

- China Cotton Use Drops in Switch to Synthetics: Chart of the Day

- China Silver Indicators Lackluster as PC Manufacturing Down 14%

- Russian Gas Lowest Since 2011 Favors Link to Oil: Energy Markets

- Aluminum Shipments by Japan Steady in August, Group Says

- Ivory Coast Offers Cocoa for 2014-15 in a Futures Bull Market

CURRENCIES

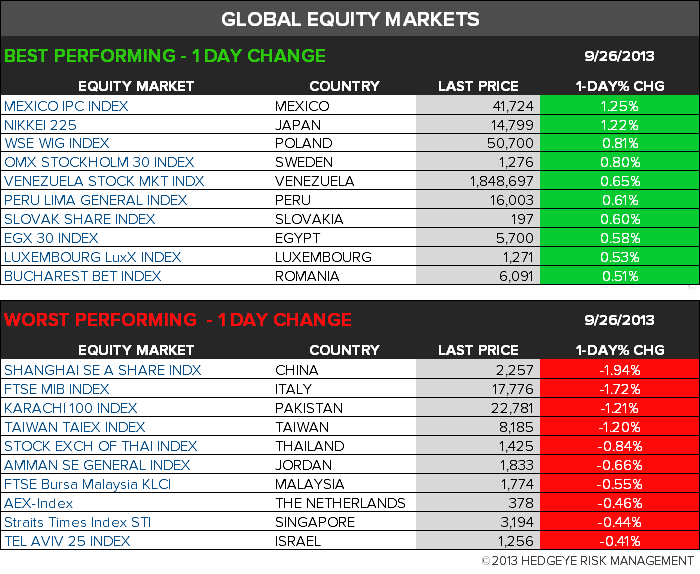

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team