- Bullish on Merkel’s Win, Coalition with the SPD likely

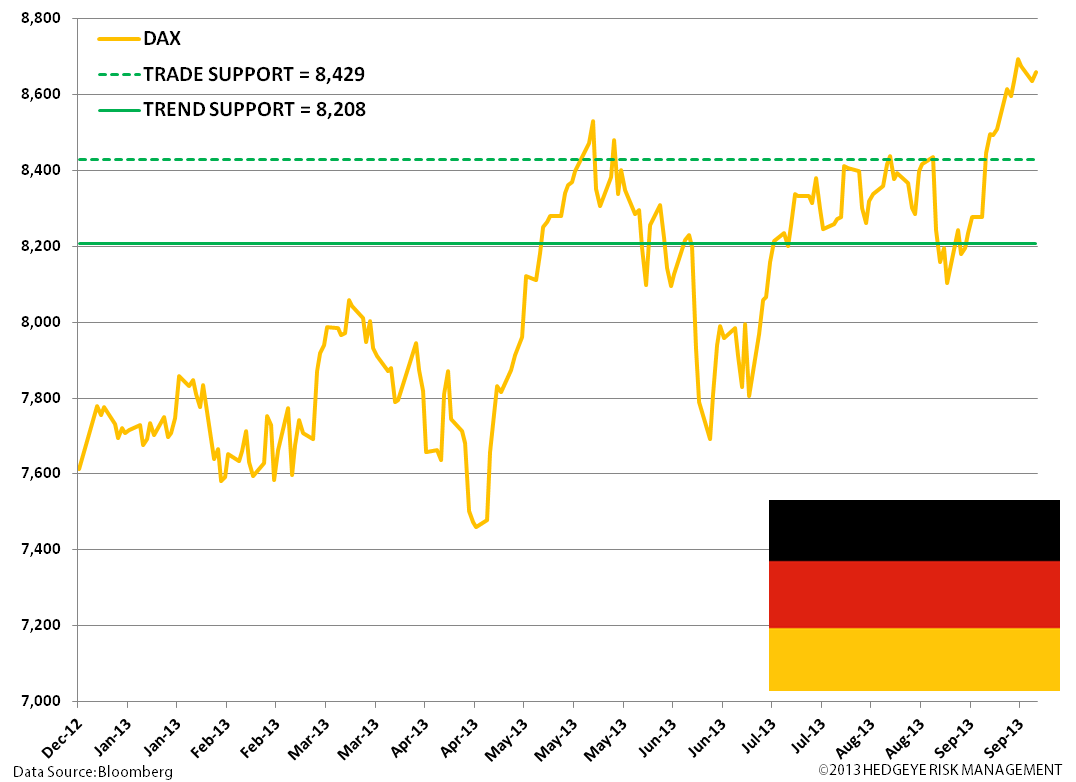

- DAX is in a bullish breakout across its immediate term TRADE and intermediate term TREND durations

- IFO German Business Confidence pushes higher in September reading

- EUR/USD strong on The Bernank No Taper Trade

Sunday ushered in a huge win for Chancellor Merkel, receiving a convincing 41.5% of the votes (5 seats short of an absolute majority in the Bundestag), while her former coalition partner, the Free Democrats (FDP), were bounced out of parliament having received less than the 5% minimum to retain their seats. The results portend a very likely alliance between Merkel’s CDU/CSU and the Social Democrats (SPD). For reference, this coalition, named the grand coalition, and last seen in 2005-2009, took 65 days to firm up back in 2005. How long will it take this time around?

It’s tough to pin down just how negotiations will flow. Merkel has said that she hasn’t ruled out a coalition with the Greens, the party with the fourth biggest showing. However, we think a coalition with the Greens is unlikely, and may well just be a bargaining chip to play against a very likely coalition with the SPD. We do expect a heavy level of political jockeying in the coming days and weeks as both sides look to secure key ministerial positions.

The SPD remains a party that has largely backed Merkel’s initiatives on EU and Eurozone policy, including the multiple bailout programs: we think the market will be bullish on this continuity. Further, we would not expect this stance to change within a grand coalition. Finally, we expect negotiations between to the parties to center more on domestic issues; the SPD may push for a national minimum wage and higher taxes on the wealthy, both of which have been opposed by Merkel.

Bullish DAX

As the politicking runs its course, we are bullish on the German equity market, a position we’ve held for much of the year. As Keith said today on the morning call:

“Respect is earned, not allocated. Over in Germany, Angela Merkel doesn’t have a bunch of Fed heads running around like chickens with their heads cut off making conflicting speeches to manic media people now does she? The DAX “correction” looked nothing like that in the S&P 500. Both DAX, the FTSE and Nikkei are all looking better now than S&P 500. Why not buy them instead?”

Below we highlight our key durations on the DAX that are screening a bullish breakout:

German Data Grinds Higher

Below we show the IFO German Business Confidence survey. While it is but one of many surveys and data points we track, the 6-month forward Expectations figure beat consensus estimates and rose month-over-month to 104.2 versus 103.3 in August. The positive data point is reflective of the grind higher in German data over the last 3-6 months. We maintain our bullish bias on German equities.

EUR/USD Levels (Refreshed)

On what we shall call The Bernank No Taper Trade, the EUR/USD levels are grinding higher. Our topside trade resistance is now $1.36.