Clients often remind us that we’ve had a great call on MCD this year, but also prod us not to get carried away with our bearish bias. Admittedly, this is not an easy feat – but, as the facts change, so will our call. Our intention is always to remain flexible in our coverage.

That being said, our bearish bias has not changed. Below we highlight four recent events and their potential implications.

- The stock outperformed the S&P 500 over the past month

- The current Mighty Wings promotion

- Changes in the Eurozone

- Personnel changes in the U.S.

Stock Price Performance – MCD is up +2.8% over the past month, outperforming the S&P 500 and its quick-service peer group by 80 bps and 200 bps, respectively. Given that the stock had underperformed the S&P 500 by -20.9% YTD, we knew the slightest whiff of good news would push the stock higher. So where is the good news coming from?

Mighty Wings – MCD hasn’t generated as much buzz around a limited-time offer (LTO) since the McRib promotion. But, at the end of the day, it is just a LTO. The recent buzz might create a month or so of stronger sales trends, but we don’t view this promotion as a game changer for the company. Selling chicken wings may temporarily boost sales, but, in the long run, we fear that it will end up inflicting more harm than good. Asking the currently disgruntled franchisee community to prepare yet another product, with a slower than normal preparation time, will only add to the service issues the company is already experiencing. In our view, this is likely to lead to further deterioration of the MCD brand.

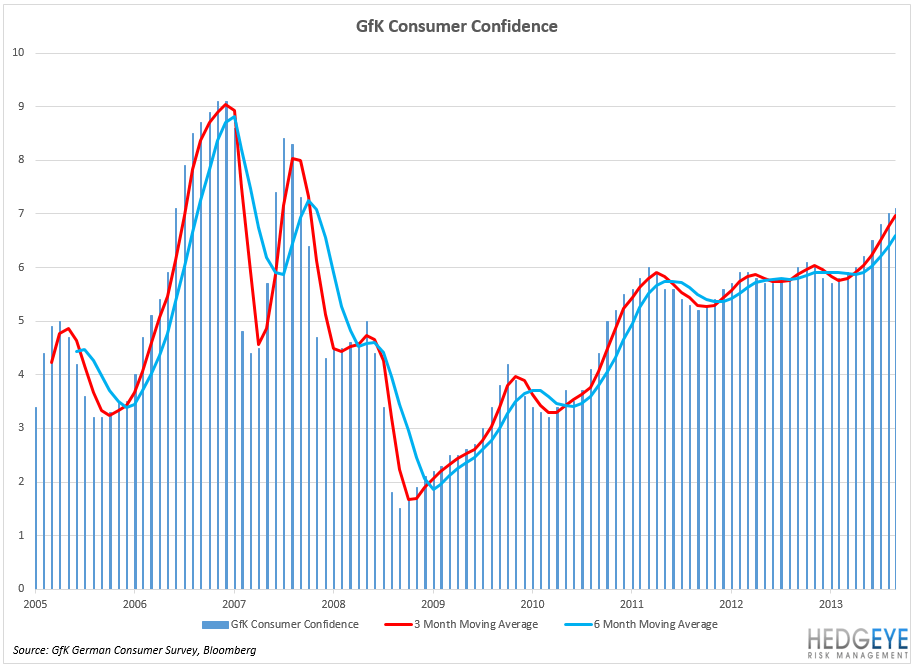

Changes in the Eurozone – MCD has been trading better since the release of August comps on September 10th. Global trends in August were stronger due in large part to better than expected results in Europe. The company reported Europe same-store sales growth of +3.3%, on top of +3.1% growth a year ago, as the UK, Russia, and France were strong. Several of the MACRO indicators we monitor in Europe continue to show improvement in the region, specifically in Germany, MCD’s most important European region. Today, the forward-looking German Consumer Confidence Indicator from the GfK Survey rose to 7.1 for October, surpassing consensus expectations. GfK notes that, “despite a fall in income expectations, German consumers are almost euphoric when it comes to their propensity to consume.” Investors also got some good news from Italy, another market that has given MCD considerable headaches in the past. Today, Italy’s Consumer Confidence Index jumped to 101.1, its highest level since June 2011.

Personnel Changes in the U.S. – Yesterday we learned that MCD’s Neil Golden plans to retire early next year. Given the importance of MCD’s marketing message, it is clear that the company does not have its act together, particularly in its most important region, the U.S. Despite the recent limited-time offer of Mighty Wings, McDonald’s continues to struggle in the region.

Summary

The stock is having a strong month and Europe is looking stronger, on the margin, for the company. However, the U.S. continues to struggle and we believe it will be a while before the company returns to high-single digit EPS growth.

Howard Penney

Managing Director